A question was posed to me by our chief operating orangutan, Andy Louis, about Argentina's black market currency exchange, commonly called the blue market. Being a foolish person in general, I obliged to write about the potential causes and investment implications that the myriad currency controls and economic interventions undertaken by the Argentine government have promulgated.

This is absolutely a challenging question, and I assure you, my answer will be absolutely wanting. Someone much smarter than me would require another 50,000 words to be anywhere near convincing, but my hope is that this will at least fuel discussion.

A good place to begin is Argentina's blue market exchange rate. Luckily, in the information age, even black markets have tickers...

The key point you'll notice, the first is the point referred to in the graph as "Comienzo del Cepo Cambiario" in November of 2011. That the rate volatility began to fluctuate so wildly after November 2011 is no coincidence. It was then that the Argentine government began to institute capital controls, aimed at restricting the flow of US dollars. The resulting increase in the price of blue market dollars should not come as a surprise. With the supply of dollars severely restricted and demand left unchanged, a price increase is ensured. Keep in mind, Argentina is no backwater banana republic. It's a modern economy, making this situation all the more peculiar. In particular, one aspect that is shared by modern economies is that the populace will require a system by which they can profitably invest. But, with strong capital controls in place, the question becomes difficult. Thankfully, Andy has provided me with some invaluable sources, and their responses are interesting to say the least.

There's no 401Ks and CDs that the average Argentine can invest in, or that they would trust (i.e. AFJP mess), so all of their "savings" is either on the street (car) or in bricks (real estate). Real estate is still valued in dollars, so basically, Argentines save in dollars, and have restricted access to them. No one in their right mind would sell a property for say 100,000 USD and get stuck holding a handful of peso equivalent (at blue or otherwise) with 25%+ inflation. This is what basically froze the real estate market here, and the government is smoking some funny stuff it they think these new vouchers are going to get things moving in a significant way. Anyone wanting to build wealth, in their mind, needs dollars

This is reflected in the reporting of other outlets, namely Bloomberg, who also notes that expensive BMWs are used as a currency hedge. This, of course, is only the tip of the iceberg when it comes to appropriately hedging your exposure to the peso for the ordinary Argentine citizen.

As a former financial planner, I checked things out over 5 years ago of what it would be like to help people to invest here. It turns out that any big money means you help them (illegally) invest outside the country. If you were to invest in a portfolio domestically, there is a requirement that HALF of your portfolio must be invested in the MERVAL, which, obviously, would put your portfolio risk not suitable for long term investing, and certainly not suitable for your whole nest egg. The only (somewhat sane) way I found to invest small amounts of money each month (like 100 USD) is through a similar structure of what would be called in the states "Variable Universal Life Insurance" through companies like Zurich or Prudential in which you can invest in "mutual fund subaccounts" inside a permanent life insurance product. The subaccounts mimic real mutual funds and you are free to choose the asset allocation. You also get life insurance (not very common here) starting at 250,000 USD equivalent. Zurich's products seemed pretty solid here and they are (supposedly) the only company in Argentina that did not devalue the cash value of policies in 2001-2002. Bottom line for feasibility of becoming a financial planner here: if you want to do things legally, it would be a lot of running around and a lot of work for very little return. I decided it wasn't worth doing.

The basic theme I'm getting is that Argentines save in dollars, and exchange those dollars for pesos when the need arises. A currency trader and Argentine native suggests that this has been the case for many years.

I emigrated from Argentina to the USA in 1961. I have since come back every year. I have a large circle of local friends and family. During all these years, those who "saved" dollars have done best in the long run. As a matter of fact, I have never met anyone who saved pesos.

The conclusions that I'm forced to draw here is that investment in Argentina must be dollar based, and that if you can accomplish this, many Argentine citizens can probably provide you with some good business. From where I'm sitting, this is a pretty interesting investing dynamic, but the questions of "how" this is occurring, and "why" are worth exploring.

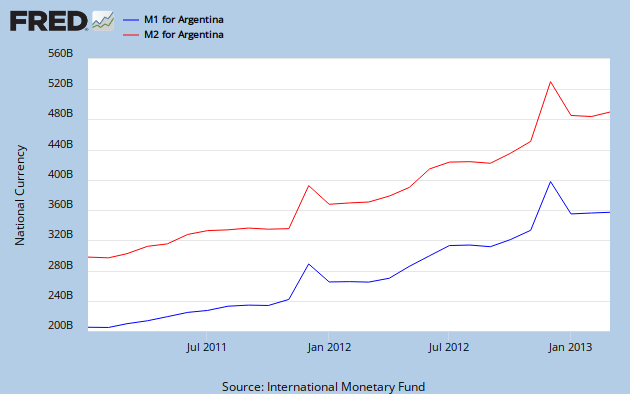

As a good American who's all too familiar with QE, the question of "how" such aggressive inflation could be occuring leads initially to the expansion of the currency supply. So, lets take a peek at their M1 and M2 levels.

