If you are old enough to remember market fevers from past booms, you are probably inclined to dismiss both the claims and the valuations as fantasy. I do believe, however, that there is a kernel of truth to the disruption argument though I think investors are being far too casual in accepting it at face value. As I attempt to attach a value to Uber, I have to confess that I just downloaded the app and have not used it yet. I spend most of my of life either in the suburbs, where I can go for days without seeing a taxi, or in New York City, where I find that the subways are a vastly more time-efficient, cheaper and often safer mode of transportation than taxis.

Uber has been able to grow at exponential rates since its founding in 2009 by Garrett Camp and Travis Kalanick, with the latter (who is new CEO) claiming that it is doubling its size every six months. While we have no access to the company's financials, there have been periodic leaks of information about the company that allow us to get a sense of its growth. Here, for instance, was a picture that was widely dispersed in December 2013 of a five-week period in late 2013:

While the company claimed to be outraged by the leak, it played nicely into the narrative of growth that it was selling to its investors. In fact, the December leaks suggested that the company generated gross receipts (the fares paid by customers for cab rides) of $1.1 billion, which would translate into revenues of $220 million (based on the 20% slice that Uber claims for itself). That was a few months ago and at the rates at which the company is growing, I would not be surprised if the updated values for both numbers are higher; I will be using $1.5 billion for the gross receipts and $300 million as revenues for Uber as base year numbers.

