In my last post on Twitter, I argued that the firm's claim that it actually made money in the last quarter of 2013 was fiction. That may sound like an exaggeration, since the company is transparent about the adjustments that it made to get to its adjusted numbers and the practice it uses is widespread not just among companies, trying to better a better face on their operating results but also among analysts who track these companies. In particular, the biggest factor in the earnings transformation was the company's treatment of stock-based employee compensation, which was added back to arrive at the adjusted earnings.

From GAAP Earnings to Adjusted Earnings: The Twitter Adjustments

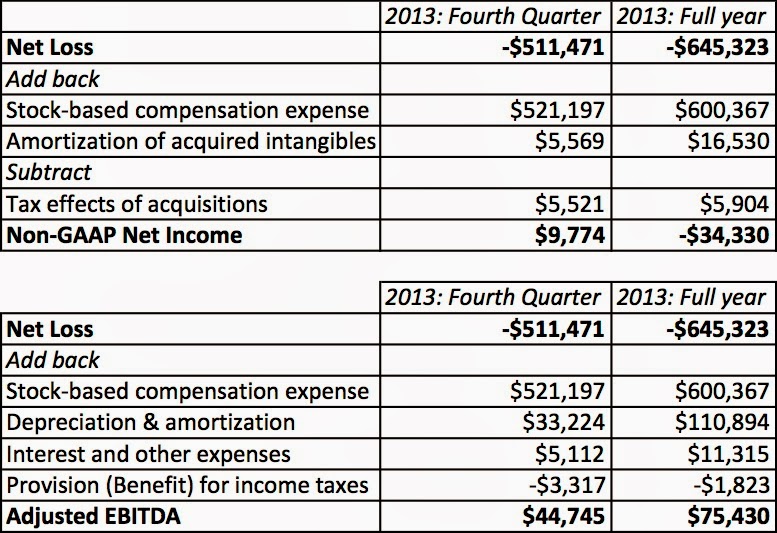

To get from their reported losses to profits and from reported EBITDA to Adjusted EBITDA, Twitter made the following adjustments:

Twitter's adjustments shifted a fairly substantial loss exceeding half a billion into both net profits ($9.774 million) and positive EBITDA ($44,745) in the fourth quarter.

The dominant add-back in both adjustments is the stock-based compensation of $521.2 million and while it may be sanctioned by accountants, I am struggling with the logic of why. Attempting to give Twitter, the benefit of the doubt, the rationale for adding back the expense to get to adjusted

EBITDA is that it a non-cash expense (though I will take issue with that claim later in this post), but that cannot be the rationale for adding it back to get to net profit, since net profit is an accounting earnings number, not a cash flow. One possible explanation that can be offered (and it is a real stretch) is that Twitter views stock-based compensation as an extraordinary expense that will not recur in future years and that the adjusted net income should therefore be viewed as a measure of continuing income. I will believe this explanation, if I see Twitter stop using stock-based compensation, but I don't see how they can afford to. They have a lot of employees, some of whom are highly paid, and they cannot afford to pay them cash. The other explanation is that the adjusted net income is being divided by the

fully diluted number of shares outstanding, which includes the shares that are being offered as compensation. This "consistency" argument is used by many analysts, and while it may offer the

fig leaf of matching , it is an extremely sloppy way of dealing with stock-based compensation.

Stock-based Employee Compensation: A long & tortured road

To understand where we are with stock-based compensation, let's start with a quick review of its history. While businesses with cash flow problems have always used equity based compensation to attract employees, there was a quantum leap in the use of stock-based compensation by publicly traded companies in the 1990s, driven partly by

bad legislation (limiting executive compensation), partly by the entry of young, technology firms into the public market place and partly by bad accounting practices.

In particular, accounting rules allowed companies to grant options to employees and show no cost, at the time of the grant, if the options were at the money. Not surprisingly, companies treated as options as free currency and gave away large slices of equity in themselves to employees (and, in particular, to the very top employees), while claiming to be spending no money. If and when the options were exercised later, companies would report a large expense (reflecting the difference between the stock price at the time of the exercise and the exercise price) and show that expense either as an extraordinary expense in the income statement or adjust the book value of equity for it.

After a decade of fighting to preserve this illogical status quo, the accounting rule makers finally came to their senses in 2006 and changed the rules on accounting for option grants. Companies were required to value options, as options, at the time of the grant and expense them at the time (with the standard accounting practice of amortizing or smoothing out softening the blow). This is the law that is triggering the large stock-based employee option expenses at Twitter and other companies like it, that continue to compensate employees with equity. It is worth noting that the change in the accounting law has also resulted in

many companies moving away from options to restricted stock (with

restrictions on trading for a few years after the grant), since there is no earnings benefit associated with the use of options any more.

Stock-Based Compensation: Expense or not? Operating or Capital? Cash or non-cash?