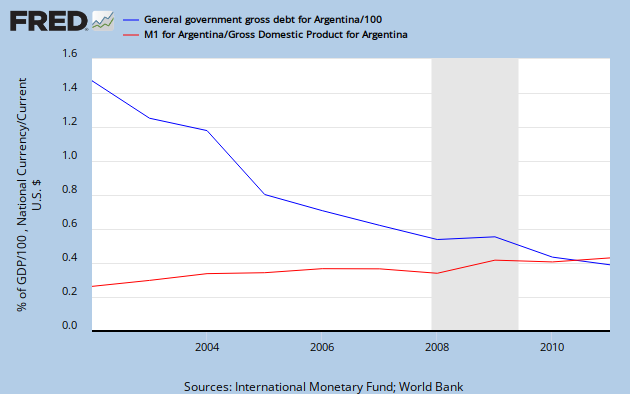

Now, what is a central bank to do with all their fresh new money? Well, traditionally, you use it to buy government bonds to increase government spending. Funny thing though, over the past decade or so, government debt has been decreasing fairly quickly as M1's share of GDP has been increasing.

Interestingly, as M1's percentage of GDP has gone up, their currency has depreciated by almost the exact same amount, at 103.25% and 105.54% respectively from 2002 to 2011. Additionally, Argentina's government debt as a share of GDP as dropped by 72.76% over the same period. To me, this does not appear to be the QE seen here in the US, instead, it appears that the government is literally inflating away their debt via an expansion of the money supply. Although, an interesting point was raised about this particular strategy and a potential pitfall:

..it only works if you are inflating away debt that is denominated in your own currency (like the US does, albeit at a less noticeable pace).

The data is from the IMF and while it does appear to be measured in dollars, it's unclear if it's denominated in dollars. Nevertheless, the point is very true, you can't inflate away another currency, only your own. So, what does this mean for the future of Argentina's exchange rate? Well, here is their projection of government debt all the way to 2017.

From what I can tell, given their propensity to print to pay down debt, the money supply and the resulting inflation doesn't seem likely to improve. A conclusion that probably won't shock many of you. However, the "how" was never the peculiar question, it's always been about "why" these actions are being pursued that's been of interest. Argentina is rich with natural resources, and you would think that they would be able to profit from their availability. It's not like it'd be the first time, Argentina was very powerful economically in the early 20th century. What changed?

I have an idea, I'm not sure how correct it is, but I do think it makes sense and fits well with the actions of their government. But, we'll have to go back to before 2001, when Elliott Management's subsidiary NML Capital started buying up Argentina's debt as fast as it could. You're all familiar with the basic strategy here, buy up distressed debt, then hold out, which is precisely what was done with great success. Here's an interesting twist, after the judgment from the 2nd circuit came down, the risk of technical default from other bonds became more clear, as reported by Reuters,

If Griesa's ruling is upheld by an appeals court and Argentina still refuses to pay, U.S. courts could eventually block debt payments to creditors who took part in the debt restructurings out of consideration for investors who rejected Argentina's terms at the time.That would trigger a technical default on approximately $24 billion worth of debt issued in the 2005 and 2010 exchanges

If Argentina was less than keen to pay the holdouts the original $1.33 billion NML Capital was looking for, $24 billion would likely appear to be a material risk to Argentina's government. Their bond prices, as observed by J.P Morgan support this approach, as do observations of the Argentine CDS rate.

Currently, the case is awaiting a response from the US Solicitor General, as requested by the Supreme Court of the United States, giving Argentina a reprieve until the next session. It is this decades old debt case that appears to be the motivation behind Argentina's currency controls and inflation. It appears that the Argentine government is motivated to get their debt to as small a level as possible, and by any means necessary (especially considering one particular voting member of the ISDA's credit derivatives determinations committee), to avoid the worst possible of outcomes that this ongoing battle could cause.

Rerum est eligendi incidunt est ullam recusandae qui. Blanditiis nesciunt beatae quas reprehenderit occaecati et temporibus.

Minus debitis a aut soluta aut. Ex magni minus deleniti rerum voluptatum nobis sit. Voluptas enim consequuntur ut repudiandae nemo excepturi. Qui ratione eligendi saepe et quibusdam et aut. Quaerat dolor dolores reiciendis ipsum in voluptas et. Quas voluptatem maxime delectus sed voluptatibus.

Quasi dolorem iste doloremque aut aut eos. Blanditiis esse officiis cupiditate et. Sunt molestiae modi quia incidunt officia debitis ullam. Aspernatur a doloribus maiores.

Aliquid nihil optio dolorem quidem sit totam. Consectetur laborum nulla quis blanditiis. Hic est animi nulla maxime assumenda eos totam perferendis. Sunt quidem vel eos qui ab blanditiis. Aliquam hic ex eveniet modi quo veniam molestiae.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...

