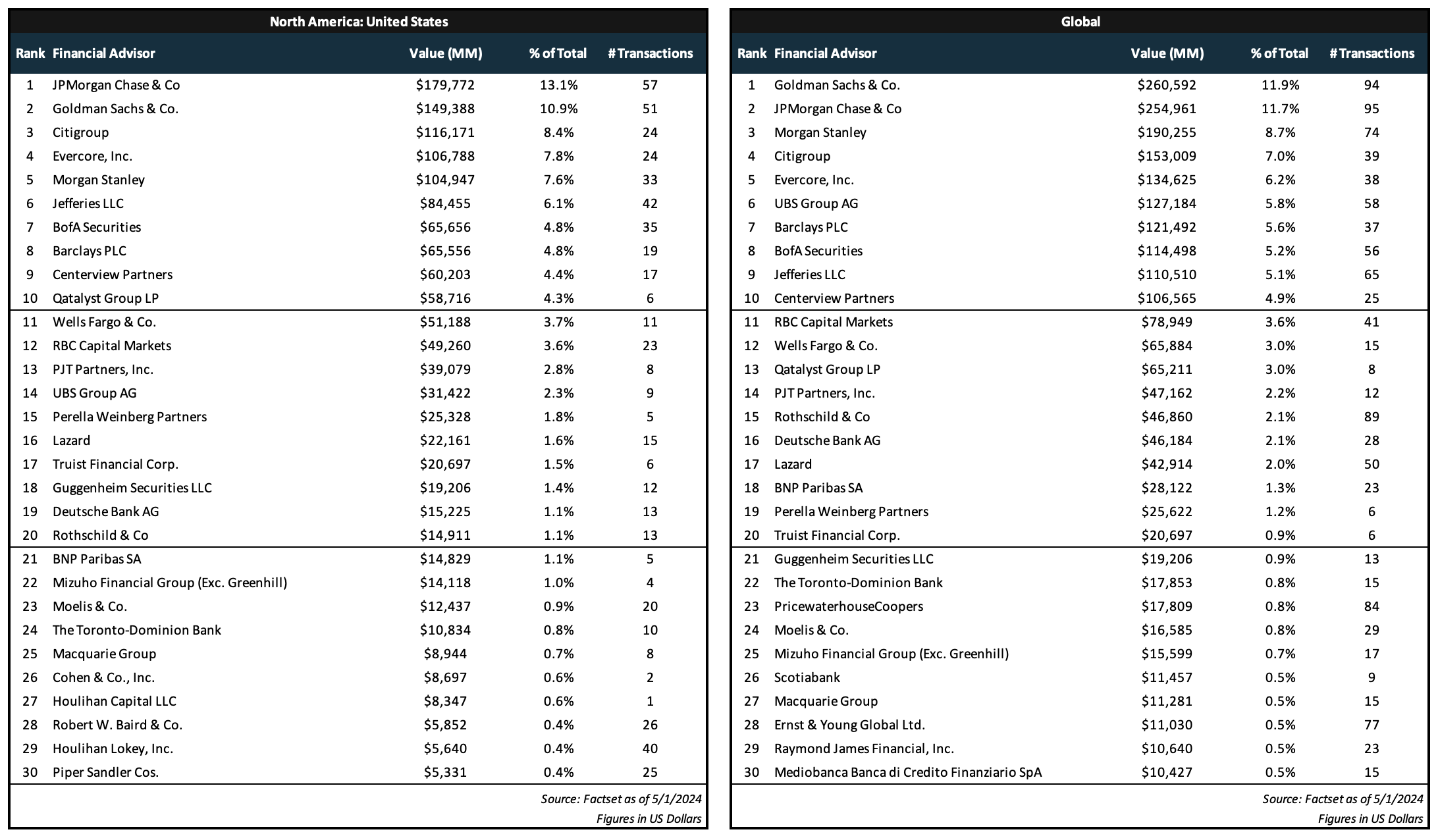

Investment Banking US League Table YTD 2024 (FactSet)

Thoughts anyone? Some interesting spots in 2024 for sure: Lazard, Qatalyst, Rothschild, Moelis, Jefferies, etc.

Edit: As of May, 2024

Thoughts anyone? Some interesting spots in 2024 for sure: Lazard, Qatalyst, Rothschild, Moelis, Jefferies, etc.

