Trust Bank

An institution that helps people manage their trust and enables customers to put assets into a trust which the trustee then administers.

What Is A Trust Bank?

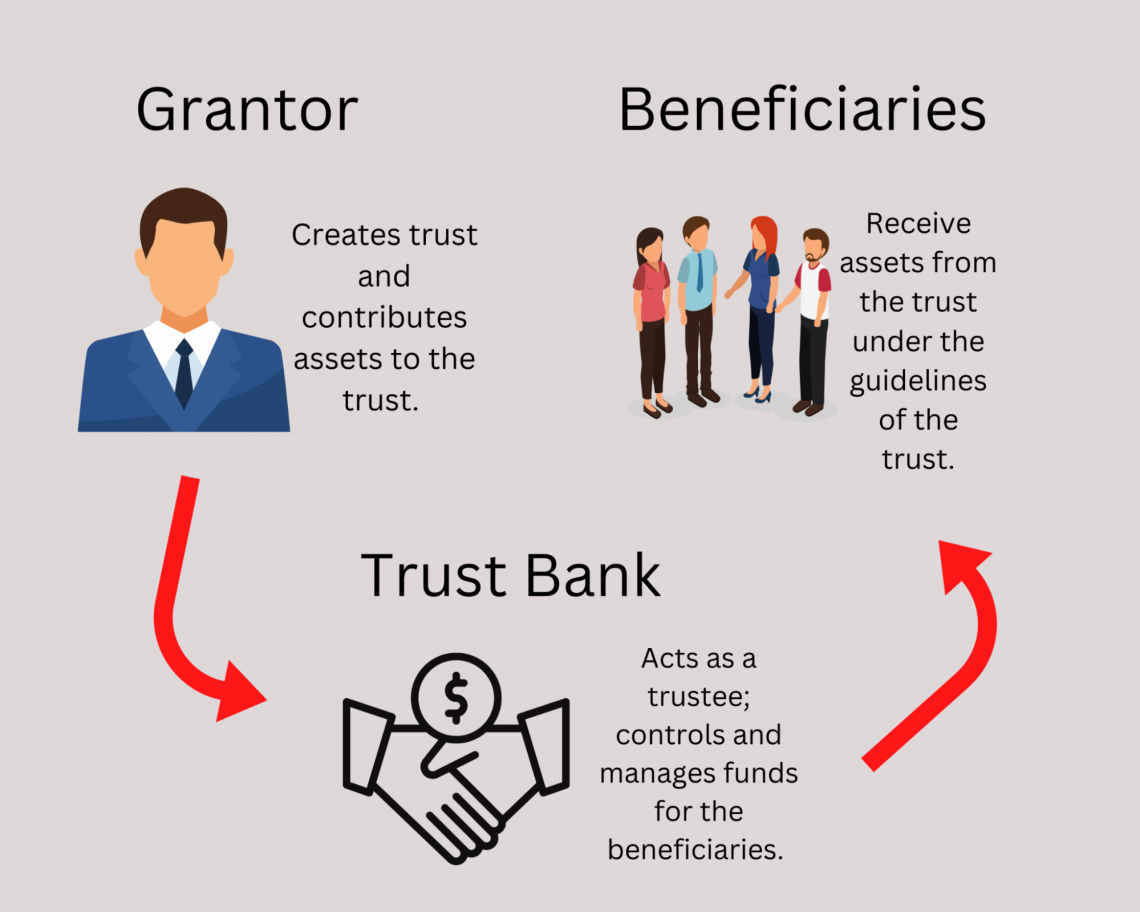

A trust bank is defined as a financial institution that permits its customers to engage in transactions through contracts called "trusts." In these transactions, trust banks act as trustees in the exchange of assets between a client and the beneficiary(ies).

It is similar to a regular bank; however, this particular financial institution specifically handles trusts. It helps people manage their trust. It enables customers to put assets into a trust that the trustee administers.

It serves as a corporate trustee that offers trustee services and can be tied to or not tied to a bank. Banks, on the other hand, manage various financial transactions, such as deposits and loans.

