Operating Income

It measures a firm's income before deducting taxes and interest payments

What is Operating Income?

Operating income, OI for short, is a business's income after subtracting the cost of goods sold (COGS), selling general and administrative expenses (SG&A), and depreciation and amortization (D&A) from revenue.

It is a measure that exclusively includes items related to the business's core operating activities, providing a clear picture of its financial health.

Core business operating activities include items necessary for the business to exist and perform its primary functions related to selling products and services. They include operating, marketing, production, and administrative tasks.

- Operating income provides a clear picture of a business's financial health by exclusively including costs related to its core operating activities.

- The two primary methods for calculating operating income are the top-down, bottom-up, and cost accounting approaches. Each method starts from different points on the income statement and follows distinct formulas.

- Operating income helps to increase the impact of the firm’s ability to reduce costs and improve efficiency.

- Analyzing operating income over different years allows investors to assess a company's performance and identify cost-reduction measures that increase profit efficiency.

- Operating income allows for comparing metrics across companies without including items related to the capital structure.

Understanding Operating Income

Operating income is a critical financial indicator derived from the business's core operating activities, which include costs such as COGS, SG&A, depreciation, and amortization.

One item is the cost of goods sold, which includes all direct expenses related to the production of goods or services sold, such as materials, labor, and manufacturing overhead.

The next set of items to get subtracted are the Selling, General, and Administrative expenses.

These expenses include salaries, rent, utilities, marketing, and office supplies. They are tied to the business's operations but not directly to selling the product.

The last components are depreciation and amortization, which represent the wear out of tangible and intangible assets.

Importance of Operating Income

Operating income is critically important for an organization to be calculated for the following reasons:

- Operating income reflects the critical costs of a business's operations, serving as a measure of operational efficiency and cost control.

- It is essential for investors as it helps evaluate a company's operational performance and efficiency over time, enabling comparisons across different periods.

- The item is also essential for investors because it doesn't include items related to the capital structure, which allows them to compare the metrics across companies.

Operating Income Formulas and Calculations

Generally, the three primary accepted methods for calculating operating income are:

Top-Down Approach

The top-down approach assumes that when calculating operating income, we start with the highest items on the income statement and work our way down.

The formula is below:

Operating income = Revenue - The Cost of Goods Sold - Selling, General and Administrative Expenses - Depreciation - Amortization

SG&A includes marketing, advertising, rent, utilities, accounting, and legal fees.

The formula started with revenue and subtracted the cost of goods sold and all of the SG&A items. Lastly, it subtracts depreciation and amortization.

Bottom-Up Approach

Another approach to calculating the operating income is the bottom-up approach, which assumes that we start with the net income and work our way up.

The formula is below:

Operating income = Net income + Tax Expense + Interest Expense

The formula starts with the last income statement item - net income. Then, we add back the taxes and the interest paid on debt.

Cost Accounting Approach

The cost accounting approach is not commonly used for external financial reporting but can be valuable for internal analysis.

Instead of grouping everything by function (like in the above examples, e.g., revenue, cost of goods sold, SG&A, etc.), the formula groups everything by nature.

Grouping implies taking the revenue and subtracting the direct and indirect costs.

Here is the formula:

Operating Income = Net Revenue - Direct Costs - Indirect Costs

Net revenue takes the revenue and subtracts all of the discounts and allowances.

At the same time, the direct and indirect costs are directly and indirectly tied to the business's core operations, respectively.