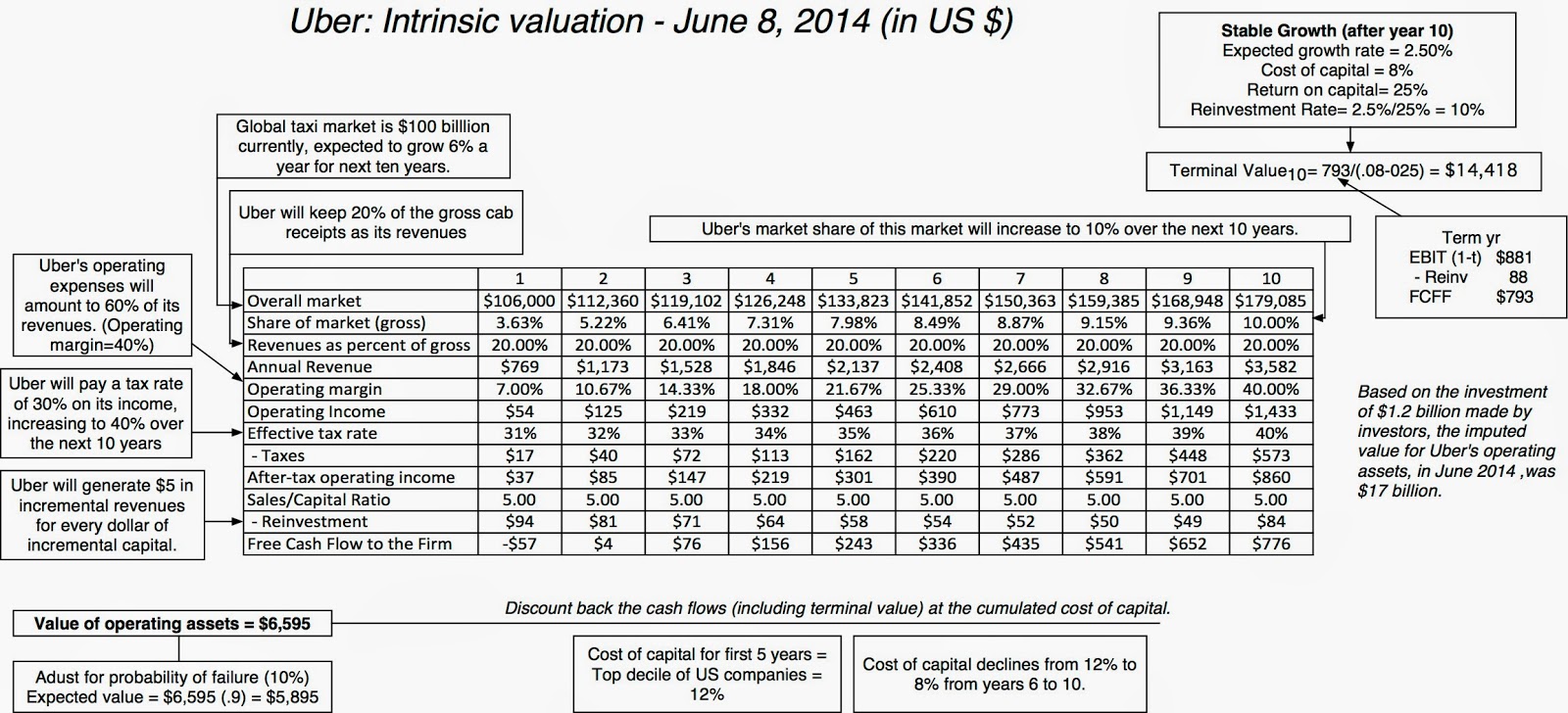

For my base case valuation, I am going to assume that the primary market that Uber is targeting is the taxi and limo service market, globally. I know that there is talk (some from Uber's management and some from analysts) that Uber could extend its reach into other businesses (car rentals, moving and even driverless cars), but I don't see any evidence that it has succeeded in making any breakthroughs (yet) and will come back to this question later in my post.

It is true that many cities, especially in Asia and Latin America, are under served currently and that the taxi business globally will continue to grow at well above the 2-3% rate that we have observed in the US, Japan and UK, and that services like Uber will contribute to the faster growth. I will estimate an expected growth rate of 6% a year for the next decade, increasing the overall market to $183 billion in 2024.

The taxi and limo market currently is dominated by small, local players and is regulated in most cities. The cities restrict entry into the market and in return, they regulate the prices that cabs can charge their customers (more effectively in some cities than others). While Uber has only a minuscule slice of the overall revenues currently, the market share that it can aspire to get will depend upon the following factors:

The metric that I will using for reinvestment is one that you may be familiar with, if you have seen my other young company valuations, and it is the sales to capital ratio. This number measures how much incremental revenue you expect to generate for each incremental dollar of investment; the higher this number, the less capital investment is needed to expand this business. The median value for technology companies on this is about 2.50, the median value for all US companies is about 2.00 and a really high number would be about 10.00. I will assume that the sales to capital ratio for Uber will be 5.00, towards the high end of the spectrum.

5. Risk

Is there a lot of risk in investing in a young, start-up like Uber? Of course, but much of the risk in the investment is survival risk (i.e., that the company will not make it as a going concern) and not operating risk. The discount rate, the primary mechanism for adjusting for risk in a discounted cash flow valuation, is designed to capture the latter and is ill-suited for reflecting the former, notwithstanding venture capitalists' attempts to push it into a target rates of return.

Looking at the operating risk side of the equation, the taxi business is a cyclical one, with revenues tied to economic growth. There are only a handful of publicly traded cab companies in the world, but the

wacc.htm">cost of capital of companies in the transportation business in US dollars is about 7.08% for US companies and 6.93% for global companies.

As a young, start-up with higher fixed costs, Uber is undoubtedly more risky than the average company in this sector and I will assume that its cost of capital is 12% (the top decile of US companies). As it matures and becomes a larger, more profitable company, I will assume that the cost of capital will decline towards 8%, the median for US companies. (I don't think that Uber will carry the debt that a typical transportation company carries and thus will not be able to push its capital towards the industry average of 7%.)

On the risk of failure, Uber has passed its most critical tests. It has a product/service that is generating revenues, has relatively little debt or fixed commitments and most importantly, it has access to capital. In fact, the $1.2 billion in cash that it will raise in its latest round of capital should provide it with enough of a cash cushion to survive leaner times, at least in the near term. As a result, I will assume that there is only a 10% chance of failure in Uber and that the company's liquidation value will be zero.

6. The value

With these pieces in place, I arrive at a base case valuation of $5.895 billion for Uber, as shown in the figure below:

|

| Valuation of Uber, June 8, 2014 |

The value of $5,895 million is a value for the operating assets and any existing cash would have to be added back and debt netted out. Given that neither debt nor cash is likely to be a large number right now, it is directly comparable to the

value that venture capital investors are attaching to the company now. As with my other valuations, you can

download this one and make your own judgments on what the future holds for Uber. (This is a generic spreadsheet that you can use to value any start-up and you can try it on Airbnb and Dropbox, if you are so inclined.)