Trust banks provide a range of services. These services include

- Investment Trusts

- Will Trusts

- Estate Liquidation

- Inheritance Consulting

- Pension Business, and

- Asset Formation Trusts

A trust bank performs various duties to ensure that a person’s will or trust is distributed according to the legal terms and process. They handle all sorts of assets, including liquid and non-liquid.

Departments within the bank work with their clients to handle matters regarding security and legal regulations, and they also act as fiduciaries on behalf of the client.

Key Takeaways

- A trust bank, also known as a trust company or fiduciary bank, is a financial institution that specializes in providing trust and fiduciary services to individuals, families, businesses, and institutions.

- Trust banks manage assets, administer trusts, estates, and retirement plans, and act as custodians for assets held in trust or investment accounts.

- Trust banks are subject to regulatory oversight by government agencies, such as banking regulators or securities commissions, depending on the jurisdiction and services offered.

- Trust banks are embracing digital transformation, offering online platforms, mobile apps, and digital wealth management solutions to enhance client experiences and streamline operations.

Understanding Trust Banks

A trust bank is a financial organization that acts as a fiduciary, agent, or trustee that authorizes the bank’s clients to execute transactions.

A trust is a contract that enables a person or institution to hold and manage title assets legally. Trust companies perform the corporate trustee role that can either be connected to a bank or not have a direct relationship with the bank.

Although there is a circulating stigma that trusts are only for the wealthy and powerful, it is not entirely true. They are helpful tools for anyone who owns money or assets they wish to pass down securely with proper care and security.

Trust funds are legal deeds that permit individuals to place their assets into special accounts to benefit another person or organization.

They are a long-term strategy for ensuring that your money is passed on to your children or other loved ones. Trust banks help influence family financial behavior by providing basic fund management rules.

These banks work specifically to meet their client's objectives and support those clients' efforts through assistance with investments.

They differ from regular banks because traditional banks mainly deal with deposits, loans, and other securities that aren’t tied to investments.

Inheritance funds can be complex and challenging to set up, which is why they often require the assistance of an attorney. However, today, plenty of online tools can help you do the process yourself.

Some examples of trust bank companies include CoAmerica, JP Morgan Trust Company, Northern Trust, Bessemer Trust, and U.S. Trust.

If you wish to make a will for distributing assets, you would need to open a trust account that provides tight rules for how those assets are distributed.

For example, if you want to give your real estate to future generations, the trust would outline who will receive it and under what conditions.

What is a Trust?

A trust is a legal agreement that dictates the rules regarding how the trust will operate for all the parties involved.

An individual's assets are combined into a trust, which has extensive control over how the money is used. They can be created under your will and composed while alive.

Depending on the types of assets and mandates of the account, trusts can be as simple as riding a bike or as complex as explaining the stock market to a middle schooler.

Inheritance funds can help confirm that your assets are dispersed and regulated according to your wishes. They are also beneficial for helping you build significant wealth, regardless of how small or large your start.

