In the last six posts, I have tried to look at the global corporate landscape, starting with how the market is pricing risk in the US and globally, how much investors are getting as risk free returns in different currencies and then moving on to differences across companies on the costs of raising funding (it varies by sector and region), the quality of their investments (not that good) and their indebtedness (high in pockets). In this, the last of these posts, I propose to look at the final piece of the corporate finance picture, which is how much companies around the world returned to stockholders in dividends (and stock buybacks) and by extension, how much cash they chose to hold on for future investments.

Dividends, Potential Dividends and Cash

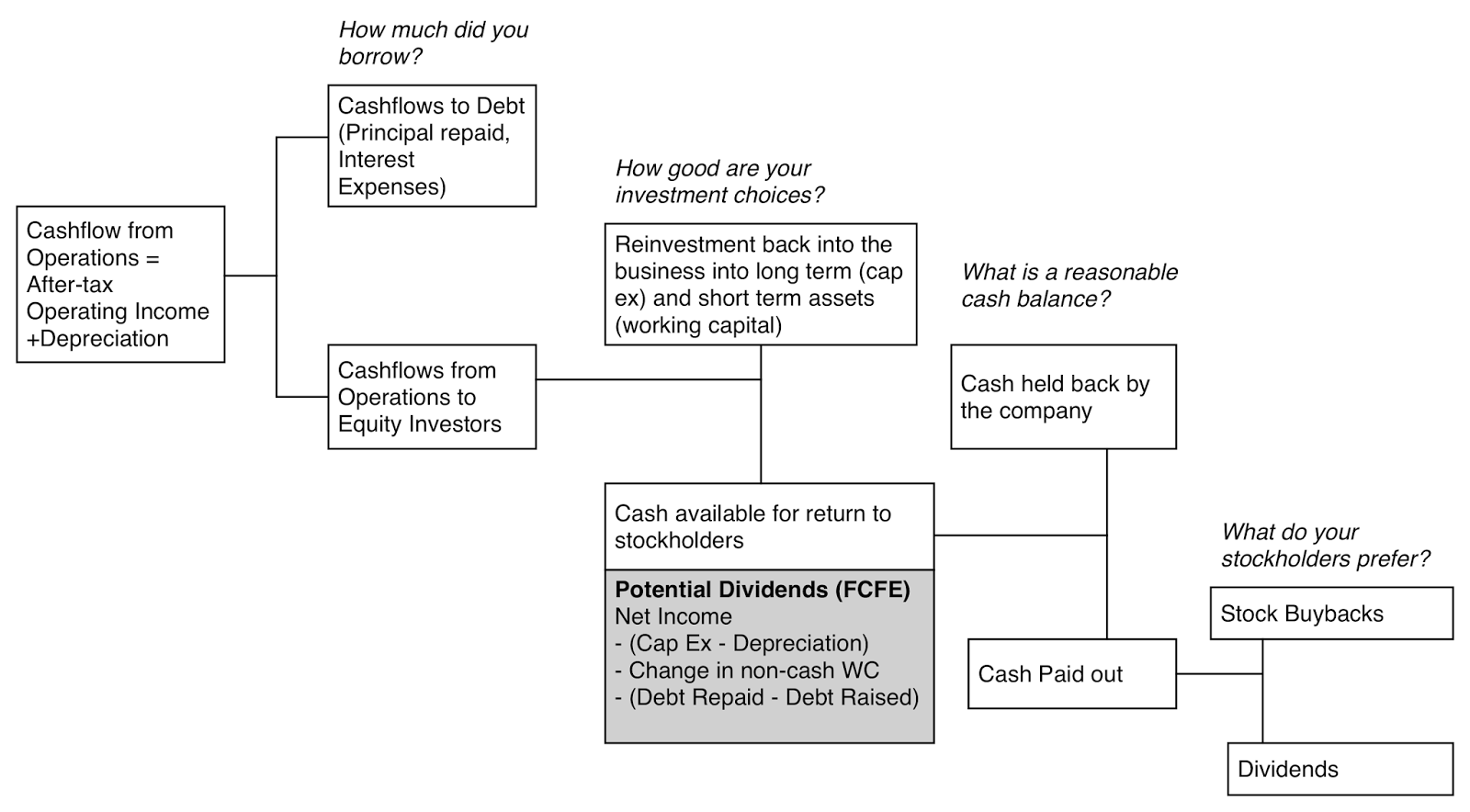

Dividend policy is often the ignored step child of corporate finance, treated either as an obligation that has to be met by companies or as a sign of weaknesses by those who believe that companies exist only to build factories and invest resources. The reality is that dividends are a central reason for investing and unless cash gets returned to investors, and I am willing to expand my notion of dividends to include buybacks, there is no real payoff to investing. That said, the question of how much a company can pay in dividends is affected in most businesses, by investing and financing choices. If equity is a residual claim, as it is often posited to be, dividends should be the end-result of a series of decisions that companies make:

If you accept the logic of this process, companies that have substantial cash from operations, access to debt and few investment opportunities should return more cash than companies without these characteristics.

