Was hoping that you fine gentlemen could potentially help me with some difficulties that I'm having with this valuation. I was tasked with valuing CBB as a stand alone entity.

The Details:

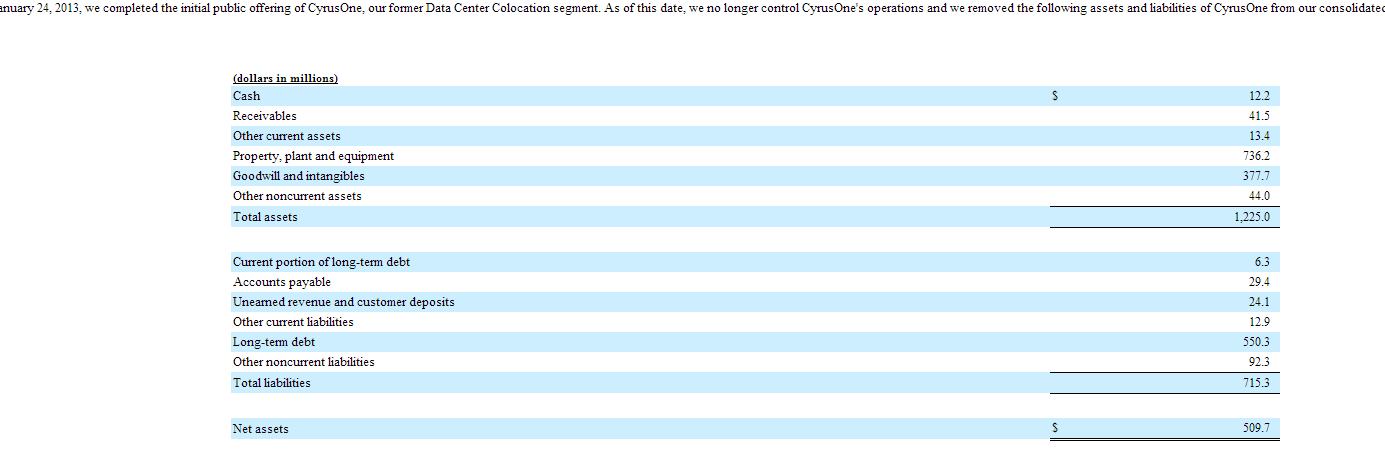

CBB spun off CyrusOne (CONE), which it acquired in 2010, in January 2013. Originally, CBB owned a 69% stake in CONE, but has since reduced it to 44%. Its 10k, for FY 2013, consolidates the operations of CONE for the first month and then uses the equity method for the remaining 11 months.