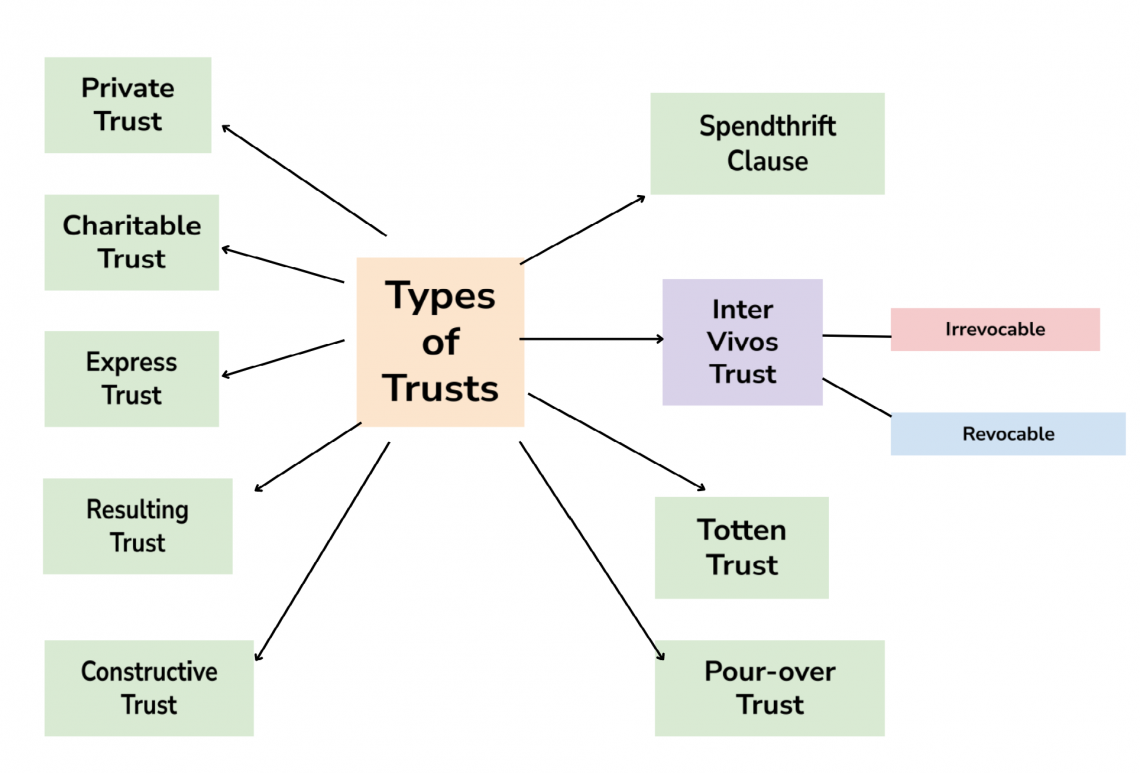

Types of Trusts

There are multiple categories of trusts, depending on what you wish to give to the bank for future holding.

Some examples include:

- Revocable Living Trusts

- Irrevocable Trusts

- Charitable Trusts

Let us understand them below.