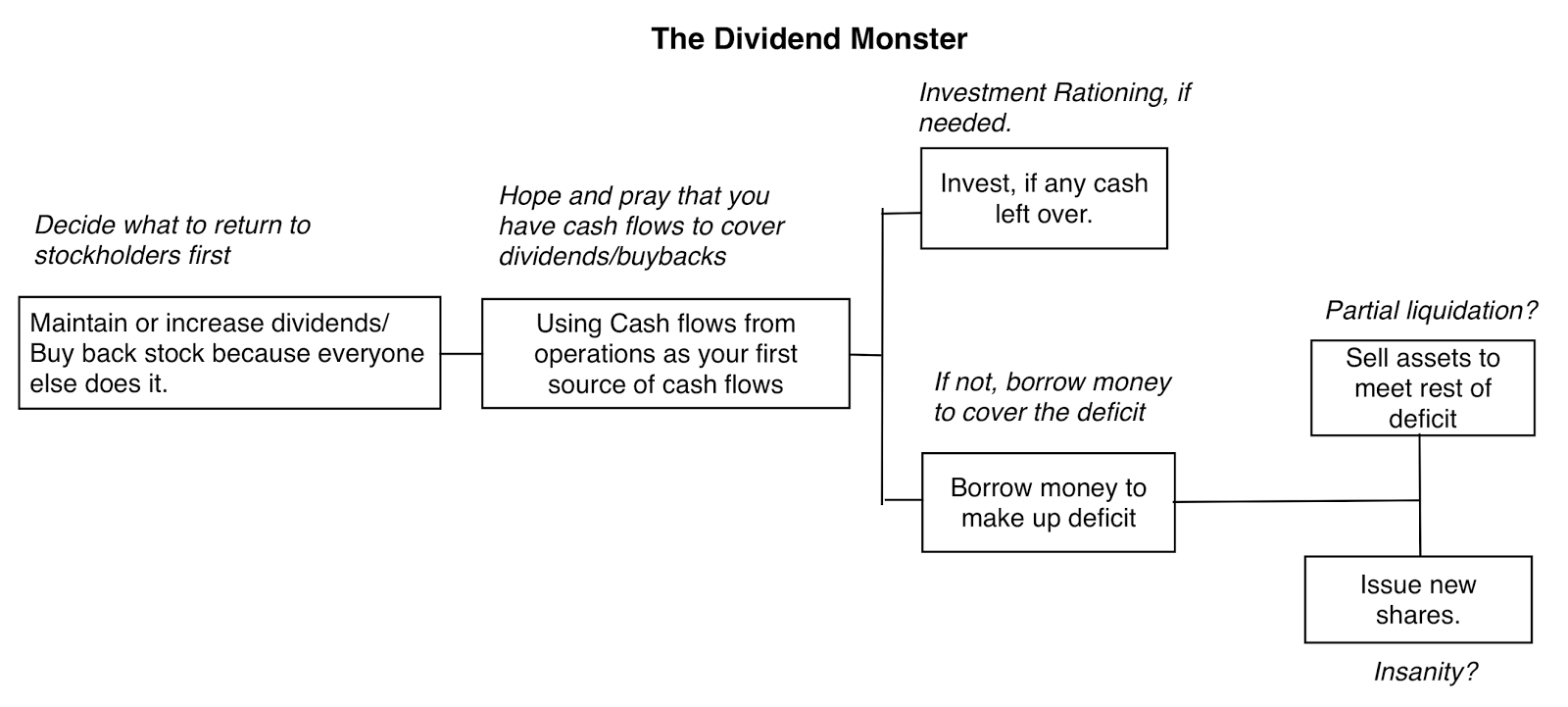

In practice, the sequencing is neither this clean, nor logical. Dividend policy, more than any other aspect of corporate finance, is governed by inertia (an unwillingness to let go of past policy) and me-too-ism (a desire to be like everyone else in the sector) and as a consequence, it lends itself to dysfunctional behavior. In the first dysfunctional variant, rather than be the final choice in the business sequence, dividends become the first and the dominant part driving a business, with the decision on how much to pay in dividends or buy back in stock made first, and investment and financing decisions tailored to deliver those dividends.

Not surprisingly, dividends then act as a drain on firm value, since companies will borrow too much and/or invest too little to maintain them. In a diametrically opposite variant, managers act as if they own the companies they run, are reluctant to let go of cash and return as little as they can to stockholders, while building corporate empires.

These companies can afford to pay large dividends, choose not to do so and end up, not surprisingly, with huge cash balances. It is worth noting that the corporate life cycle, a structure that I have used repeatedly in my posts, provides some perspective on how dividend policy should vary across companies.

Dividend Policies across Companies

As with my other posts on the data, I started by looking at the dividends paid by the 41,889 companies in my sample, with an intent of getting a measure of what constitutes high or low dividends. So, here were go..

1. Measures of dividends: There are two widely used measures of dividends. The first when dividends are divided by net income to arrive at a dividend payout ratio, a measure of what proportion of earnings gets returned to stockholders (and by inversion, what proportion gets retained in the firm). The distribution of dividend payout ratios, using dividends and earnings from the most recent 12 months leading into January 2016, is captured below:

|

| Source: Damodaran Online |

Note that more firms (23,022) did not pay dividends, than did (18,867), in 2015. Among those companies that paid dividends, the median payout ratio is between 30% and 40%.

