Operating Cash Flow

The amount of cash generated by the operating activities of a business.

Abbreviated as OCF, Operating Cash Flow is the amount of cash generated by the operating activities of a business. It represents if the company has a positive or negative cash flow from business operations. This can be found on a statement of cash flows included in a 10-K or 10-Q statement.

Another way to look at OCF is to measure the cash generated by a company's regular business operations.

A favorable operating cash flow indicates a company can maintain and grow operations, whereas if negative, it suggests that the company might not be able to maintain its existing operations.

OCF is a critical metric to consider as it shows how much a company can pay for its current liabilities. Using the cash it generates from its operations also indicates whether a company can meet its financial obligations and service its debt.

A company that generates high levels of OCF may be better positioned to take on more debt. It suggests they can finance capital expenditures and make acquisitions without the need for equity financing.

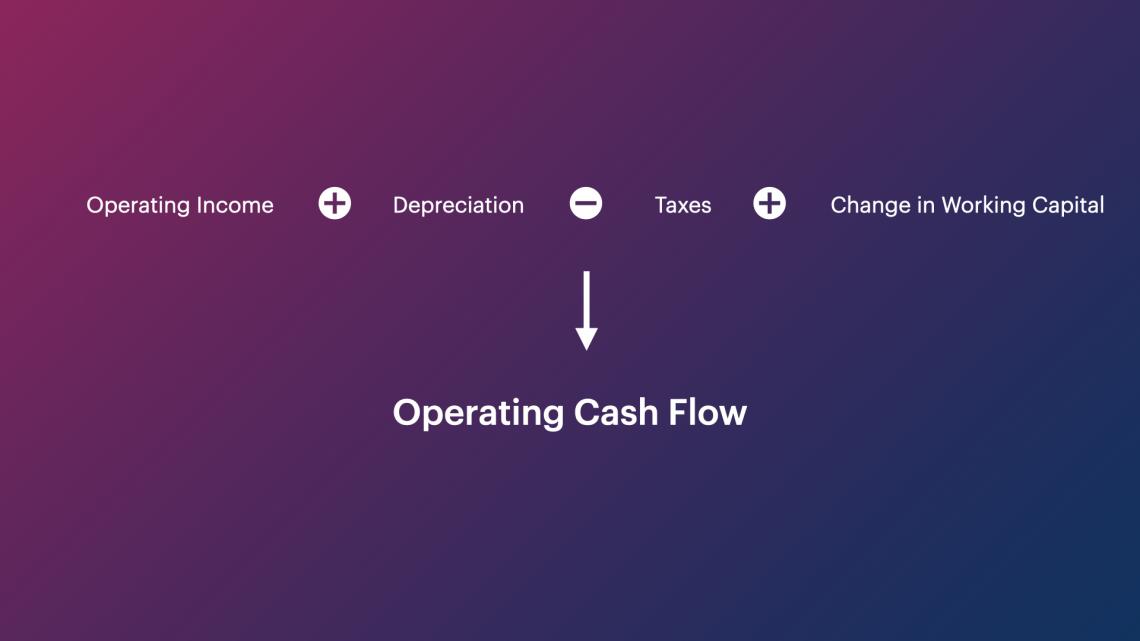

You can derive the OCF by adding a company’s non-cash expenses to its net income and adjusting for changes in working capital (current assets minus current liabilities).

However, it also suggests that businesses with low levels of operating cash flow may have difficulty meeting financial obligations. They may need equity financing to expand or cover operating expenses.

Components

Many components go into the calculation. Here are the most important components:

1. Net income

This is the top line of OCF. It is sales minus the cost of goods sold, expenses, taxes, and interest.

2. Stock-based compensation

It refers to the awards a company gives its employees in the form of equity ownership. This is subsequently added back to the OCF.

3. Depreciation

Depreciation of property and equipment is also added to net income when finding operating cash flow. This is because depreciation is simply an accounting technique designed to spread the cost of an asset over its life.

4. Other operating expenses

Other operating expenses include expenses that are not directly related to production. This includes rent, marketing, and office expenses, among additional costs.

They are also referred to as overhead expenses. Other operating expenses are added to net income when finding operating cash flow.

5. Changes in operating assets and liabilities

Changes in operating assets and liabilities can be added or subtracted from net income when calculating OCF. Managing support and penalties include:

- Inventory- raw materials used to produce goods and goods that are available for sale.

- Accounts receivable- funds owed to a company for goods or services that have already been sold.

