My last two posts looked at two strains of value investing. In the first, passive screening, you look for mismatched companies that trade at low prices, while not being burdened with high risk, low growth or low quality growth. In the second, contrarian investing, you focus on companies whose stock prices have gone down the most, on the assumption that markets overreact to news and consequently have to adjust.

While both approaches are backed up by empirical evidence, you still face a problem as. Without a catalyst in the market, causing the stock price to move to what you think is a "fair value", you can be right in your assessment of value, and go bankrupt being right. In activist value investing, you remedy that problem by acting as the agent of change in the companies you target, and thus have a bigger say in your investing destiny.

Structuring the discussion

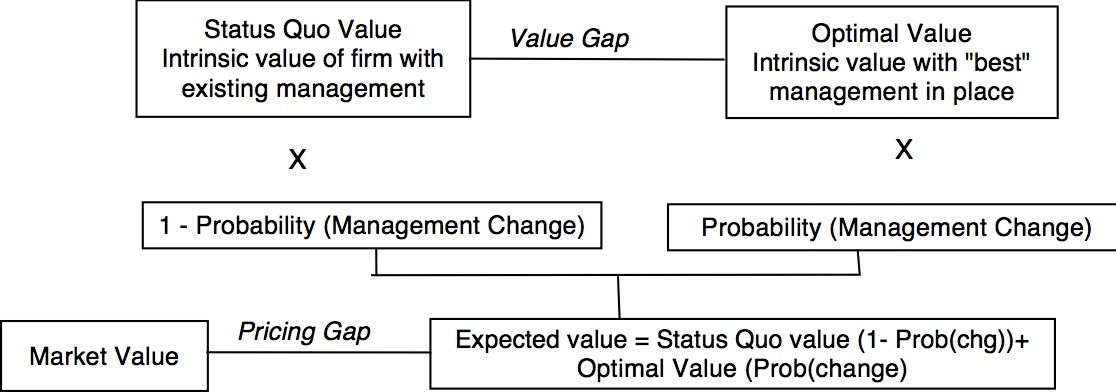

To structure the discussion of activist value investing, let me begin be offering three measures of value for a publicly traded company: The first and most observable measure is the market price of the stock and the resultant market value of the company, set by demand and supply, and driven by the moods, perceptions and expectations of investors. The second is what I will term "status quo value, reflecting the intrinsic value of the company, run by its existing management team, with all of its strengths and weaknesses. The third is the "optimal value", capturing the intrinsic value of the same company, run by the "best" possible management team. To the extent that a firm is not being optimally run (and what firm ever is?), the optimal value will be higher than the intrinsic value. Unlike the market value, both the status quo and optimal value will require you to make subjective judgments and estimates, with all of the noise that comes with that process.

There is one final factor to consider, and that is the likelihood that the existing management will change, either as a result of internal pressures (from stockholders and the board) or external ones (a hostile acquisition). The expected intrinsic value of this firm can then be written as: Expected Intrinsic Value = Optimal value (Probability of change in management) + Status Quo value (1 - Probability of change in management)

While there are multiple factors that go into determining this probability, including the composition of stockholders, insider holdings and the existence of multiple share classes (with different voting rights), it is a convenient shorthand for the quality of corporate governance of the firm; good corporate governance should translate, other things remaining equal, into a higher probability of management change.

Bringing it all together, here is the big picture of how the three measures play out in the real world:

Both passive and contrarian value investing are focused on finding stocks that have a pricing gap, i.e., trade at a market price less than the expected value, though some strands of contrarian investing incorporate expectations of control changing (and the resulting increase in value). In contrast, activist value investing attempts to provide catalysts to close both the pricing gap and the value gap, by changing the probability of management change at companies (and thus increasing the expected value of the company) and getting the market to recognize its mistakes in pricing the stock.

The expected value of control

If you buy into this framework, to assess the value of control in a firm, you have to value it not once but twice, and be able to trace out the effects of changing the way a company is run into the value. Since we know the determinants of value, that is a relatively simple task. In the figure below, I list out the four determinants of the value of operating assets of a firm and the questions that give rise to potential value creation:

In summary, there are three pathways to value creation.

-Generate more cash flows from existing assets:

You can manage your existing assets more efficiently and generate higher cash flows from those assets. To the extent that cost cutting and more efficient operations are not buzz words, this is the place where you will see the results.

-More valuable growth:

Since it is not growth, per se, that creates value, but growth with excess returns, a firm that is pursuing value destructive growth (by investing in assets that earn less than the cost of capital) can increase value by reinvesting less, whereas a firm that has lucrative investment opportunities (earn more than the cost of capital) can increase value by reinvesting more. The choices made on this dimension will affect dividend policy, since less (more) reinvestment will translate into more (less) cash available for return to stockholders.

- Cost of funding:

To the extent a firm can reduce its cost of capital by changing its financial mix (debt and equity), altering the debt it carries to better match its assets or reduces it operating risk can reduce cost of capital and increase value.

If you are interested, I have an extended discussion of the expected value of control in this paper. I also have a simple spreadsheet that you can use to assess the status quo and optimal values for a firm. I have entered the numbers for Kraft Foods in here, and based on my assessments, Kraft Foods has a status quo value of $59 billion and an optimal value of $ 65 billion, leading to a value of control of about $ 6 billion.