7. Break even points

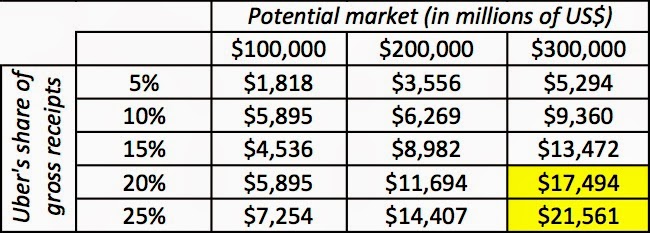

The imputed value for Uber, based on what investors demanded for their $1.2 billion last week, is $17 billion, well above my estimate of value. It is entirely possible that the error is mine and that I have under estimated a key input into value. In particular, there are three key drivers of Uber's value:

(a) the potential market, which I estimated to be $100 billion

(b) the market share that Uber will command of that market (my estimate is 10%) and

(c) the slice of gross receipts that Uber will get to keep (which I have left at 20%)

Changing any or all of these assumptions will change value. In the table below, I hold the gross receipt slice constant, at 20%, and change the potential market size and Uber's market share to arrive at the following numbers:

|

| Value of operating assets for Uber, keeping revenue slice at 20% and other inputs fixed |

The shaded numbers indicate the combinations of total market/market share that you would need to deliver. In particular, the total market has to be either three times bigger than my estimate (around $300 billion) or the market share has to be more than twice my estimate (20% and higher) to justify the $17 billion value.

Holding the market share fixed at 10%, I looked at the effect on value of changing the potential market and the percent of gross receipts that Uber receives, and the effects are summarized below:

|

| Uber operating asset value, holding market share and other inputs fixed. |

The effects of a reduced market slice are more devastating to value, with even a $300 billion total market (with a 10% market share) being insufficient to break even, with a $17 billion value, if Uber keeps less than 20% of gross receipts.

The bottom line: Viewed as a car service company, even with optimistic assumptions about market growth, market share and profitability, Uber's value is about $6 billion. The combination of assumptions that you would need to get to $17 billion is improbable, at least in my view. It is possible that I am missing the value of new markets that Uber may be able to enter but I will reexamine that possibility later in this post.

Pricing Uber

As I have argued in

many of my blog posts over the last two years, the value of an asset can be very different from its price. The former is determined by the interplay of fundamentals (cash flows, growth and risk) whereas the latter is a function of demand and supply. To price an asset, you follow two simple steps. In the first, you look for a

metric that the market is scaling the price to; that metric can be an operating number like revenues or earnings or an intermediate number like number of users or customers. In the second, you

identify "comparable" companies, i.e., companies that are like the one that you are valuing and compare the scaled price (the multiple) across these companies. Most investors and analysts are more comfortable pricing assets, rather than valuing them, and this is especially the case with young companies like Uber. So, is that what investors are doing to arrive at the $17 billion price for Uber? To make that judgment, let's look at the choices when it comes to pricing metrics and comparable firms.

Pricing Metric

You cannot compare values or market capitalizations across companies, because companies can vary in terms of size and scale. Dividing the estimated value by a scaling variable creates a multiple that can be compared across companies.

With mature companies, you scale market value (equity or enterprise) to measures of earnings, dividing market capitalization by net income to get to a PE ratio or enterprise value by operating income or EBITDA to get an enterprise value multiple. With young companies, where earnings are often negative or minuscule, earnings multiples either cannot be computed or are not meaningful. In fact, the only current operating number that is consistently positive at those companies is earnings, explaining why revenue multiples are so widely used at this stage in the life cycle. The fact that revenue multiples can be computed does not necessarily mean that they are useful in valuation. Dividing Uber's value ($17 billion) by the revenues ($300 million) yields a revenue multiple of 56.67, an outlandishly high number but one that tells you little about the pricing of the company, partly because investors are pricing these young companies on potential, not current performance.

One solution to the problem with current numbers not reflecting potential is to use expected future revenues or earnings in computing multiples. Thus, you could divide the enterprise value today by the expected revenues in five or ten years and compare these forward multiples across companies. Applying this approach to Uber, I divided the enterprise value of $17 billion by my expected revenues in ten years ($3.59 billion) to yield 4.75, still a high number and one that should be compared to the same multiple (enterprise value to future sales) computed for other companies. The problem with this approach is two-fold. The first is that you need to forecast revenues for each company in your sample, not just the company that you are valuing. The second is that these multiples are only as good as your revenue forecasts, making this a joint test of the multiple and your forecasting ability.

In

my post on Whatsapp and Facebook's valuation of it, I noted that the metric that best explains the difference in values across companies is not revenues or earnings, but the number of users. While that may strike some as being irrational, it is not unreasonable to assume that companies with more users are better positioned in terms of potential. If Uber, Lyft and Hailo (all of which operate in the taxicab market) were all publicly traded, what equivalent metric would investors focus on? It could be the number the subscribers to the service, the number of rides taken by these subscribers or even the number of cabs covered by the service. For the moment, though, we are still in the dark about all of these statistics for these companies.