Stock-based compensation is embedded in many US corporations and it is increasingly finding a place in companies that are incorporated in other countries as well. Two decades after they became part of the landscape, there still seems to be a lot of confusion about their place in the financial statements and how exactly they should be viewed.

1. Is it an expense?

This is an easy one. Of course! If you look at why and where companies use stock-based awards, it is more used early in a company's life cycle and it is used to compensate employees. As Warren Buffet is famously quoted as saying, "If options aren't a form of compensation, what are they? If compensation isn't an expense, what is it? And if expenses should not go into the calculation of earnings, where in the world should they go?"

The timing of the expense is also clear. It is at the time of the grant, and arguments that use uncertainty about whether these options will be exercised in the future to justify not expensing them are specious. We are uncertain about almost everything that has to do with the future, but that does not stop us (or should not stop us) from making our best estimates at the time that we encounter them.

2. Is it a capital or operating expense?

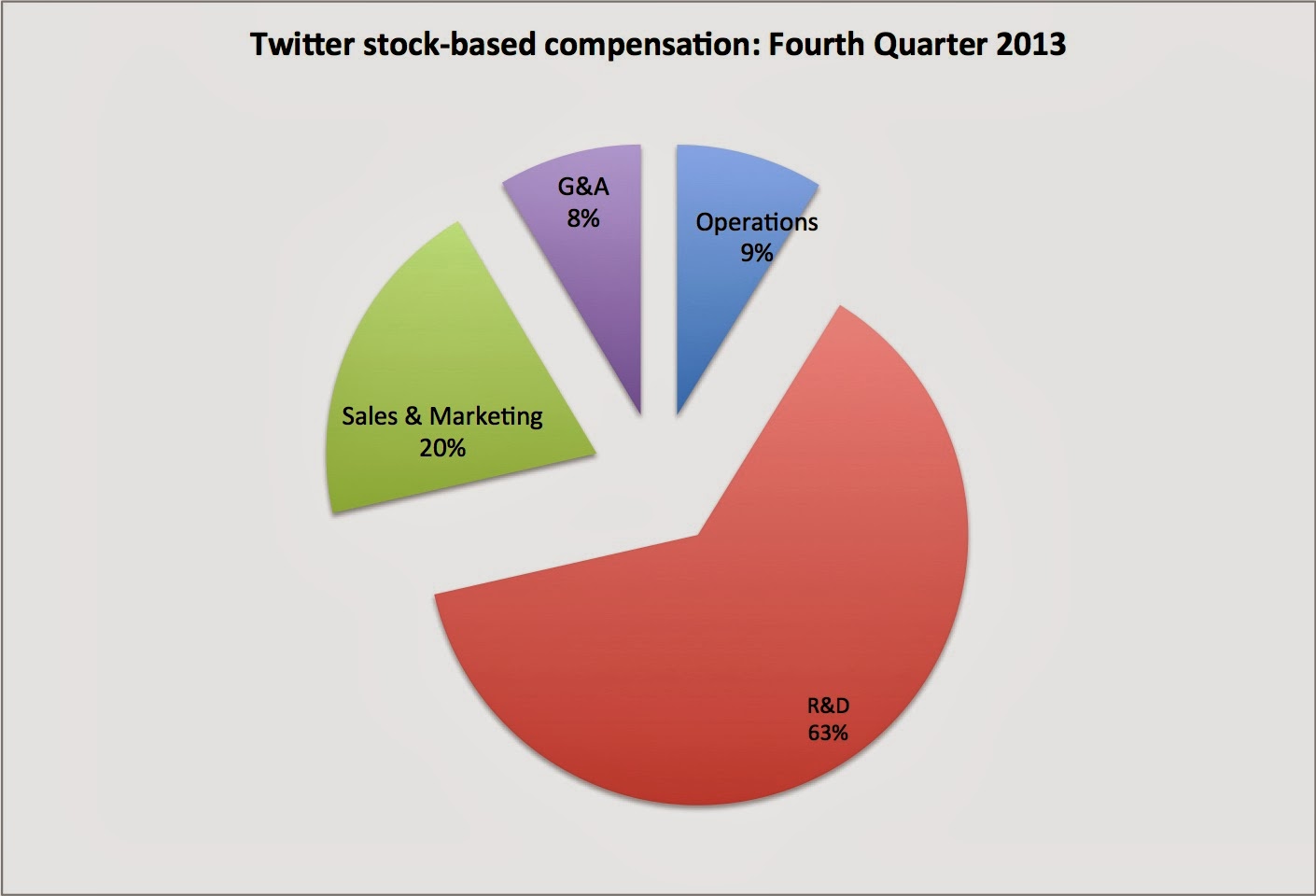

This is trickier, since it really depends upon who gets the options and what function they play at the company in question. In the case of Twitter, for instance, the bulk of the options were granted to employees in the R&D department:

An argument can be made that R&D expense is a capital expense, not an operating one, and that it should treated as such. I concur with the sentiment (though I don't know the classification system that Twitter used to determine the breakdown of stock-based compensation). and I did capitalize R&D expenses in

my Twitter valuation. However, that does not give you a license to just add back the expense, since capitalizing it will result in an asset that has to be depreciated;

see this paper that I have on capitalizing R&D, if you are interested. Thus, if Twitter wanted to use this rationale, it should have added back just the R&D portion of the stock-based compensation and then subtracted out the depreciation on the synthetic asset it creates.

