My last post on Facebook’s acquisition of Whatsapp brought a whole host of responses, some of which took issue with my argument that it is easier to explain the deal using pricing metrics, especially ones that are used in the social media sector (# users) than with valuation models or logic. One of the arguments made by some of the commenters was that I was missing the real reason for the deal, which was that it was a defensive maneuver by Facebook, designed to both protect its profitability and to keep a prime competitor (Google) from acquiring Whatsapp. Many of these commenters also emphasized that these defensive deals cannot be assessed using conventional valuation techniques and that we have to trust management to make the right judgments on them. I don't have a bone to pick with the logic of defensive deal making, but as a valuation person, I don't agree with the claim that defensive deals cannot be valued. If preemption is the primary rationale behind an action, I believe that it not only can be valued but it should be valued.

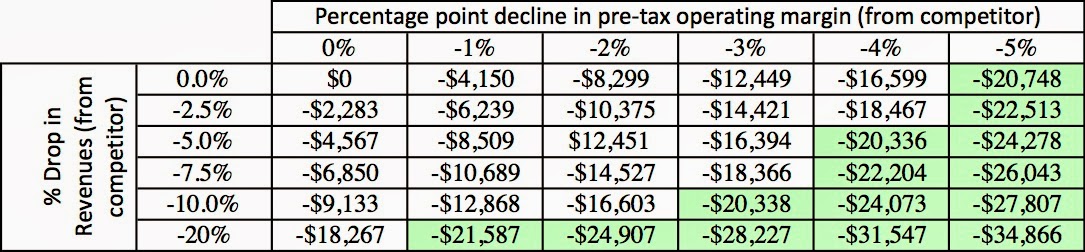

Now, assume that this company is faced with Company B, a young company that has a product that has no revenues right now, but if allowed to develop or in the hands of a competitor, could eat into Company A’s market and lower its after-tax cash income to $ 6 million. Even though company B has little income potential on its own, company A should be willing to pay up to $40 million to acquire it.

-

The business you are defending is worth defending: Acting in defense of a business makes sense only if that business is a good one, and the measure of a good business is whether it generates returns on invested capital that exceed the cost of funding that business. If you own or run a bad business, spending money to defend that business strikes me as a pointless and expensive exercise. Lest this sounds like a weak precondition, note that by my calculations in 2013, about 60% of all listed companies (40,000+) globally generated returns that were below their costs of capital, and more than a third of them under performed by substantial margins (>5%).

- The threat is real, not imaginary: Spending preemptively to ward off a threat makes sense only if the revenue loss/ margin decline that is anticipated is real and is not just in the fevered imagination of the top management. While you can argue that this is a business judgment that should be left to the top managers of a firm, a paranoid CEO, egged on by “strategic” consultants and aided and abetted by bankers, eager to get the deal done, will find a hundred potential threats for every real one.

- The preemptive action is the most efficient (and cheapest) way to ward off the threat: Even if the threat is to a valuable business and is imminent, there may be less expensive and simpler ways to deal with the the threat then the chosen action. Thus, if you can acquire a technology from a company or exclusive licensing rights for a billion, you should not be spending $10 billion to buy the whole company.

- The threat is unique and not easily recreated: Spending money to eliminate a potential threat makes sense only if the threat is unique and not replicated easily/quickly. If the threat can be replicated easily, the spending company will find itself repeatedly spending larger and larger amounts of its depleting stock to make subsequent threats go away. These are companies with fragile business models with shallow ditches rather than competitive moats separating them from mediocrity.

- Survival is not the end game: As I have noted in my prior posts, there is no glory in growth for the sake of growth or business survival for the sake of survival. A business is a commercial enterprise and if you cannot generate sufficient returns, given the risk you face and the capital you have invested, you should shut the business down.

- Doing nothing is not only an option but it may sometimes be a better one than doing something: We live in a world where activity is not only prized more than inactivity, but one in which there is far more money to be made by people from promoting activity (consultants, bankers) than from promoting inactivity. At the risk of sounding like stodgy, I believe that it is better sometimes to do nothing instead of doing something, especially if that something is ill advised or expensive.

- If your competitors are planning on doing something stupid, let them do it: If your competitors want to overpay for companies or take investments that generate substandard returns, your best option is often to let them do it. Especially with acquisitions, the winners of the deal making contest are not necessarily winning for their stockholders:

This graph looks at winners and losers in multiple-bidder acquisitions and looks at the returns that investors would have made in the 40 months after the deal is done. The stock price, on average, declines by about 35% in the deal winners and increases by 25% in the deal losers in that period.

This graph looks at winners and losers in multiple-bidder acquisitions and looks at the returns that investors would have made in the 40 months after the deal is done. The stock price, on average, declines by about 35% in the deal winners and increases by 25% in the deal losers in that period.

Wrapping up

While I have framed this post in terms of the Facebook/Whatsapp deal, I continue to believe what I said in my first post. I don't think that Facebook's management is doing this deal for defensive reasons or because they have explicit plans for generating value, at least as of now. It is Whatsapp's large, growing and engaged user base that makes it so attractive to Facebook, especially given how much the market is pricing all of those factors. You may find it difficult to believe that someone as smart as Mark Zuckerberg would pay $19 billion without a clear vision of how he plans to make money off the deal, but I don't.

If we don't our competitors will. That's exactly the mindset of Wall Street before the '08 crash. To quote John Mack "We can't help ourselves".

If I were a tech analyst I'd be screaming "SHORT THE HELL OUT OF THE SECTOR".

....but I'm not.

Porro molestias et dolore facere tempora. Soluta qui voluptatem labore at accusamus voluptatibus voluptas. Vel quis rerum deleniti quo sequi quam aliquid. Libero eveniet ex praesentium. Quo aut vel illum distinctio dolore expedita eos.

Quas quos velit qui vero quasi. Sunt delectus sapiente reprehenderit excepturi molestiae saepe esse.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...