The New Year has ushered in with a bitter aftertaste for the Euro zone. On one side, it is threatened by the risks of deflation and slower recovery and on the other hand looms the exit Greece from the currency union as the forces of the radical left (SYRIZA) and center right have a face off during the elections on January 25.

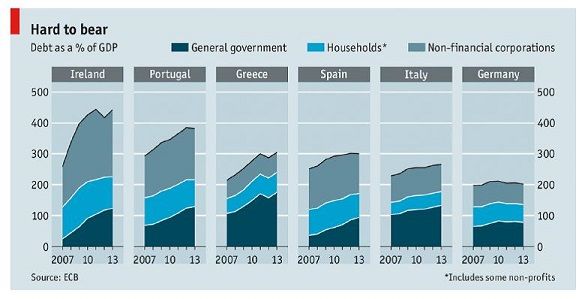

The Euro zone has been plagued by a plethora of troubles since the crisis in 2009. A persistent area of concern has been the rising debt to GDP ratios across countries with the average increasing to 93% from 66% between 2007 and 2013. For countries like Greece and Portugal the percentage of government debt to GDP rose to 175% and 129% respectively.

The image has been sourced from an article by The Economist

Greece in fact was the only country in the Euro zone to have witnessed an official debt restructuring. Although the Euro zone in the first half of 2014 was witnessing slow recovery and officials (read Angela Merkel) were still sceptical about QE, Greece raised 3 Billion Euros worth bonds with less that 5% yield. Just as things began to look up, the markets witnessed global sell offs pushing bond yields up with Greek bond yields momentarily exceeding 9%.

As the risk of deflation increases the plight of debt burdened countries increases as repayment becomes more expensive. If the trend in weak demand and non-existent recovery continues the Euro zone might be propelled into stagnation as was witnessed by Japan in the nineties.

As an early response to the impending instability the Euro, the Euro fell to $1.1864 against the dollar on Monday January 5th 2015.

With Syriza routing for writing down nominal debt, increasing minimum wage and putting an end to the austerity regime in Greece all eyes are on the much awaited elections January 25th. A victory for Syrizia and enforcement of non-austere economic measures might lead to debt default and potentially an exit from the Euro.

So what are your thoughts and predictions for the Euro zone?

The content for the blog has been sourced using:

The Euro Crisis Is Entering A New, Highly Dangerous Phase , The euro crisis Back to reality , Samaras Warns of Euro Exit Risk as Greek Campaign Starts , Euro Slides to Weakest Since 2006 on ECB, Greece as Yen Advances

IMO if Greece were to leave the eurozone, it would have happened in 2011/2012. That being said, SYRIZA is not a trustworthy party; they officially claim that they want to stay within the eurozone, yet the promises they have given to the people are not feasible without money printing or a big debt haircut. Moreover, some members within the party are lunatic leftists making comments on what are they going to do that are out of the party's official line and cause more worries (i.e. bail in). Unsure about what's happening behind the scenes. Some fund managers have been net buyers during the last turbulent days (namely Wellington, LNG Capital) and others which have stayed long for a while (Einhorn, Loeb).

I think currency wars will continue. Deflation risk in the Euro zone is real and although QE infinity hasn't really done much to help, what else are they going to do but debase the Euro further?

now I just feel dumb for not going long the US $ earlier....although I also don't feel like the FED is going to be raising interest rates (if at all) until very late 2015...

Who knows :-)

Eveniet odio necessitatibus quis sunt odio veritatis vel. Aliquid maxime ipsam repudiandae molestias. Molestiae odio dolorem magnam molestiae quasi eligendi sit quod. Vel enim nobis autem consequatur ut quasi eligendi.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...