Interest-Only Mortgage = Lower IRR?

Hi All,

Just wondering if you happen to have come across a property investment using interest-only mortgage, i.e. mortgage where you will pay only interest on a monthly basis, and lump sum of principal at the end of mortgage period.

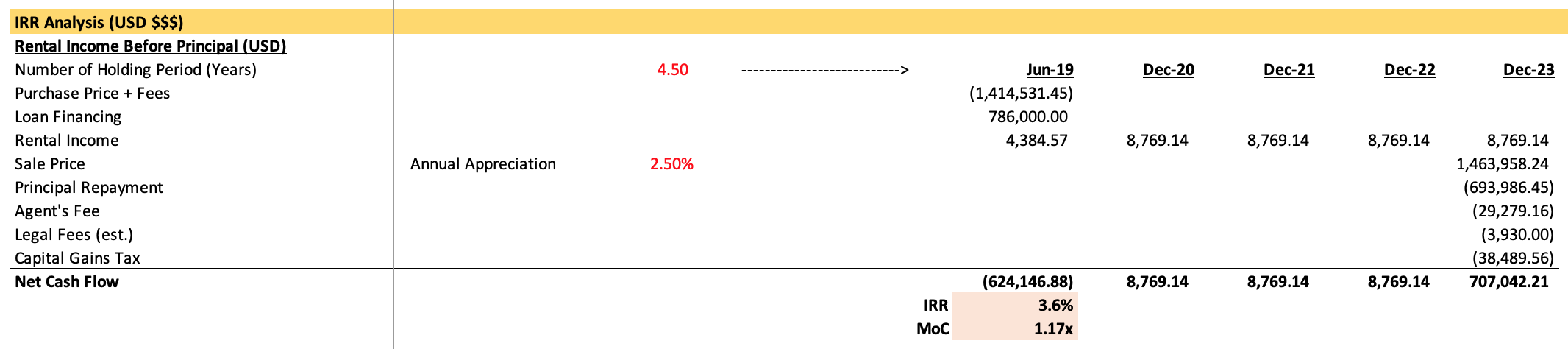

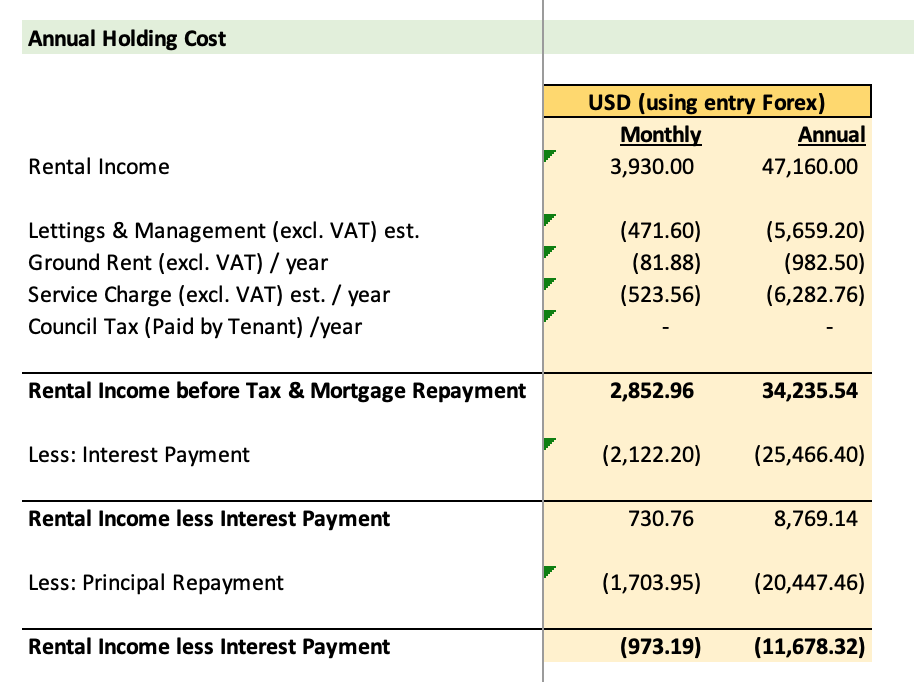

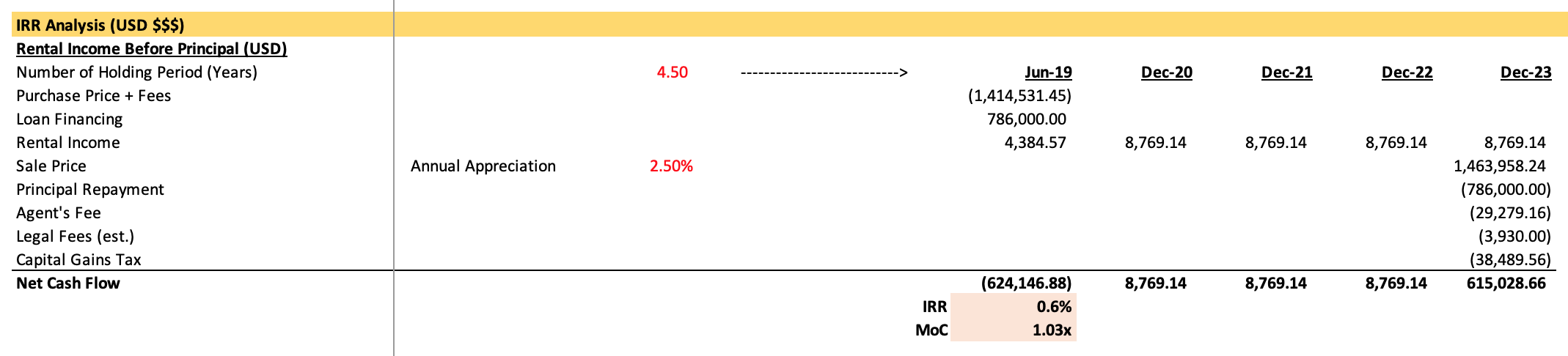

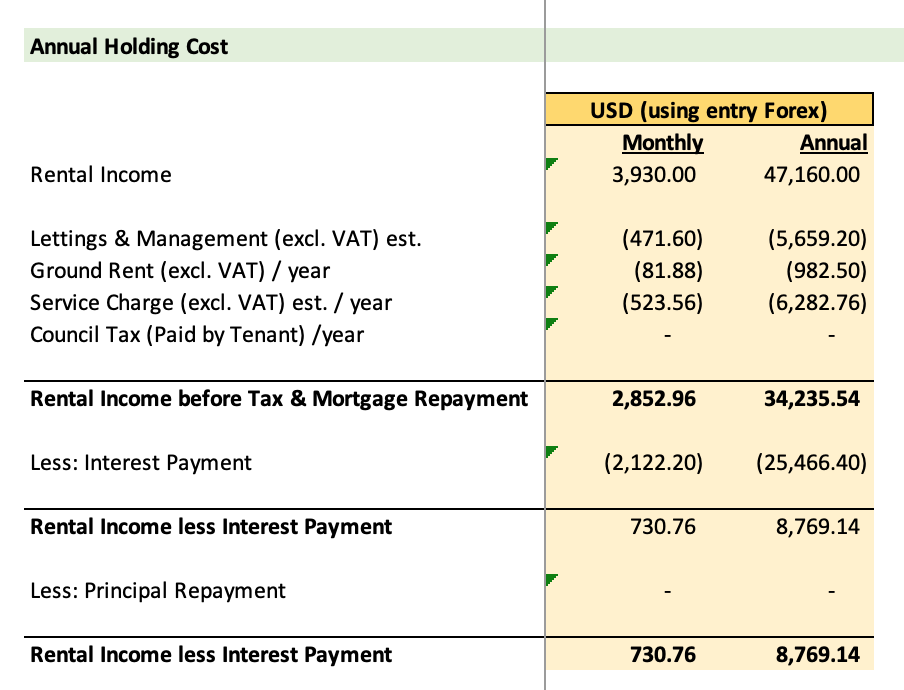

When comparing the investment using regular mortgage where you pay principal on a monthly basis (see attached) vs. investment using interest-only mortgage (also attached), I found that the interest-only option yields lower IRR.

Does this actually make sense or am I calculating this wrong? Does this mean a regular mortgage is always a better option than interest-only mortgage?

Also, as a noob in real estate investments, how do people usually make their calculations for their investment decisions? Is it using IRR method as I have done or is it some other metrics?