Comparables

In pricing, the choice of companies that you compare your company to is critical. In fact, one simple way to tilt the pricing in the direction that you want it to go is to change the firms that you use in your comparison. In the case of Uber, we will first try to value it, relative to other publicly traded young technology firms and then try again, relative to private technology companies that have received venture capital infusions in the last year.

If we define Uber's comparable companies as young, technology companies that are being priced on potential, the most obvious subset of companies that we can compare it to are social media companies. In the table below, I update the numbers for social media companies, with key multiples computed in the last four columns:

|

| Enterprise and market values from June 2014, Trailing 12 month numbers |

Since the only number that we have some measure of (and a rough one at that) is Uber's revenues ($300 million), applying the median multiple of 9.22 yields a value of $2.766 billion for Uber. Even applying the highest value (Twitter's

EV/Sales of 21.82) yields a value of $6,546 million, well below the $17 billion estimate. Uber reports the number of cities that it operates in, but it provides no detail on the exact number of subscribers to the service and the number of rides that it provides. Even extrapolating from the leaked report (shown towards the top of this post), that shows up 90,000 new users signing up each week, I get 4.68 million sign ups for a year and perhaps 15 million subscribers overall. Applying the median value of $70/user to this number leaves you with $1.05 billion and even applying the high (Netflix's $568/user) yields a value of just over $8.5 billion.

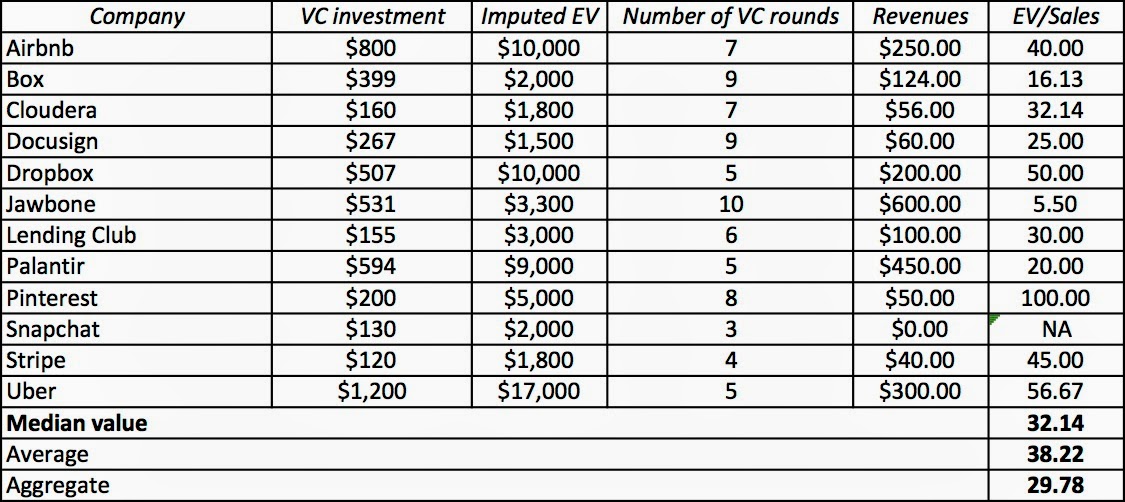

It is possible that the investors in Uber are comparing its pricing to the imputed pricing of the other non-public "big" companies in this space. In the table below, I have highlighted the largest private technology companies with

VC investments in the last 12 months, the imputed valuations and the revenues in 2013 (or at least the best estimates that I could find):

|

| VC investments, imputed valuations and revenues in 2013 |

Even in the rarefied air of

VC valuations, Uber's $17 billion dollar value stands out as an outlier. Applying the median multiple of revenue (32.14) across just these companies to Uber's revenues would still leave you with a valuation just under $10 billion.

The bottom line: Even if I use the most favorable pricing metric (revenue) and comparable firms (other favored

VC targets), it is difficult to justify a price greater than $10 billion.