The other dividend statistic is to divide dividends paid by market capitalization (or dividends per share by price per share) to estimate a dividend yield, a measure of the return that you as a stockholder can expect to generate from the dividends, on your investment. The rest of your expected return has to come from price appreciation. Again, using trailing 12-month dividends leading into and the price as of December 31, 2015, here is the distribution:

As with the payout, the yield is more likely to be zero than a positive number for a globally listed company, but the median dividend yield for a stock was between 2% and 3% in 2015.

2. The Buyback Option: For much of the last century, dividends were the only cash flows that stockholders in corporations received from the corporations. Starting in the 1980s, US companies have increasingly turned to a second option to returning cash to stockholders, buybacks. From an intrinsic value perspective, buybacks have exactly the same consequences to the company making them, as dividends, reducing cash in the hands of the company and increasing cash in the hands of stockholders. From the stockholders' perspective, there are differences, since every stockholder gets dividends (and has to pay taxes on it) while only those who sell their shares back get cash with buybacks, but leave the remaining stockholders with higher-priced stock. In the table below, I look at the proportion of the cash returned that took the form of buybacks for companies in different regions in the twelve months leading into January 2016:

While it is true that US companies have been in the forefront of the buyback boom, note that the EU and Japan are not far behind. Buybacks are not only here to stay, but are becoming a global phenomenon.

3. The Cash Balance Effect: Any discussion of dividends is also, by extension, a discussion of cash balances, since the latter are the residue of dividend policy. In this final graph, I look at cash balances at companies, as a percent of the market capitalizations of these companies.

You may be a little puzzled about the companies that have cash balances that exceed the market capitalizations, but it can be explained by the presence of debt. Thus, if your market capitalization is $100 million and you have $150 million in debt outstanding, you could hold $150 million of that value in cash, leaving you with cash at 150% of market capitalization.