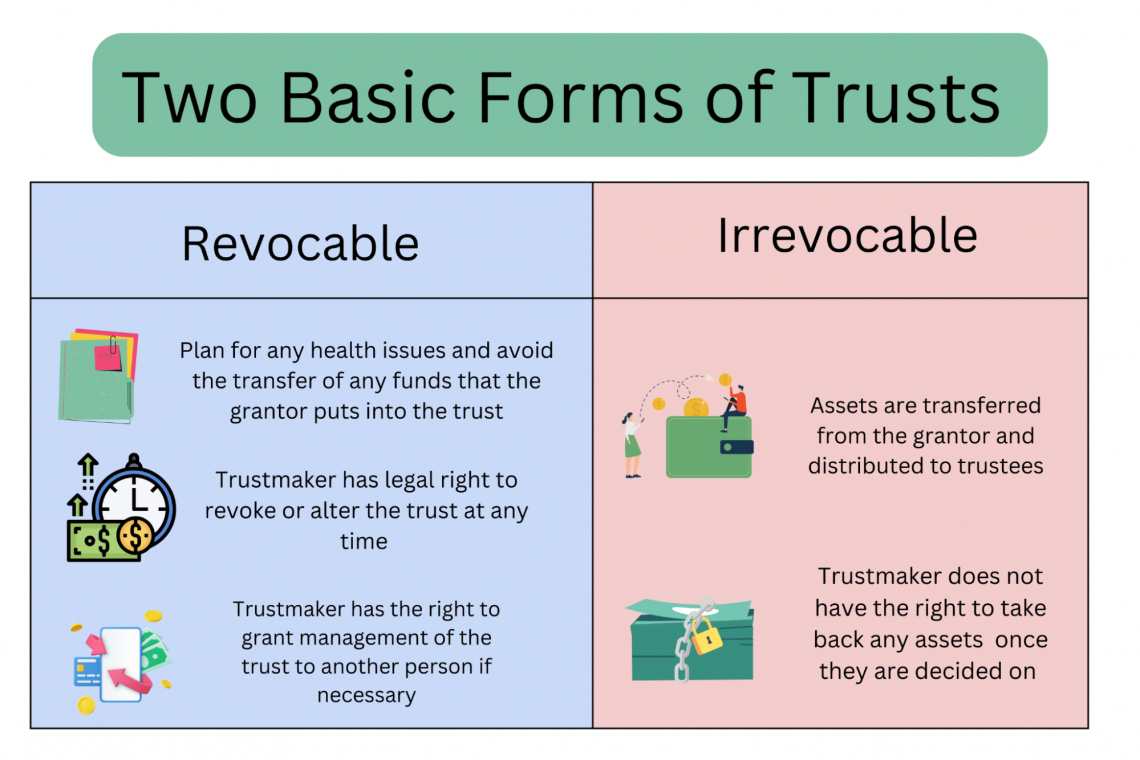

Revocable Living Trusts

A revocable living trust would allow you to control what happens to your assets during your lifetime. In contrast, depending on state requirements, an irrevocable trust usually cannot be changed after it is established.

In some ways, a revocable living trust is like a will since they both reflect a person’s wish for asset distribution and what should be included in the taxable estate.

Some reasons for considering a revocable trust may be that you own specialty assets, hold assets in multiple states, or have health concerns.

Irrevocable Trust

An irrevocable trust is different since the asset distribution conditions usually cannot be changed, hence the word “irrevocable.”

Irrevocable trusts can be created for various reasons, such as giving more financial security to your family or loved ones and, in some instances, gaining additional tax benefits.

Charitable Trust

A charitable trust is irrevocable; however, this specific trust guarantees that any asset stated in it is distributed to a charity or other type of charitable organization. Two main types are charitable lead trusts and charitable remainder trusts.

With a charitable lead trust, you allocate an income stream to a qualified charity for the required time. At the expiry of the specified period, any remaining funds are distributed to selected individuals.

With a charitable remainder trust, you would allocate an income stream to a beneficiary. After the death of the final income beneficiary, the remainder of those assets would be distributed to qualified charities.

Functions Of Trust Banks

The functions of a trust bank are essential for it to cater to its clients. These hyper-specialized services provided to its clients can range from corporate and retail banking to financial and investment services.

Some of the functions of trustee banks are as follows:

- Corporate Banking: As a corporate bank, trustee banks can provide tailor-made financial solutions to their clients like trade financing, corporate loans, cash management, and treasury management.

- Retail Banking: Trustee banks offer basic banking services like savings accounts, loans, and debit cards. They can also provide other financial services to their individual and corporate clients.

- Investment Services: Assisting their clients in asset investment and management is another function of trustee banks that can help their clientele achieve their financial goals and objectives.

- Foreign Exchange Services: These services are for clients engaged in international businesses and investments that require currency conversions. They may also prove to be helpful in conducting cross-border transactions without any hassle.

- Trade Finance: Trustee banks can offer financial solutions in documentation, letters of credit, and trade and export financing for clients engaged in imports and exports trade businesses.

Objectives Of Trust Banks

The objectives of trust banks can be classified as follows.