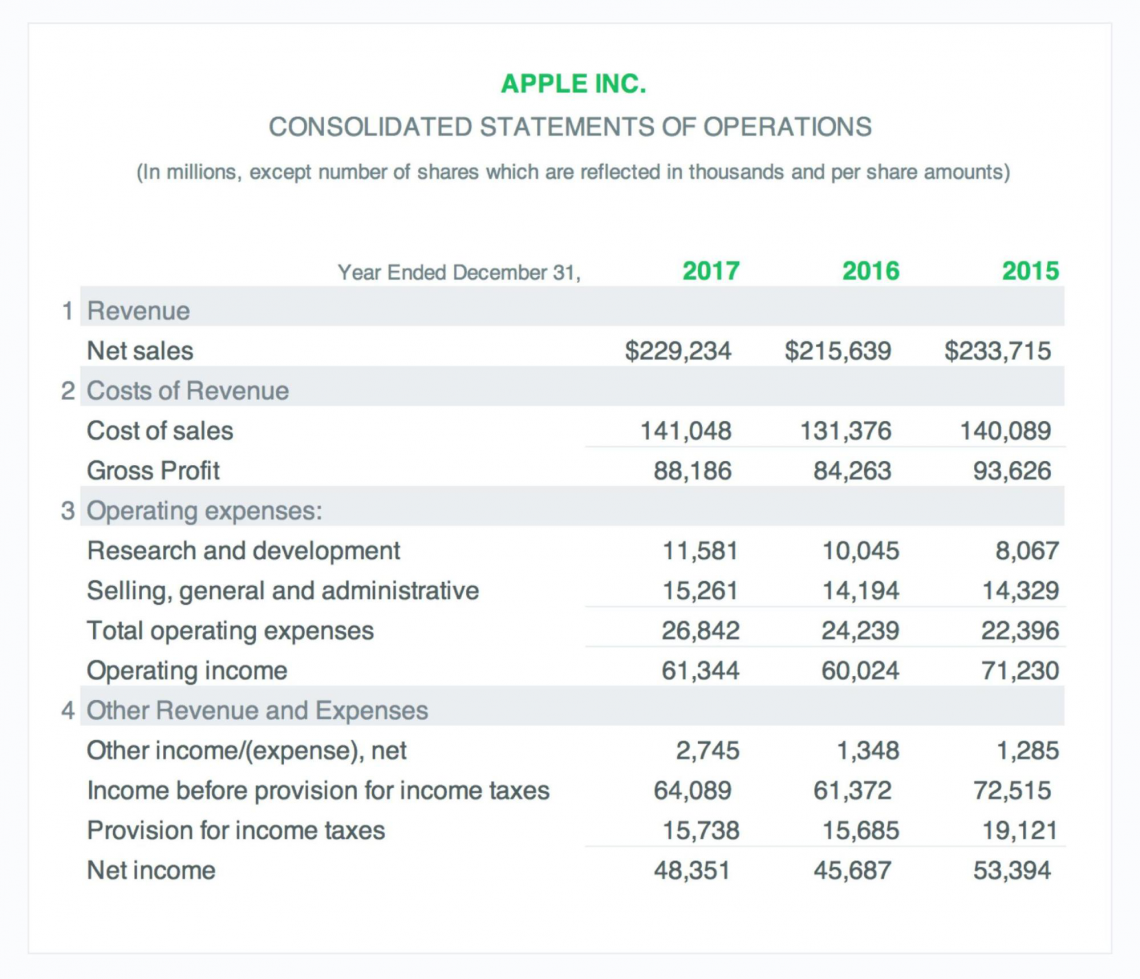

Operating income example

Let's examine a real-world example of operating income on an income statement for Apple in 2015, 2016, and 2017:

Looking at the income statement, one can observe many items and operating income somewhere in the middle. We can arrive at those items either using top-down or bottom-up approaches.

One can also observe that Apple’s financials have been presented for several years. An investor can compare the statements for different years to see how the company performs.

For example, in 2016, Apple's operating income was $60,024 million, but a year later, in 2017, it was $61,344 million. The cost of goods simultaneously has increased from $131,376 million to $141,048 million.

By running a simple calculation, operating income increased by 7.36%, meaning Target became more profitable from an operating standpoint.

Operating Income vs. Other Financial Calculations

Operating income is an excellent measure of a business's profitability after subtracting all costs related to its core operations. Still, other metrics also try to display a similar idea but differ.

Some comparisons are:

Operating Income vs. EBIT vs. EBITDA

EBIT and operating income can appear similar in company statements, but EBIT may include some non-operating income or expenses, unlike operating income.

Still, sometimes, both calculations do differ. The EBIT calculation excludes interest income but might include income from other non-operating sources.

EBITDA is very similar to EBIT. The only difference is that EBITDA adds back depreciation and amortization. However, unlike operating cash flow, EBITDA does not account for changes in working capital or capital expenditures.

Some analysts think EBITDA is a better operating metric since the depreciation and amortization are non-cash expenses and don't represent actual cash outflows.

Operating Income vs. Operating Cash Flow

While OI is an excellent measure of a company's core profitability, it is based on the accrual GAAP rules.

The rules require companies to record revenues and expenses when they are incurred rather than when the actual cash is received, which is a helpful metric.

Still, it is also helpful for investors to know how much cash the business generates from its core operations, and operating cash flow is crucial here.

Operating cash flow takes net income and adjusts for accruals by adding changes in net working capital, depreciation, amortization, and other non-cash expenses.

Operating Income vs. Free Cash Flow

While free cash flow also tries to show how much a business has generated from its operations, it is more related to the return the investors require.

After subtracting all the operating expenses, the metric tries to find out how much actual cash flow all the investors in the capital structure get.

The most common formula takes the EBIT, adds depreciation and amortization, and subtracts net working capital and CAPEX to determine what is left for the investors in real cash (adjusting for accruals).

Operating Income FAQs

One limitation of operating income is that it is based on accrual accounting, which may not accurately reflect the actual cash flow generated by the business.

Additionally, operating income excludes interest expenses, taxes, and non-operating income or expenses, which may affect the overall financial health of the company.

The company can improve its operating income through several methods.

One method is to reduce the cost of goods sold through various cost management initiatives, including negotiating lower prices with suppliers and improving operational efficiencies.

Another method can be improving inventory management by reducing the amount of inventory on hand and increasing turnover.

Lastly, management can enhance staff productivity through training and incentive programs while also focusing on strategies to increase the average order value.

Yes, operating income can be negative, which indicates that the business is not generating a profit from its core operations, regardless of interest and tax expenses. This is typically a concerning sign for the company's financial health.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?