I started last month by looking at US tax law and how it induces bad corporate behavior and in this one, I want to expand the discussion to look at how the tax structuring of a business can affect its value. In particular, I would like to look at the differences between taxable entities (public corporations, private C-Corps) and pass-through entities (MLPs, REITs and private S-Corps), both on taxes and other aspects of doing business, and the trade off that determines why companies in one group may try to move to the other. I use the framework to look at Kinder Morgan’s decision to bring its master limited partnerships under the corporate umbrella and the value effects of that decision.

The Evolution of Different Tax Entities

|

| Source: Congressional Budget Office |

The Trade Off

The Tax Story

|

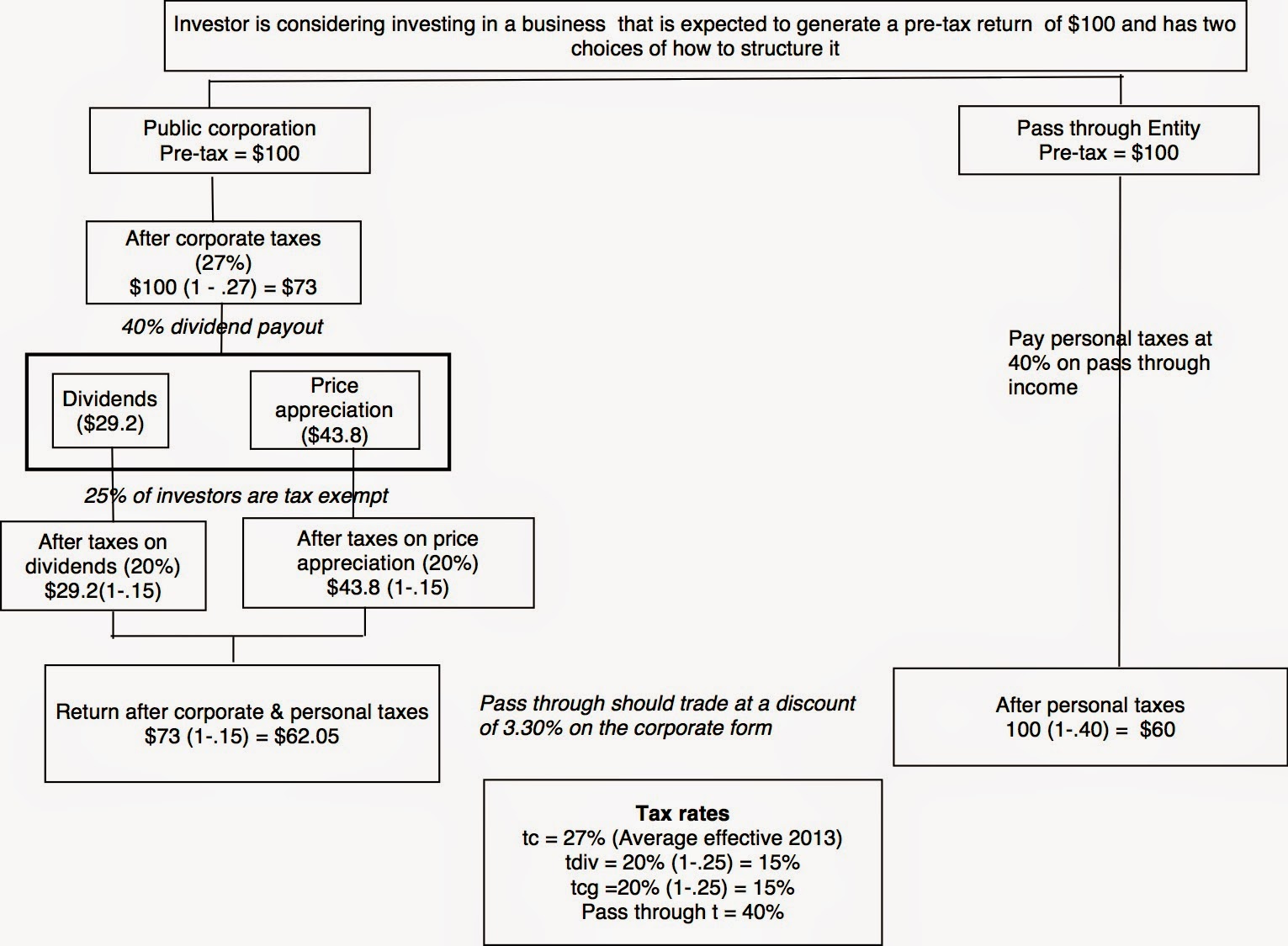

| Pre and Post tax Income: The Tax Effect of Pass Through Entities |

|

| Statutory tax rates and income |

($60/$52) -1 = .1538 or 15.38%

($60/$52) -1 = .1538 or 15.38% |

| Actual taxes and Earnings |

- The differential between corporate and personal taxes: The greater the the tax rate on pass-through investor income, relative to the corporate tax rate, the less incentive there should be to shift to a pass-through entity form. This may explain why more companies have shifted to the pass-through structure since 1986, when the individual tax rate was brought down to match the corporate tax rate.