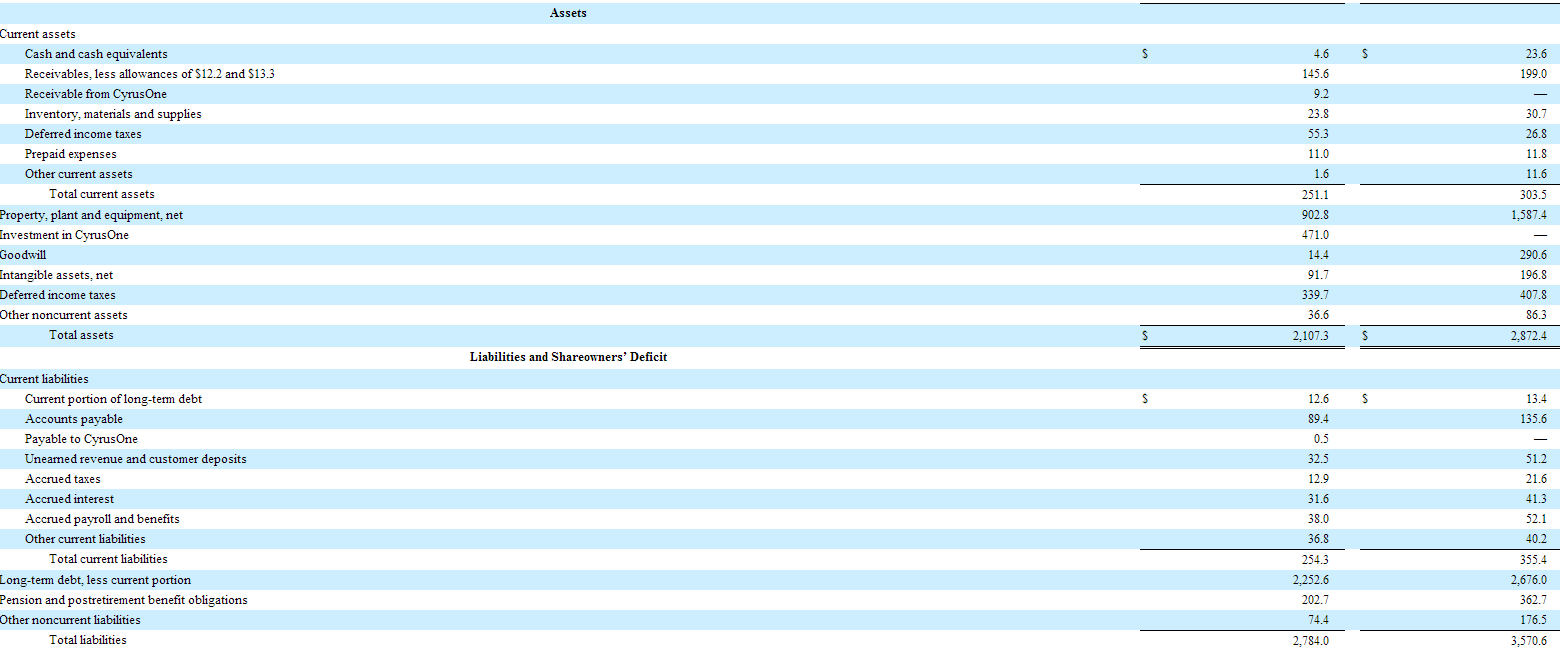

The equity method strips the assets and liabilities of the entity from the balance sheet and replaces them with single line items representing the equity investment (see attachments "CBB Balance Sheet Adjustments" and "CBB Balance Sheet"). The equity investment in CONE shows up on the asset side of the balance sheet as "investment in CyrusOne" for $471M, but I fail to see any explicit contra account.

Total assets, even when you include the "investment in CyrusOne," falls from $2872.4M in 2012 to $2107.3 in year end 2013. Additionally, the "equity method" moves all operating activities below EBIT on the income statement, but the adjustment remains above the line as "loss from CyrusOne equity method investment." The adjustment takes the % stake in CyrusOne and then multiplies it by its respective net income figure.

Clearly, there is incongruity in the financial statements, which I attempted to adjust for during the explicit forecast period. In other words, I attempted to remove the "investment in CyrusOne" line-item and add back (a) the original balance sheet values (see attachment "CBB Balance Sheet Adjustment") and (b), the revenue and EBIT figures of CONE to the consolidated revenue/ebit balances. I did this so that there's uniformity in the financial statements between FY 2010 and FY 2013. I then projected those values forward (using quarterly 2014 data from CBB and CONE's 10Qs).

My Original plan was to value CBB with CONE and then strip out 56% of CONE based on its current market cap (also plan on valuing CONE with both a multiples/comp analysis and with a DCF model in order to compare its intrinsic value with that of its current market cap).

My Problem:

Reconstructing the CBB's financials by adding back CONE, especially the balance sheet, led to a massive spike in most of the book values, leading to, what appears to be, an overvaluation - even when I subtract 56% of CONE's current market cap. Additionally, I don't know how other line items are affected; CBB has all sort of ambiguous liabilities/assets without footnotes (such as "other noncurrent assets" and "other noncurrent liabilities"). The overall accounting quality for this company is shit.

A fellow analyst told me that balance sheet adjustments aren't required when the equity method is employed - the only adjustments that need to be made are to revenue and EBIT figures. The single "investment in CyrusOne" line item will account for the CONE spin off. Unfortunately, this leads to a massive decline in asset and revenue growth which, in a valuation model, is projected forward.

So again, my problem is establishing congruency between the book values depicted in the financial statements for years 2010 - 2014. I can ignore balance sheet adjustments and just revise revenue and EBIT growth, but that doesn't seem correct without corresponding balance sheet adjustments. Any recommendations?

| Attachment | Size |

|---|---|

| CBB Balance Sheet Adjustments.PNG 12.94 KB | 12.94 KB |

| CBB Balance Sheet.PNG 22.63 KB | 22.63 KB |

{kind=link}

{kind=link}

{kind=link}

{kind=link}