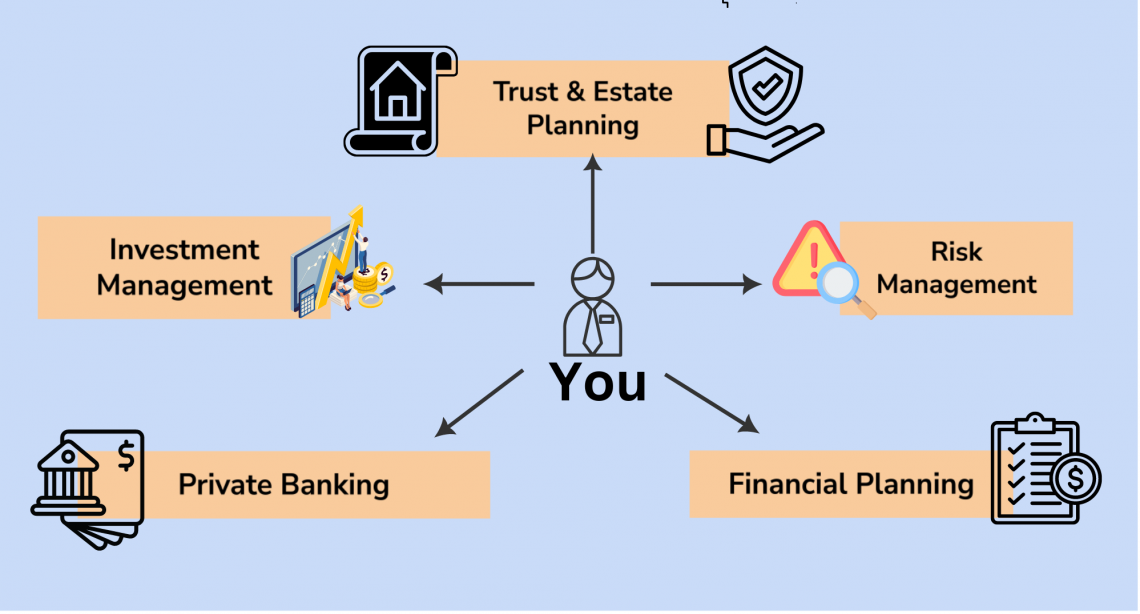

- Wealth Management: Trust banks act as financial advisors to individuals, families, and corporations to manage wealth and assets. They also provide services in investment management, financial planning, and estate planning.

- Fiduciary Services: Trust banks act as fiduciaries, holding assets and managing them in the interest of clients. Trustees, executioners, estate administrators, trust administrators, and retirement planners, are all fiduciary duties of trust banks.

- Estate Planning: Trust banks can act as an estate planner and help their clients minimize estate taxes.

- Asset Protection: Protection of assets from creditors, lawsuits, and other risks is one of the most important tasks for a trustee. Trustee banks can develop legal plans and structures to protect assets from potential dangers.

- Corporate Trust Services: These banks can act as trustees in bond issues, manage escrow accounts, and ensure regulatory compliance for corporations and municipalities.

- Custodial Services: Trustee banks provide custodial services by safeguarding clients' assets and securities. They also safeguard, settle, and process corporate actions.

- Charitable Donations: Trustee banks establish and maintain charitable trusts, foundations, and donor-advised funds.

- Specialized Financial Services: These banks provide specialized and tailor-made financial services to high-net-worth individuals, professionals, families, or institutional investors.

- Risk Management: Trust banks can help their clients assess and manage financial, market, credit, and operational risks. They services may also be extended with portfolio management and insurance solutions.

- Regulatory Compliance: The bank ensures that clients comply with regulatory requirements related to anti-money laundering (AML) laws, know-your-customer (KYC) regulations, and fiduciary standards.

It is interesting to note that trustee banks' objectives encompass financial services, asset management, and aiding clients in achieving financial goals within the appropriate laws and regulations.

Advantages Of Trust Banks

The advantages of working with trust banks provide the following benefits:

- Tax Efficiency: Trusts can provide benefits and advantages to their clients by assisting them with the transfer of assets in a tax-efficient way. Minimizing the income tax liability of the client.

- Flexibility: Trustee banks provide the flexibility of managing or distributing assets according to the client's preferences and legal obligations. This ensures that the assets under the safekeeping of trusts are managed and distributed according to the wishes of its clients/settlor.

- Investment Opportunities: Acting as financial advisors, trusts provide various investment opportunities by separating monetary claims. These monetary claims can include mortgage loans with financial institutions, and real estate, and packaging them into financial instruments.

- Stock Transfer Agency Services: Trusts serve as shareholder list managers for stock-issuing companies and provide consulting services related to corporate stock practices, shareholder list management, cash dividend management, share acquisitions, and compliance with appropriate legislation.

- Professional Services: Trusts provide a wide range of professional services that include investment management, estate administration, and services which may include acting as a trustee, executors, or guardians.