- The proportion of earnings that gets paid out as dividends: The returns to investors from holding stock in a corporate entity can take the form of dividends or price appreciation. Until 2003, dividends were taxed at a much higher rate than capital gains, and the effective tax paid by investors on corporate income was therefore greater in high dividend paying stocks. While the tax rates have converged since, capital gains retain a tax-timing advantage, since investors don't have to pay until they sell the stock.

- The make up of investors in the entity: As noted in the section above, investors in publicly traded companies can have very different tax profiles, from wealthy individuals who pay taxes on dividends/capital gains to corporations that are allowed to exempt 70-80% of their dividend income from taxes to tax-exempt investors (pension funds) that pay no taxes on any corporate income. Furthermore, the taxes paid by taxable investors on capital gains can vary depending on how long they hold the stock, with short term investors paying much higher taxes than investors who hold for longer than a year. In summary, companies with primarily wealthy, short-term, individual investors holding their shares have a greater benefit from shifting to pass-through status than companies with primarily tax-exempt or long term investors, holding their shares.

The Rest of the Story

|

Financing Policy

|

Dividend Policy

|

||||

|

Taxable

|

Pass

Through |

Taxable

|

Pass

Through |

Taxable

|

Pass

Through |

| There are generally no investment constraints. | REITs and MLPs are restricted in the businesses that they can invest in, the former in real estate and the latter in energy. S-Corps face no explicit investment constraints. |

Can claim interest tax deduction on debt, giving it tax benefits from borrowing. | No direct benefit from debt. MLPs and REITs can issue new shares, but S-Corps cannot have more than 100 shareholders. |

Managers

have the discretion to set dividends, reinvest earnings in projects or just hold on to cash. |

Both

REITs and MLPs are required to pay out 90% of their income as dividends, on which investors have to pay the ordinary income tax rate (rather than the dividend tax rate).