Industry Differences: The Me Too Effect

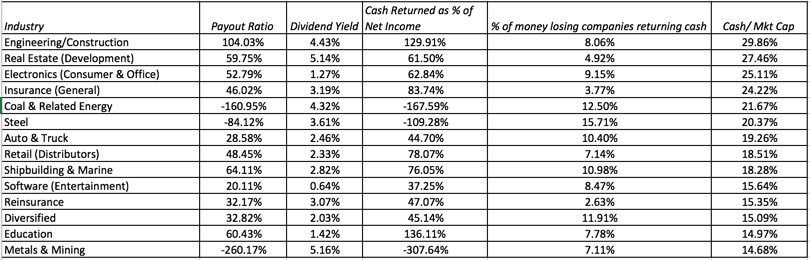

If a key driver of dividend policy is a desire to look like your peer group, it is useful to at least get a measure of how dividend policy varies across industries. Using my 95 industry groups as the classification basis, I looked at dividend yields and payout ratios, as well as the proportion of cash returned in buybacks and cash balances, and you can download the data here. While there are many measures on which you can rank industries on dividend policy, I decided to do the rankings based on the cash balances, as a percent of market capitalization, because it is the end result of a lifetime of dividend policy. In the table below, I list the 15 industries that have the lowest cash balances, as a percent of market capitalization, in January 2016.

While this is a diverse listing, most of these industries are in mature businesses, where there is little point to holding cash and one reason for the low cash balances is that many of the companies in these sectors return more cash than they have net income.

At the other end of the spectrum are industries, where cash accumulation is the name of the game. Below, I list the 15 industries (not including financial services, where cash has a different meaning and a reason for being) that had the highest cash balances as a percent of market capitalization.

In a few of these businesses, such as engineering and real estate development, the cash balances may reflect operating models, where the cash will be used to develop properties or on large projects and is thus transitional. There are other businesses, such as auto, shipbuilding and mining, where managers may be using cyclicality (economic or commodity) as a rationale for the cash accumulation. The ratio may also be skewed upwards in highly levered companies, since market capitalization is a smaller percent of overall value in these companies.

Regional Differences

If me-tooism is the driver of why companies in a sector often have similar dividend policies, can it also extend to regions? To examine that question, I started by looking at dividend statistics, by region:

Companies in Australia, Canada and the UK returned more cash collectively, in dividends, than they generated in net income, a reflection of both tax laws that favor dividends and a bad year for commodities (at least for the first two). Japanese companies are cash hoarders, paying the least in dividends and holding on to the most cash. Indian companies are cash poor on every dimension, paying little in dividends and having the least cash, as a percent of market capitalization, of any of the regional groupings. Finally, while much has been made about how much cash has been accumulated at US companies (about $2 trillion), the cash balance, as a percent of market capitalization, is among the lowest in the world. Absolute values are deceptive, since they will skew you towards the largest markets.

I also computed dividend statistics (dividend yield, cash dividend payout, cash return payout and cash as a percent of market capitalization) by country and plotted them on a heat map:

via chartsbin.com

Note that in some of these countries, the sample sizes are small and the statistics have to be taken with a lot of salt.

The Bottom Line

For both managers and investors, dividends are more than just a return of cash for which companies have no use. Dividends become a divining rod for the company's health, a number that companies stick with through good times and bad and one that has its roots in imitation more than fundamentals. Consequently, companies often get trapped in dividend policies that don't suit them, either paying too much and covering up the deficit with debt and investment cut backs or paying too little and accumulating mountains of cash.

Datasets

- Dividends, Buybacks and Cash Balances - By industry in January 2016

- Dividends, Buybacks and Cash Balances - By industry in January 2016

Data Update Posts

- January 2016 Data Update 1: The US Equity Market

- January 2016 Data Update 2: Interest Rates and Exchange Rates - Currencies

- January 2016 Data Update 3: Country Risk and Pricing

- January 2016 Data Update 4: Costs of Equity and Capital

- January 2016 Data Update 5: Investment Returns and Profitability

- January 2016 Data Update 6: Capital Structure

- January 2016 Data Update 7: Dividend Policy

- January 2016 Data Update 8: Pricing, with an end of month update