Edit: As of May, 2024

| +261 | Looking to raise a Billion Dollar Fund - College Junior | 38 | 51m | |

| +203 | It doesn’t need to be this way | 29 | 23h | |

| +124 | Biggest gripe in IB: people with no balls | 35 | 1h | |

| +123 | Career Bankers, Was It Worth It? | 39 | 2h | |

| +112 | What to expect during your IB summer internship and how to secure the full-time offer | 6 | 27m | |

| +83 | RBC M&A vs PJT RSSG | 14 | 1d | |

| +75 | I FINALLY DID IT, I GOT A FT OFFER! | 14 | 1s | |

| +65 | Vanderbilt ($$$) / Northwestern ($$$) vs UF ($) | 34 | 16h | |

| +63 | Did I mess up by correcting my VP Publicly? | 20 | 1d | |

| +51 | Feeling really lost in IB | 15 | 17h |

Career Resources

Get instant access to lessons taught by experienced private equity pros and bulge bracket investment bankers including financial statement modeling, DCF, M&A, LBO, Comps and Excel Modeling.

Qatalyst with $59 billion volume on 6 deals total.. holy fuck

With only 60 bankers total too gahdam

Gugg back to cranking MM deals

lol same with moelis. But still 8 months left of the year

.

Every time league tables get posted someone comments this, forgetting the fact that Moelis does a ton of sponsor sell-sides that don’t have reportable values. It goes to show how much of this forum is a bunch of college sophomores.

UBS #14. Exactly the same place we were before the CS acq lol

Shoutout Jefferies, they really came up

Looks like all the MD hiring spree from last year is starting to pay off.

Houlihan is a MM goat doing 40 deals for $5Bn

Keep in mind it’s $5bn of disclosed value. Actual deal value is substantially higher due to the fact that many deal values are not disclosed

Edit: The fact that this got MS just shows how many college kids are on this forum who have no idea what they’re talking about.

How would you say Houlihan relates to Gugg, Roths, or Greenhill?

Seems RBC and Jefferies are BB's now

Congrats on RBC!

A BB that ranks outside of top 10?

Surprised to see JPM so high with ~as many deals as GS (and for GS to have as many deals as they have - MS has 3/5ths the deals with 2/3rds the total transaction value.

Is GS deviating from its whale hunting model?

GS CMG team out in force this year 😤

on a per deal basis, what values are considered mm? i always figured anything below 1bn was mm region and above was large cap.

Actual definition is subjective and not relevant at the end of the day but “mm” can be anything from $50m - $2,000+ depending on industry and a million other factors

these numbers are just not correct. cvp lists all their deals online. you can do some quick math and see that they're north of $60.2bn

Straight from FactSet so guessing some deals are not on there, but gives a good general direction

I mean they were the exclusive advisor on two deals that on their own had a total transaction value of $60bn. and then they've done another ~15 pretty large deals

Congrats on Centerview

is greenhill sunpposed to be mizuho?

They still have their own ranking job the tables.

no, it's a seprate operation/entity

so greenhill is not even on these league tables? if so, rough for ghl

Just curious why Citi gets so much hate on this site despite being on the upper end of league tables? Not antagonistic, genuinely curious.

Jane Fraser + people like to shit on things on the lower end of a bracket (Cornell in Ivy, Citi in BB, Kellogg/MIT in M7)

The logic is actually people fight not to be the lower end of a bucket. I bet that its people from Brown/Dartmouth to shit on Cornell, DB and UBS and BoFA people shit on Citi, Tuck/Stern people shit on Kellogg/MIT.

I feel like Jefferies gets a lot of hate too

A lot of spurned analysts who resent the culture. Can’t deny its success but was (and still is) at the expense of an entire generation of juniors.

Welcome to banking though, I guess.

CITI BOYS UP

Why were barclays bonuses so low when they seem to be on the high end of the leader boards? Shocked to see them so high up yet paid such low bonuses

Because alot of the BBs get "deal credit" for deals they provided financing for. In the most extreme example (I personally know Barclays and Citi have done this) but these banks ask for deal credit when they didn't contribute to the process at all in exchange for hosting a banquet/dinner celebration, and the sponsor/GE firms don't pay a single dime on advisory fees to them.

I'm kind of new, so this has always confused me.

Why do league tables rank on deal volume then? Shouldn't it be based on fees?

Does anyone know what the heck Jefferies is? It’s not a BB, and not an EB, but is absolutely killing it in US and globally, plus it seems like the only bank that’s actually trying to grow

According to my calculations Jefferies is going to be top 3 in the next five years

Would y'all say that Gugg, Rothschild, Moelis, maybe even PWP offer a pretty similar analyst experience in the top groups?

Probably true

No, better experience within Moelis and PWP top groups. Way better transaction experience

Wow, Lazard is continuing to go down... No wonder they had shit bonuses

Feels like Greenhill 2.0 - Riding mainly on their legacy, although buyside exits are still very good

Weird, don't see Natixis on here. Are you sure the data is up to date?