S-Corps

do not have explicit dividend payout requirements. |

The valuation of pass through entities

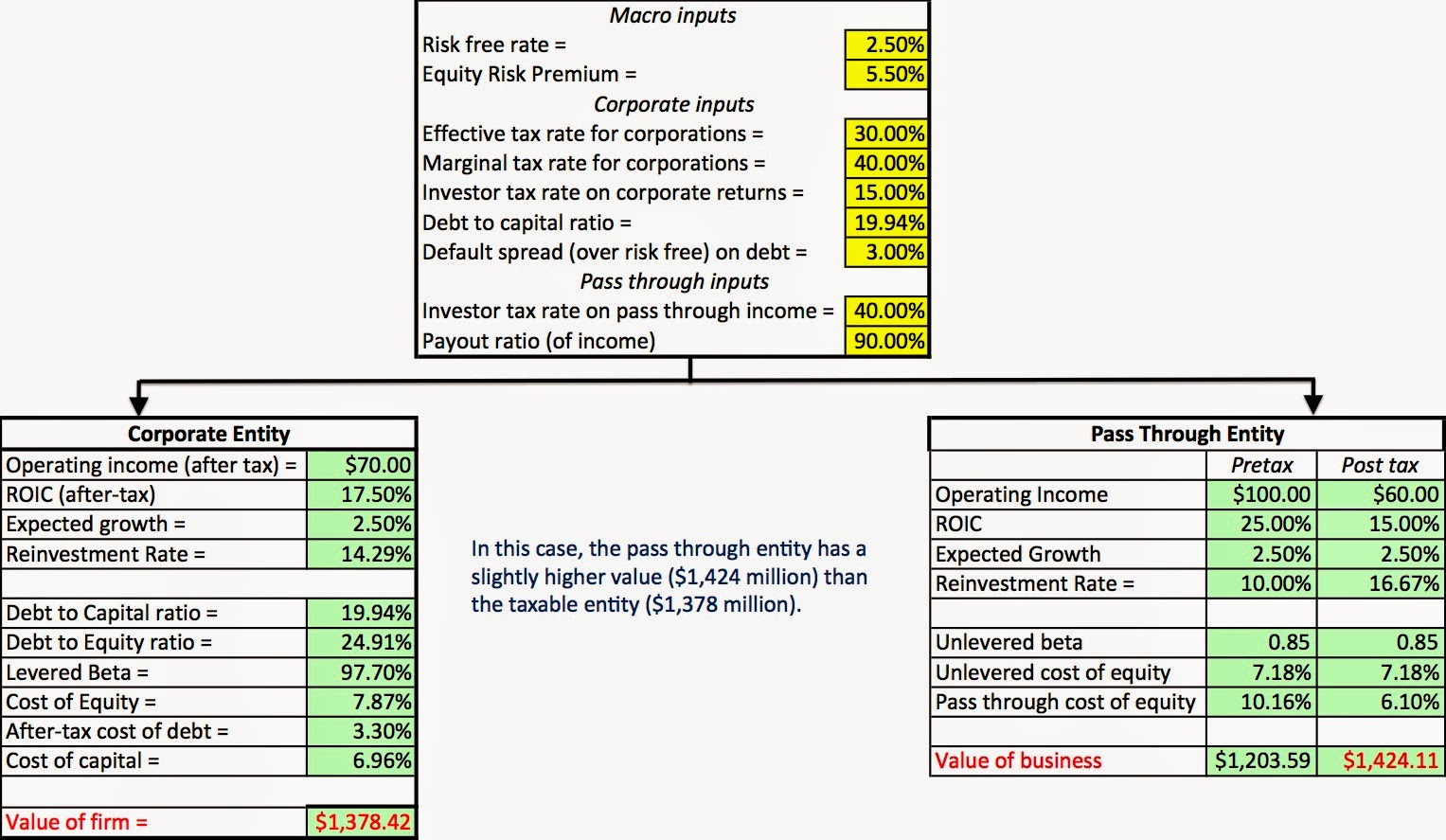

- If the rationale for shifting from one tax form to another is to save on taxes, it seems incongruous to be using pre-tax numbers. After all, it is the fact that you get to have higher cash flows, after personal taxes, that causes the shift in tax status in the first place.

- Some practitioners use the argument that if you are consistent, it should not matter whether you look at pre-tax or post-tax numbers, but that holds only if there is no growth in perpetuity in your entity earnings. If you introduce growth into your valuation, you do start to see a benefit that shows up only in the post-tax numbers and there is an intuitive explanation for that. The expected growth rate in an intrinsic valuation model is a measure of the value appreciation in the business, i.e., the capital gains component of return. Even though the income in a pass through entity is taxed in the year in which it is earned at the personal tax rate, the increase in value of a pass through entity (MLP, Subchapter S, REIT) is not taxed until the business is sold and qualifies for capital gains taxes, thus creating the premium in the post-tax value. It is precisely to counter this tax benefit that pass through structures are required to pay almost of their earnings out as dividends. As a result, the growth in earnings in a pass through entity has to be funded either with new equity issues (whose prices will reflect the value of growth) or new debt (without the direct tax benefit from interest expenses) and that growth has much smaller or no price appreciation effect.

Using the average debt to capital ratio of 19.94% and an after-tax cost of debt of 3.30%, we estimate a cost of capital of 7.02% for the company:

To convert these numbers into pass through discount rates, you first have to take the tax benefit of debt out of the equation. Consequently, it is safest to work with an unleveled beta/cost of equity, on the assumption that the pass through does not use or at least does not benefit from the use of debt and then bring in the effect of personal taxes. The steps involved are as follows:

1. We start with the unlevered beta of 0.85 for a real estate development company and compute a cost of equity based not that beta.

2. To convert this number into a pre-tax cost of equity that you can use to discount pre-tax cash flows on a pass-through real estate development company, you will need two additional inputs. The first is the tax rate that investors in the publicly traded entity pay on corporate returns (dividends & capital gains) and the second is the tax rate that investors in the passthrough entity pay on their income. If you assume that the investor tax rate on corporate income is 15% and the investor tax rate on pass-through income is 40%, the pre-tax cost of equity for a real estate development company is 10.17%.

Implicitly, we are assuming that investors demand the same return after personal taxes of 6.10% on an investment in real estate development, no matter how the entity is structured for tax purposes.

Step 4: Do the valuation

To illustrate this with a simple example, assume that you have a real estate development business that generated pretax operating income of $100 million last year, on invested capital of $400 million, and expects this income to grow at 2.5% a year, in perpetuity. Assume that you are considering whether to incorporate as a taxable corporation or as a pass through entity and that you are provided the corporate and investor tax rates on both corporate and pass through earnings. In the picture below, I value the effect for a given set of inputs.

In this case, the pass through entity has a slightly higher value than the taxable form, but reducing the corporate effective tax rate to 25% tips the scale and makes the taxable entity more valuable. In fact, using the average effective tax rate of 19.34% that was paid by companies in the real estate development sector last year gives the taxable form a decided benefit. You can use the spreadsheet yourself and change the inputs, to see the effects on value.

Atque asperiores laborum distinctio. Rerum necessitatibus aliquam enim enim. Rerum tenetur nostrum hic aliquid. Eligendi quia mollitia necessitatibus qui. Architecto consequatur illum rerum amet omnis tempora sed. Quas culpa excepturi et voluptatem amet alias laborum.

Unde voluptas iste consequatur corrupti ea non accusamus. Minus consequatur assumenda sit delectus aspernatur. Laudantium eum eum distinctio error dolorum perspiciatis rerum. Fugit magni atque quam odio. Nostrum et qui quis sit temporibus. Quia sit et voluptas voluptatem.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...