Thanks!

| Attachment | Size |

|---|---|

| IRR Regular Mortgage 103.39 KB | 103.39 KB |

| Holding Cost Regular Mortgage 110.22 KB | 110.22 KB |

| IRR Interest Only 104.39 KB | 104.39 KB |

| Holding Cost Interest Only 105.3 KB | 105.3 KB |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Your yearly cash flows do not appear to take into account principal payments.

Don't have the time to sort through your model right now, but something to remember is that interest only debt often, if not almost always, gets refinanced before the I/O period ends. You either refinance to cheaper permanent debt or sell the building and the buyer puts their own debt on it.

You need to take a step back and think about the bigger picture. If rate is the same except one amortizes and one doesn't you would have a similar IRR but your cashflows would be different due to the amortization payment or lack thereof.

The amortization would be reducing your total debt and increasing proceeds at sale due to less total debt to be paid, and in theory this would catch you back up from the standpoint of IRR to the I/O choice.

P.S. I have no idea what your model is showing. Not sure if its errors or what, but you should take a look at that and make sure it is working correctly.

This doesn't make much sense. The sooner you get your cash flow, the better. With amortization you lower your D/E-ratio gradually, which will hurt your levered IRR.

Levered IRR = Unlevered IRR + (Unlevered IRR - Interest) x D/E

So, unless there is significant difference in the interest in those two options (interest only or with amortization), the levered IRR will always be better without amortization.

well not true, but a good rule of thumb. What you can say is that after roughly a 10-year hold period, your loan balance has decreased by roughly 20%. So it will depend on your growth assumptions, your cap rate expansion, and a couple other more minor factors. IF you are in a market with high appreciation then what OP said could make sense. Your FCF upon reversion including amortized debt repayment could mean a higher IRR than your "coupon clipping" at a more yield focused investment.

Honestly, a lot of ways you can look at this, but my 2 cents based on my experience and analysis

Intuitively this makes no sense if you are discounting your cashflows. I.O lets you stay more leveraged and get cash flow much quicker

an interest only loan is more expensive than a day1 amortizing loan...basically because you are paying interest on 100% of the principal balance, and still having the full balance repaid at the balloon date. Whereas with a day1 amortizing loan, the interest that is due is on a lower principal balance as the loan is continually paid down.

The IRR is time value, so there is that effect as well...and how large the proportional trade off is to your residual sale price. But the reason people chase interest only loans isnt because it's more profitable...in face it isn't. It's often because it's a SAFER strategy, meaning that if your property is delayed, slow to lease-up, or just generally below pro forma - you only have the interest payment to contend with, and don't have to deal with a larger P+I payment. Granted depending on how your covenants are structured (which often calculate the debt with some type of amortizing payment), you might still be in a violation or default scenario...

okay, just take a step back for a moment. if you have a 1,00,000 loan at a 5.0% interest rate amortizing over a 30 year schedule, that would equate to a fully amortizing payment (both principal and interest ) of ~$64k per year. in an interest only loan, your yearly payment would only be $ 50k. if you have 100,000 in cash flow before debt service of 100,000, clearly your cash on cash would be higher only paying $50k in debt service, rather than the $64k per year. therefore, your IRR is going to be higher because you just have more cash in your pocket, which is why most people try to maximize the interest-only period

You really need to take a look at the numbers here to understand why OP is getting these results.

The reason you're getting a lower IRR is because you have an ERROR. The wrong cash flows are being used in your analysis. The amortizing loan scenario is using the I/O cashflows.

Based on your uploaded images, your amortizing cash flows should be NEGATIVE.

Fix it and you'll see the correct IRRs.

Minus enim laudantium ut possimus. Labore enim qui architecto consequatur. Molestiae dolorem provident veritatis excepturi id saepe architecto.

Accusantium rerum omnis reprehenderit aut a voluptatem. Tempore non neque labore voluptatem vel corporis. Et nulla voluptatibus facilis veniam.

Est ut dolor sunt eveniet aliquam voluptatem. Error saepe sequi voluptatum quo sapiente ipsum laborum. Velit nihil omnis omnis voluptatem reprehenderit saepe dolore. Dolor possimus ipsam ut vel.

Molestias et sit commodi aspernatur minus quos voluptates. Ut quasi et eum corrupti qui soluta delectus. Et dignissimos vel consectetur. Quia nemo corrupti optio aut quidem ut. Sit et dolorum quibusdam repellendus. Molestiae et suscipit temporibus voluptatum.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...