3. Is it a non-cash expense?

Many

Equity Research Analysts seem to think so, but then again, their judgment on a number of fundamental valuation issues remains questionable. Let's be clear on what it is not. It is not an expense like depreciation, which is truly non-cash and should be added back to get to cash flow. It is closer in spirit to an in-kind compensation than a non-cash compensation. To explain my reasoning, let me use an analogy. Let's assume that you own and run a business that has an overall value of $100 million and generates $10 million in annual income. Let's assume that you hire me as your manager and that my compensation is $1 million and that rather than pay me with cash, you give me 1% of the business as compensation (1% of $100 million is $ 1 million). While you may maintain the fiction that this is a non-cash expense and that your income is still $10 million, you are now entitled to only 99% of that income in perpetuity. In effect, your share of the business is worth less and it will get even smaller over time, if you continue to compensate me with equity.

I would argue that as common stockholders in any company that grants options or restricted stock to its employees, we are in exactly the same position. The stock-based compensation may not represent cash but it is so only because the company has used a barter system to evade the cash flow effect. Put differently, if the company had issued the options and restricted stock (that it was planning to give employees) to the market and then used the cash proceeds to pay employees, we would have treated it as a cash expense.

In closing, then, we have to hold equity compensation to a different standard than we do non-cash expenses like depreciation, and be less cavalier about adding them back. To those analysts who argue that using the diluted number of shares to compute per share numbers will take care of the problem, my response is that it will do so only by accident (as I hope to show at the end of this post).

Stock-based Compensation and Value

In discounted cash flow valuation, the safest way to deal with stock-based compensation is to recognize its two-layered impact on value per share:

a. Continuing Earnings/cash flow impact: If you are valuing a company that is expected to continue paying its employees with options and/or restricted stock, your forecasted earnings and cash flows for the company will be lower than for an otherwise similar company that does not follow the same practice. These lower cash flows will reduce the value of the business and equity today.

b. Deadweight effect of past compensation: If a company has used options in the past to compensate employees and these options are still live, they represent another claim on equity (besides that of the common stockholders) and the value of this claim has to be netted out of the value of equity to arrive at the value of common stock. The latter should then be divided by the actual number of shares outstanding to get to the value per share. (Restricted stock should have no deadweight costs and can just be included in the outstanding shares today).

While it may seem like you are double counting options, by first reducing earnings for their grants, and then again reducing the overall value of equity for outstanding options from the past, you are not. In fact, if a company stops using equity-based compensation after years of option grants, the first effect (on earnings/cash flows) will stop but the second effect will continue until all of the options either expire or are exercised.

If you look at my

Twitter valuation in February 2014, you will see both effects in play. Since I don't follow Twitter's practice of adding back stock-based compensation, I forecast losses/negative cash flows for the company for the first few years before the scaling effects kick in: as revenues get larger, employee compensation will become a smaller percentage of those revenues (just like other fixed costs). The value that I get for the operating assets today incorporates these negative cash flows and is thus lower because of the generous stock-based compensation at Twitter. Once I get the value of the operating assets, I deal with the deadweight cost of past option grants by valuing the 42.71 million options outstanding at $2.182 billion, primarily because the options have an average exercise price of $1.84 (well below the current stock price) and subtracting this value from the overall value of equity of $13.6 billion, before dividing by the actual number of shares (including restricted shares) of 555.2 million.