For an activist value investor to be a catalyst for value change, he or she has to first identify a firm that is poorly managed, relative to it's potential, and then has to follow up by figuring out what aspect of value creation offers the most promise in the identified firm. Cookbook restructuring, where the same remedy (borrow money, divest asset, pay dividends) is employed for every "troubled" firm, can easily destroy value at some firms. Finally, the investor has to try to alter the probability of management change. At the extreme, this can take the form of a "hostile acquisition", where the activist investor accumulates a majority stake in the company and puts in place a new management team. It can also take lesser forms, including proxy fights and forming coalitions with other investors to change the composition of the board of directors.

The pricing gap

Assume that you have what you feel is a reasonable assessment of the expected value of a firm, based upon your status quo and optimal values. Could the market price deviate from this value? Sure, and there are three possible reasons:

a. Wrong side of momentum:

As I have noted in earlier posts, market momentum can be a strong force, pushing prices away from fair value over extended periods. Thus, a stock that has fallen out of favor may see its stock price get pushed down well below its status quo value, as investors flee, and one that is in favor can see its stock price increase well above even its optimal value.

b. Market mistakes:

Even the firmest believer in efficient markets will concede that markets can make mistakes in assessing and incorporating information into prices. If that occurs, the price can deviate from value, in either direction.

c. Market misunderstanding:

Some companies are so complex in terms of organizational structure and business mix that even diligent investors may be unable to price them correctly. During periods of crisis, it is not uncommon for investors to reduce what they will pay for these assets, i.e., attach a complexity discount on value.

As an individual investor, you or I have little chance of stopping momentum, getting the market to correct its mistakes or clearing up misunderstandings, but activist investors may be able to provide a counterweight to the market. First, they can bring enough resources to bear on the market to shift momentum. Second, the news that a well-known (and savvy) value investor has bought (or sold short) a stock may lead investors to reassess the price and remove or reduce market mistakes. Finally, activist value investors with enough heft may be able to get companies to remove some of the sources of market misunderstanding, pushing for (and getting) companies to spin off or divest non-core assets and increase accounting transparency.

Activist value investing

As the description should make clear, activist value investing requires significant resources (to acquire large stakes in publicly traded companies) and persistence (it takes time to get management to change its ways). By its very nature, it also requires concentrated portfolios, since you cannot contest managers at dozens of companies at the same time.

Most institutional investors are ill suited for activist value investing, since they do not have the time horizon to wait for activism to pay off or the stomach to challenge incumbent managers. It is ironic, therefore, that some of the first attempts at activism in recent decades came from institutional investors like CALPERS, the California Public Employee Pension fund. While activist institutions remain the exception, there are still mutual funds (mostly small) that play the activist game. The early eighties also saw the coming to age of "corporate raiders", who targeted what they saw as bloated corporations and demanded change. That tradition remains alive in the individual activists such as Carl Icahn and Bill Ackmann, among others, who publicly target firms for change. Finally, the last two decades has seen some hedge funds and private equity investors (with KKR and Blackstone being leading examples) that have made activism the centerpiece of their investing strategy, often using leverage as their way of bridging the funding gap.

While all three groups of activist investors start with the same core premise, i.e., that you can make money by targeting the right firms and acting as catalysts for change, they do vary on who they target, what they do at these targets and how much excess return they generate from their investments. In the table below, I summarize what studies of the three groups have uncovered on each of these dimensions:

In summary, institutional investors have pushed primarily for changes in corporate governance and seen little payoff to their activism. Individual activists have targeted unprofitable, poor performing companies, agitated for deploying assets to more profitable uses and higher dividends, and the survivors have generated superior returns (though the unsuccessful ones drop out quickly). Hedge fund activists have behaved more like passive value investors in the companies that they target, often fail at getting companies to change and if there are excess returns on average, they accrue to a few investors at the top of the pile.

Strategies for the rest of us

Given that most of us do not have the resources to be activist value investors on our own, is there a way to still make a play with this approach? Here are two alternatives:

a. Follow the activists:

You could invest in companies that have been targeted by activist investors and try to ride their coat tails to higher stock prices. Since the bulk of the excess returns are earned in the days before or on the announcement of activism, there is little to be gained in the short term by investing in a stock, after it has been targeted by activist investors. In the long term, you can perhaps make money by focusing on the right activists, looking for performance cues (improved operations) at the targeted firms and hoping for hostile acquisitions. Overall, though, a strategy of following activist investors is likely to yield modest returns, at best, because you will be getting the scraps from the table.

b. Lead the activists:

You can try to identify companies that are poorly managed and run, and thus most likely to be targeted by activist investors. In effect, you are screening firms for low returns on capital, low debt ratios and large cash balances, representing screens for potential value enhancement, and low insider holdings, aging CEOs, corporate scandals and/or shifts in voting rights operating as screens for the management change. The first part should be easy to do but the second part will be more challenging, requiring a mix of quantitative and qualitative assessments. To help on the first, I did a preliminary screening to arrive ata list of 25 companies that trade at less than 8 times EBITDA, have returns on capital 7.5%, book debt to capital ratios 10%, cash as % of value>10% and insider holdings 10%. The rest is up to you!

Perferendis ad qui qui voluptatem nisi ex. Blanditiis quidem sed eligendi consequatur mollitia fugiat distinctio. Consequatur quaerat ipsum dolore vero iste. Iusto numquam sequi consequatur facere et vitae.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...