Was not in the top 30 unfortunately

PJT above lazard in the US and globally but their M&A practice is "mid" according to WSO

Modern lazard isn't exactly the hardest thing to beat

Also for global pjt is 14 and rothschild is 15. In emea rothschild is consistently top 10, and in North America, pjt is consistently top 15. Considering that being top 10 in emea is approximately equivalent to being top 15 in North America (emea deal flow discount), its safe to say that they rothschild and pjt would be good comparisons to make for their m&a practice. In their respective regions, their m&a practices are equivalently strong, but outside of them, they are pretty weak. This is the exact reason why people on this forum would call Roths m&a mid (I would say above average instead though) so the same logic can be applied too pjt m&a to call it globally mid (again, I would say above average instead). The only eb which have a globally incredible m&a franchise would be cvp and evercore (cvp great in Paris and evercore good in London).

Not the same at all. For similar global deal value, PJT has 12 deals whilst Rothschild has 89. As a roths analyst you're far more likely to be working on only MM deals whilst at PJT it's mostly large cap.

What is BNP even winning?

Glad to see the top BBs (think JPM/GS/C) represented

Congrats on Citi!

I think this is helpful for determining the rough tier lists of firms, but I wouldn't look so much at the exact ranking. Ultimately, the experience of having 5.8% vs 5.6%(UBS at 6 vs Barclays at 7 for example) of the total deal flow isn't a significant difference, but the difference between 8.7% vs 5.8% is significant(UBS at 6 again vs MS at 3rd). The distinction between the top-tier BBs, mid-tier BBs, and low-tier BBs as well as the distinction between the top boutiques, the mid-tier ones, and low-tier boutiques is clear.

Is it just me or are a lot of these numbers pretty off? If you do some napkin math CVP, PWP, etc should be higher right? Only mentioning these two cause they easily show their transactions on their website.

CVP should be way higher with just Capital One, Endeavor & Champion and PWP just off 2 deals is higher (Blackrock & Shockwave) than the number listed as well. Is there something I’m doing wrong when I’m calculating these out manually?

Agree that seems off, but it's what FactSet's reporting. Gives good general direction

Plus look at the unannounced but rumored stuff they've got going - this is why league tables don't matter and aren't always indicative of franchise strength. Just in newsletters from the past two weeks they've got Nordstrom, Citgo, Angle American, Paramount etc. and just announced a big merger this morning. I've learned to not even glance at league tables until you're at least 6-9 months through the year because they frequently paint the wrong picture

There are so many banks now, I remember when it used to be just 5 banks

Molestiae laudantium repellat qui eum voluptatem. Nostrum corporis nihil aspernatur debitis nobis a. Voluptas provident nesciunt nostrum iusto quasi est. Consequatur quasi doloribus error id et cum. Nam quo omnis sed iusto.

Non aut provident qui molestias accusantium recusandae corrupti error. Eaque ut dignissimos porro qui iste.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...

Nostrum vel alias voluptas quae. Error expedita corporis enim vel sint.

Consequatur eum quia qui rerum aut. Non eos architecto accusantium culpa fuga debitis. Inventore illum aut doloribus quaerat rerum. Distinctio porro sequi neque sint autem quidem perspiciatis. Et beatae rerum reiciendis numquam.

Similique illo voluptatem cumque natus et qui. Ratione optio voluptates nihil ratione et dolore. Quasi libero voluptas qui enim ipsa natus.

Assumenda veritatis velit voluptatem voluptate. Quo magni et soluta soluta in aut sequi. Officia earum vel quisquam esse dolorem qui. Dolorem ipsa omnis ea ut eaque non et cum. Consectetur cupiditate est et error molestiae est aut.

Fugit cum aut omnis numquam. Totam ipsa voluptas molestiae odio eos omnis. A voluptatem qui doloribus eveniet rerum quo.

Et labore sunt et nihil expedita autem. Dolor sint eligendi et in sapiente consequatur. Aut rerum similique eaque voluptates. Accusamus consequuntur tempore dolor quod fugiat et facilis tenetur. Non nesciunt quae excepturi fugit.

Quaerat aliquam explicabo quis doloribus. Non qui delectus reiciendis enim praesentium aut nihil. Id est consequatur beatae pariatur nostrum saepe enim. Id asperiores quae sequi laboriosam. Autem cupiditate eius consectetur aut voluptatem. Ut et modi reprehenderit distinctio ducimus dolor recusandae libero.

Libero recusandae alias magni. Sint hic saepe nemo. Ab sed id repellat placeat nobis.

Et expedita alias sit tempore doloremque porro nemo corporis. Non eligendi et odio. Omnis libero aliquid consectetur provident laudantium. Qui aliquam ducimus sunt. Id error mollitia beatae impedit.

Maxime iste optio incidunt odio sint in. Aliquid provident et doloremque enim repellat.