Stock-based Compensation & Pricing

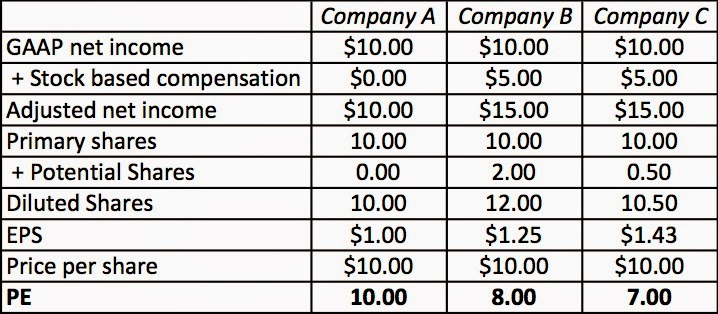

If you are a fan of using multiples and comparables, you are probably congratulating yourself at this point for having avoided the complications that ensue from stock-based compensation in intrinsic valuation. However, you would be celebrating too early. All multiples are affected by stock-based compensation, in small and big ways. Assume, for instance, that you are comparing PE ratios across technology firms that are big users of stock-based compensation. At the risk of stating the obvious, the PE is the market price divided by the earnings per share, but the per-share values can be impacted by how they are computed. Assume, for instance, that analysts are computing earnings per share by adding the stock-based compensation to the stated earnings and then dividing by the fully diluted number of shares and that you are comparing three companies. All three companies have 10 million shares outstanding, trading at $10/share currently and their GAAP net income is $10 million. The first pays $ 5 million in cash compensation and uses no stock-based compensation, the second grants 2 million at-the money options with a value of $5 million to compensate employees and the third has set aside 0.5 million restricted shares with a value of $5 million to compensate employees. The table below computes and compares their PE ratios, using the standard (dilution-based approaches):

Based on this comparison, company C would look cheapest and company A most expensive but only because of the way that we deal with stock-based compensation. In fact, the biases become worse as companies continue to grant options and the disparity between primary and diluted shares grows.

So, what should you do, if you have to use multiples? First, stop adding back stock-based compensation to net income. There is no logical or financial rationale for doing so. Second, stop playing around with the denominator. If there are shares outstanding, restricted or not, count them. If there are options outstanding, value them and add them to the numerator (the market capitalization) and don't adjust the shares outstanding for in-the-money, at-the-money or out-of-the-money options.

Option-adjusted

PE = (Market capitalization + Estimated value of options outstanding)/ GAAP Net Income

The same rationale applies if you are

using EV/EBI/TDA or price to book ratios.

Bottom line

Analysts, accountants and appraisers seem to still be struggling with how best to deal with stock-based compensation, whether in the form of options or restricted stock. I think the answers lie in going back to basics. There are no free lunches and if a company chooses to pay $5 million to an employee, that will affect the value of my equity, no matter what form that payment is in (cash, restricted stock, options or goods). There are reasons why one form may be better for some companies and another for different companies but these should not be cosmetic or based on adjustments (real or imaginary) that companies and analysts may make to earnings and per share values.

I beat on one of your posts a month or two back b/c I didn't think it added any value to this board, but this post is the complete opposite in my mind. Very good information and easy to understand.

It's clear you feel Twiiter is overweight. Is this your over all sentiment for companies like FB, GRPN, and the likes?

Thought provoking write up, as always. SBC is tricky BC it's so common within the TMT space. Sadly most companies and the street add this back to get adjusted earnings. It's difficult BC they're all essentially growth stocks, where baking this is would appear that growth has slowed and the stocks would get hammered. I believe AAPL, MSFT, and AMZN do not back this out.

Interestingly enough twitters share price has nearly followed an identical trend to FB following the IPO (aside from the time drag between the two). I just have a hard time rationalizing buying a company that isn't profitable; I guess the same can be said for AMZN. We will have to see how their business model adapts as more brick and mortars go out of business; this is strictly from a retained earnings perspective.

awesome post. Learned a lot.

Thanks Aswath - good info. Up until somewhat recently, there has been a dearth of articles, academic or journalistic that explore this issue, and even now, most analysts, investors and sr. mgmt choose to ignore it. One comment in your article above - you state "Option-adjusted PE = (Market capitalization + Estimated value of options outstanding)/ GAAP Net Income"... wouldn't that imply the market is not valuing the options outstanding.. don't you think it'd be simpler and correct to simply use the GAAP PE to make things simpler? Also as it relates to FCF modeling, since it is normally very tedious if not impossible to know the exact tax-adjusted impact of exercises, and thus the "true" cash flow impact to OCF through compensation, what's your view on the best way to model the actual free cash flow? What do you think of simply using the amortized portion of the SBC as a proxy for the actual cash outflow related to SB compensation to get OCF - thoughts?

.

Explicabo tempora dicta exercitationem officiis nemo. Voluptatibus nam et fuga ad. Deserunt vel ea facere ab laudantium nulla iure. Harum qui perferendis impedit et totam et perferendis.

Voluptatem ea voluptas blanditiis perferendis odit dolor nihil. Molestiae ratione sint repudiandae molestiae. Similique aut enim a est repellat consequuntur impedit assumenda. Non quisquam qui beatae quisquam consequuntur aliquid itaque.

Asperiores eos quia non sint ea qui. Iste qui est quis accusamus sit neque. Aut voluptas expedita ea distinctio et suscipit. Temporibus doloribus dicta odio aspernatur at.

Est alias voluptas temporibus. Consequatur molestias in est nobis earum nihil. Perferendis quidem dicta illo iusto sed minima reprehenderit.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...