Uber, the disruptor

While I admire the big picture perspective that strategists like Michael Porter and Christensen have brought to business, I am, by nature, a skeptic and feel the urge to tie the big picture to the bottom line. As I see it, disruptive innovation affects value at two levels. In the first, it allows a new entrant to enter a targeted market, disrupt the status quo and then capture the excess profits in that market. That can be captured in a discounted cash flow valuation, which is what I attempted to do in my intrinsic valuation of Uber. The second level at which disruptive innovation affects value is more subtle. Assuming that the disruptor is able to succeed in its targeted market, success in that market may allow the disruptor to enter new and potentially larger markets in the future. The fact that these markets are undefined at the moment and the odds of success are low mean that the intrinsic value added from this possibility is small. However, the fact that the disruptor does not have to commit to investing in these new markets until the outcome from the initial market is known, as well as the potentially large profits from this expansion, give it the characteristics of an option. I do not want to entangle myself in the mechanics of option pricing in this post, but the value of this disruption option is an add-on to the intrinsic value and will increase with the size of the potential markets, the uncertainty/risk in these markets and the competitive advantages that the disruptor brings to these markets.

Applying these very general concepts to Uber, the attraction to investors is clear. Uber's contention is that it is targeting the car service market for the moment but its intention is to use success in this market to expand into other markets. While we can be skeptical and uncertain about its chances of success in these fuzzily defined markets, that uncertainty, which would reduce intrinsic value, increases the value of the disruption option. To give Travis Kalanick, the co-founder and CEO of Uber, credit,

his subtle pitch that Uber is in the logistics business plays into the option narrative, as does the fog that the company has created around specifics.

It is easy to see the allure of the option argument, where uncertainty becomes your ally and big markets beckon, but as investors, we need to understand that most deep out-of-the-money options never get exercised and that the company owners/managers cannot be given free rein over narratives. I am not privy to the questions that investors in Uber asked before they made their investment, but I would hope that they pushed Mr. Kalanick to be specific about his expansion plans, the details of growth and what it is costing to deliver that growth, and most importantly, what will give Uber the exclusivity to be able to advance into new markets faster and more profitably than its competitors (both current and new).

Bottom line: Can the disruption option explain the difference between the assessed value ($17 billion) and the estimated value ($6 billion, with intrinsic valuation)? It is possible but not probable. For the option to be worth $11 billion, the potential markets that Uber can enter, assuming it is successful in the car service business, will have to be at least four times larger than the base market (the $100 billion taxicab market). I know that there is talk of Uber becoming a player in a futuristic world of driverless electric cars, but even if that scenario unfolds, I don't see why Google and Tesla would let Uber have anything more than crumbs off the table.

The end game

The numbers seem to indicate that Uber is being overpriced by investors who have valued it at $17 billion. Since these investors are presumably sophisticated players, how would I explain their pricing? I will not try, since I did not pay the price, but it is worth remembering that even smart investors can collectively make big mistakes, especially if they lose perspective. The tech world is a cloistered one, where the leading players (venture capitalists, managers, serial entrepreneurs) immerse themselves in minutiae and know and talk to each other (and often only to each other). Not surprisingly, they develop tunnel vision where technology (or at least their version of it) is the answer to every problem, the status quo is both inefficient and easily disrupted and 50 times revenues is cheap! If history is any guide, tech geeks are just as capable of greed and irrational exuberance as bankers are.

Attachments

Intrinsic Valuation of Uber

Uber Pricing: Multiples and Comparables

Very interesting break down and analysis. Always an interesting read. One interesting component of Uber is with regards to regulation. They are completely disregarding most of the regulations in many of the local markets they are entering. In the short term, this "negative" press (the strike etc) is creating lots positive attention for Uber. I'm wondering if in the long term, some of these brash moves will come to bite them in the butt (once the regulators start making cases against them).

With that being said, to add some qualitative spin/personal perspective to this article, the true differentiating factor of Uber is their service they provide to users. I now almost exclusively use Uber when I'm out in Boston: I know exactly where and when I'll be picked up (no more uncertainty/waiting), the drivers have always been friendly, and in many cases the cars and rides are much nicer than traditional cabs. Part of the high valuation may be due to the brand that this company is creating, where many users become strong advocates and loyalists, something they could take advantage of down the line as they expand their service offerings

Explicabo numquam repellat ipsam alias. Et quos maiores repellat veniam delectus sit et ut.

Numquam consequatur itaque alias. Ut possimus dolores veniam ullam. Voluptatem modi et aliquam ut occaecati consectetur.

Eaque earum autem nisi voluptates. Dolorem voluptatem modi quia amet. Velit fuga sint ea amet hic perferendis aliquam. Iusto aut error quis quia qui reprehenderit beatae magni. Aut et sapiente eius qui nobis. Error quisquam eos error ad. Cum quia et aliquid ut.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...