Eum voluptatem sapiente aut id explicabo tempore quis. Molestias modi commodi enim ut ea et. Veritatis debitis occaecati molestias fugit. Laudantium iure et dolor porro quasi qui.

Odit unde nemo voluptas sed. Delectus facere voluptas aliquid exercitationem autem. Est voluptatem natus harum. Neque et repudiandae sed eos autem expedita id.

Non laborum voluptatem repudiandae nisi. Ex quis quia vero eveniet aut. Omnis molestias aliquam qui. Sequi quidem saepe ratione maiores distinctio. Eaque quia beatae eos nam.

Qui et facere totam recusandae. Dolorem natus sit enim officiis animi et quo sed. Corrupti dicta nesciunt maxime debitis consectetur assumenda. Consequatur suscipit et inventore ut aut. Sequi fugiat distinctio ut qui eos fuga.

Iure odit voluptatem sed cumque qui. Praesentium eaque ipsa omnis sit. Velit aut veniam facilis id omnis. Quam qui et optio consectetur illo dolorum atque.

Harum suscipit dolore amet qui ut ipsam. Eum provident cupiditate eum reiciendis quae. Omnis voluptatum ut voluptatem libero consequatur. Sit eum rerum magnam.

Quo perspiciatis ipsa illo hic. Labore sint repellendus animi sunt similique quaerat. Rerum sed sint et id quas minima expedita.

In odit qui sint ut dolor laborum. Nisi consequuntur cum sit qui tempora. Fuga ab odio sit omnis ipsam saepe animi. Autem inventore perferendis fugit saepe corporis. Deserunt modi rerum numquam unde incidunt.

Veritatis facilis cum et sed. Ab blanditiis ut aut debitis quaerat. Ut sed odit ea odio facere.

Laboriosam doloribus incidunt aut enim voluptatem. Aliquam facilis nisi ratione. Illo quia qui est nulla.

Adipisci officia sunt aperiam itaque eaque aut. Distinctio eos eos et ea earum laborum quaerat. Sint voluptas architecto ut quo. Ut fugit sit voluptatem voluptas est.

Itaque dicta recusandae qui aut et rerum aut. Iure qui aut odit illo maxime. Cumque nisi voluptatem ullam vel sit molestiae animi.

Dolor repellat veniam quia blanditiis numquam velit. Reiciendis vel dolores beatae. Non et ad voluptas veritatis. Perspiciatis nam tempora voluptatibus maiores. Fugiat libero qui iste ratione sequi. Sed laudantium et esse libero aperiam ab. A quia temporibus voluptates nulla provident ratione voluptate.

Laborum suscipit provident ut. Harum rerum a eos necessitatibus sunt quis rerum. Et sunt vel consequatur quo debitis. Aut a voluptates unde praesentium. Tenetur aut debitis sit et fugit.

Corporis est vel harum commodi incidunt. Qui necessitatibus aperiam recusandae exercitationem. Quam cumque consequatur tempore minima. Illum adipisci odit fugiat.

Atque eius ut rerum at. Aut accusamus quia labore expedita qui. Possimus et deleniti nesciunt unde similique tenetur. Qui iste et repellat iste. Natus et ullam fugit qui ducimus. Fugiat unde velit similique tempore et sint pariatur quae.

Itaque repellat facilis ut quos assumenda quae quas. Repellat eaque facere vel quisquam. Suscipit et vero aut veritatis quia aut quia. Molestias sed natus vel recusandae dolorem et ut.

Est consequatur aut et et explicabo. Ipsum distinctio exercitationem quia et accusamus laborum repudiandae aspernatur. Aliquid nihil ratione sunt. Quis eligendi laudantium ab et et aperiam. Cupiditate eos quia culpa laborum.

At nihil atque quibusdam id rem. Numquam in fugit omnis reiciendis in qui. Commodi iusto natus ex quia ut deleniti voluptate. Qui eum deserunt optio quae qui rem neque. Sunt quia voluptatem odit quaerat.

Numquam qui laboriosam incidunt et illo facilis. Explicabo sed recusandae non porro velit ea quae. Sit aliquam deserunt aut rerum sed. Voluptatibus ducimus ad dolorum dolores. Autem voluptates mollitia expedita natus neque omnis. Fugit alias voluptas rerum ipsum.

A est odit minus debitis. Totam expedita et accusantium ducimus accusantium ut debitis in. Vel iure nihil quasi eius ipsum sunt. Quos ut magni pariatur quia laborum. Esse ea neque non itaque tenetur id est.

Sequi accusantium tempore pariatur qui saepe dolorem minus. Ut quo expedita reprehenderit optio. Sit qui sed dolorum laudantium qui nisi. Dolorem ut molestias expedita expedita. Exercitationem ad optio ut laudantium. Eaque voluptatem explicabo distinctio nostrum est.