- Accounts payable- funds payable to suppliers for products received but not yet paid off.

- Accrued expenses- an expense that has been recognized but not yet paid.

- Unearned revenue- cash acquired by the company for a good or service that has yet to be provided.

Example

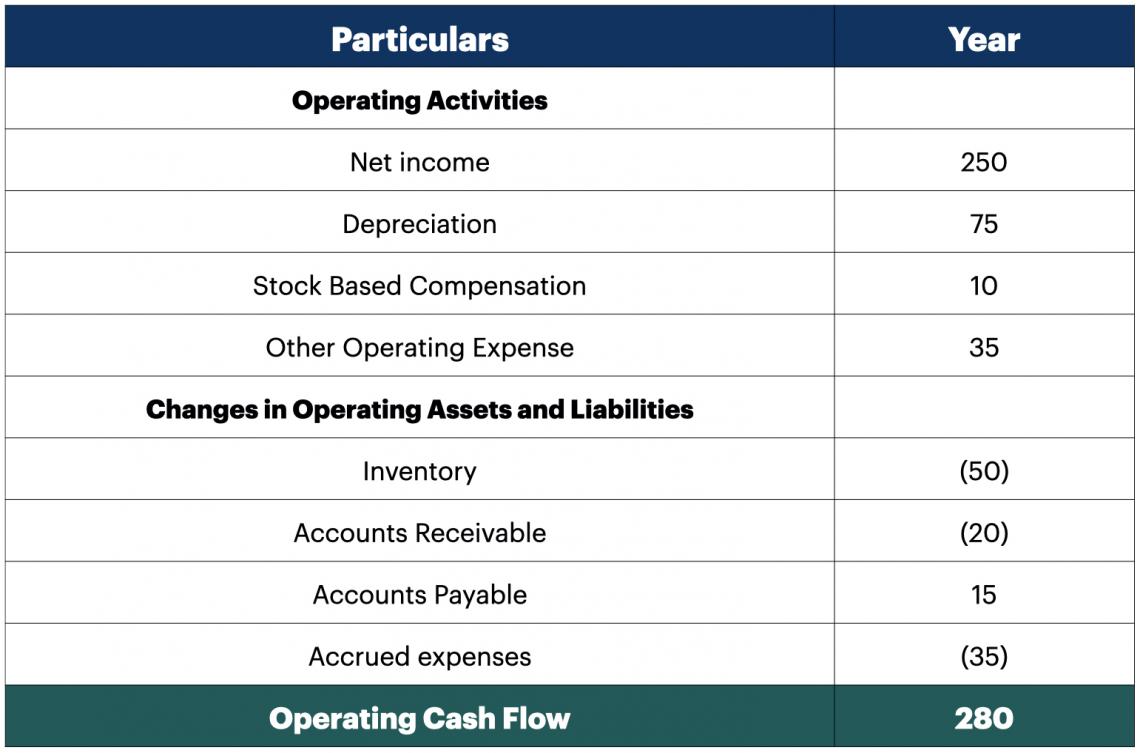

For the year 2022, Company X had a net income of $250. It paid out $75 to its employees through stock-based compensation in 2022. Accumulated depreciation came out to $10 for the year.

Other operating expenses amounted to $35. There were increases in inventory, accounts receivable, and accrued expenses of $50, $20, and $35, respectively. Finally, there was a decrease of $15 in accounts payable.

To determine company X’s OCF, you can add its non-cash expenses to its net income.

The non-cash expenses were stock-based compensation, accumulated depreciation, and operating expenses. Adding these three together, you get $120. Then adding the non-cash expenses to the net income is $370.

Finally, there should be adjustments for changes in working capital. To find working capital changes, subtract inventory, accounts receivable, and accrued expenses by accounts payable. This would give a value of -$90.

Therefore, company X has an OCF of $280 ($370-$90). Above is a visualization of the calculation for 2022.

What is the cash flow statement?

The cash flow statement is a financial statement that summarizes the changes in cash that come and go from a company and is one of the three major financial statements. Broadly speaking, the cash flow statement is separated into three distinct business activities:

- Investing activities

- Financing activities

- Operating activities

Cash flow from investing activities covers the inflows & outflows of money related to investments. Items such as the purchase or sale of assets would be covered under investing activities in the cash flow statement.

Cash flow from financing activities accounts for all cash flows used to finance the company.

You can think of it as the inflow and outflow of money surrounding shareholders and lenders, which also reflect major financing decisions made by the company. It covers items such as dividends, loan payments, stock repurchases, etc.

Cash flow from operating activities is cash flow from all activities related to business operations. Cash flow from operating activities starts with net income, accounting for changes in working capital and depreciation.

A sample cash flow statement for Amazon's (AMZN) 2020 10-K report is included below.

A cash flow statement is essential to a company's profitability and financial health. Generally, investors refer to the cash flow statement to help determine whether a company can meet its long and short-term liabilities.

Indirect vs. direct operating cash flow

There are two methods for finding OCF (indirect and direct methods). You would be tracking all cash inflows and outflows using the direct method. This method uses cash payments and receipts to find the operating cash flow.

In the direct cash flow method, cashless transactions are omitted, and only cash transactions are considered. Payments made in cash and cash received are some examples of cash transactions.

The earlier example above demonstrates the indirect method. It uses accrual-based accounting where non-cash expenses are added to net income and adjusted for working capital changes. This is the more common method used by accountants.

Although there are differences between the direct and indirect methods, they should theoretically produce the same OCF. While the direct method is more intuitive, it is also more time-consuming.

Because the direct method is time-consuming, most companies prefer utilizing the indirect method.

OCF and a company’s financial health

OCF is an essential indicator of a company's financial health.

Not only does it show the amount of cash generated by a company's regular business operations, but it also indicates whether a company can generate positive cash flow to maintain and grow its operations. Otherwise, it may need external financing for capital expansion.

A high OCF means the company has positive earnings and can repay short-term debts. Low OCF could show that the company cannot meet its short-term obligations, which can cause concern.

When it is low, it could be related to a lack of sales or an increase in inventory levels. This would lead to lower profits and more spending on inventory rather than other areas like marketing costs or advertising expenses.

One drawback of OCF is that it does not give a total picture of financial health. This is because it does not factor in long-term expenditures and financing activities.

While operating cash flow is useful, it must be used along with other financial metrics to get an overall picture of a company’s financial health.

Operating cash flow vs. net income vs. free cash flow

OCF is a measure of the amount of cash generated by a company's normal business operations- it highlights the ability of a company to cover its operating expenses.

Net income indicates the profit or loss the company has made in one fiscal year. It represents the total net income after taxes and minority interest deducted from revenue.

However, net income is not a good measure of financial health because it fails to account for many aspects of its balance sheet, including long-term debt, depreciation, and deferred taxes.

Free cash flow represents the cash remaining after operating expenses and capital expenditures. It shows the money remaining after a company covers all its costs and taxes.

Generally, free cash flow is used to pay dividends, perform share buybacks, finance acquisitions, and other expenditures if the company is looking to grow.

You subtract capital expenditures from operating cash flow to find free cash flow. The higher the free cash flow, the more it can pay dividends and use for company expansion.

A lower or declining free cash flow can signify a company is struggling to generate cash. Investors use free cash flow to gauge financial health.

Both net income and free cash flow are metrics to understand profitability. Similar to operating cash flow, they can tell investors about a company's ability to pay off operating expenses. However, both net income and free cash flow account for capital expenditures.

Therefore, net income and free cash flow are considered better measures of total profitability and financial health. At the same time, OCF gives a better picture of a company's ability to cover its expenses related to direct business.

Evaluating OCF

Investors and lenders alike use operating cash flow when evaluating a company. It provides lots of information about a company’s profitability and liquidity.

Also, it is used as a benchmark for the company's ability to repay debt, pay dividends and expand its operations. All this information is helpful to investors when deciding whether to invest in a company or not.

When determining the creditworthiness of companies, lenders will look at their OCF because it can tell lenders about the company’s ability to pay their necessary expenses.

A company with a high OCF is more likely to be approved for loans, while a company with a low or negative OCF will find it more difficult to borrow from lenders.

Other metrics, such as the operating cash flow ratio, can be calculated after deriving the OCF.

Without going into much detail, a ratio greater than 1.0 is desired because a company can pay off all its liabilities using the cash flow it generates from operations.

An OCF ratio of less than 1.0 signifies a company cannot pay off all its current liabilities.

Therefore, investors are often skeptical about companies with an OCF ratio below 1.0 because it may signify financial distress.

Using OCF to value a company's profitability and liquidity is helpful. However, it is important to realize that it does not give a total picture of a company's financial health.

Therefore, while OCF helps find information about a business's core operations, it must be used with other metrics.

Researched and Authored by Liam

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?