Other advantages may include their participation in asset protection, real estate management, inheritance-related services, and acting as financial guides to their clients.

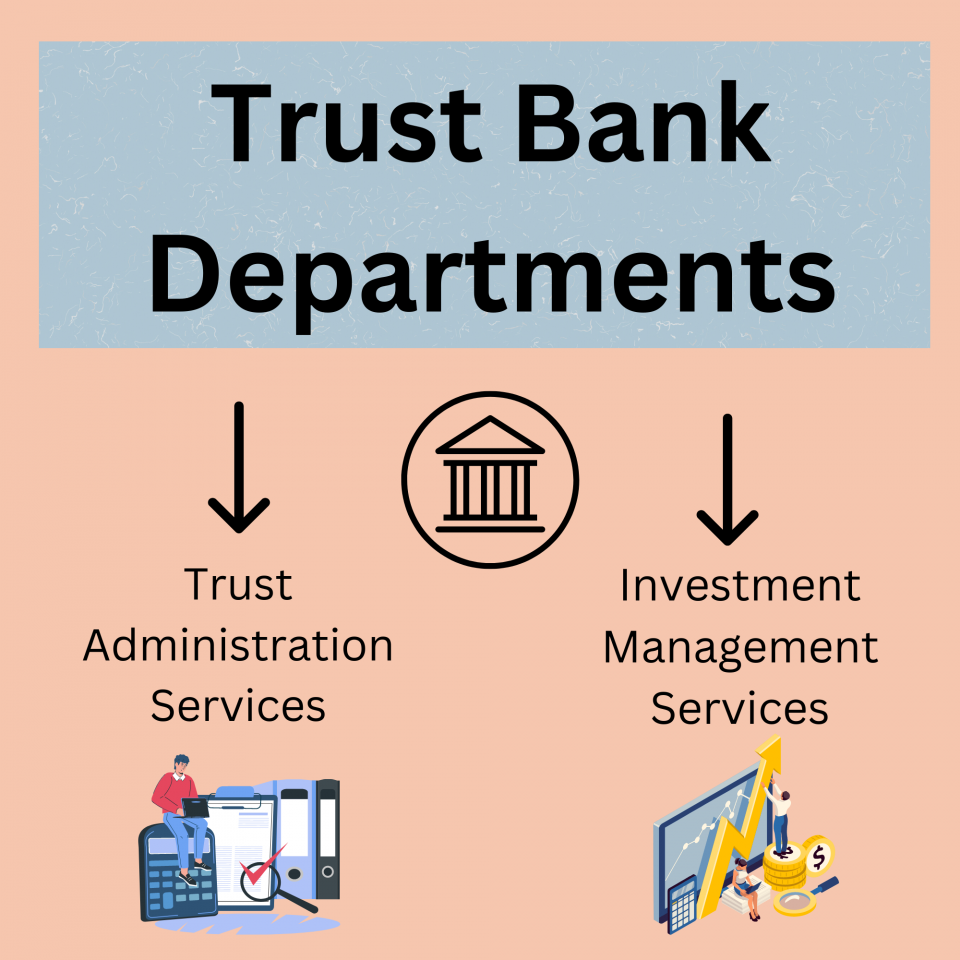

Trust Bank Departments

Trust banks help individuals or entities manage their monetary or non-liquid assets and ensure that they are distributed in a precise legal, and organized manner that complies with the intentions of the guarantor.

Financial institutions dealing with trusts and trust accounts have different departments that pertain to different types of trusts and intentions of what to do with those funds.

Departments within trust companies are designed to work with all types of people who wish to instill those trusts.

To do so, they must fulfill many roles relating to the creation, maintenance, and issuance of those trusts.

For instance, suppose your grandpa purchased a block of Apple stock and decided to hold it in a trust until a future date. The bank trustee can guarantee that the stock share is still paying dividends while prohibiting outside grantees from borrowing or selling against that share.

Departments within these banks also assist in finding the present or future values of assets and how to distribute them over time in the best logical manner.

Note

Trust administration and investment management are the two main sectors of service for directing the trusts in a person’s account.

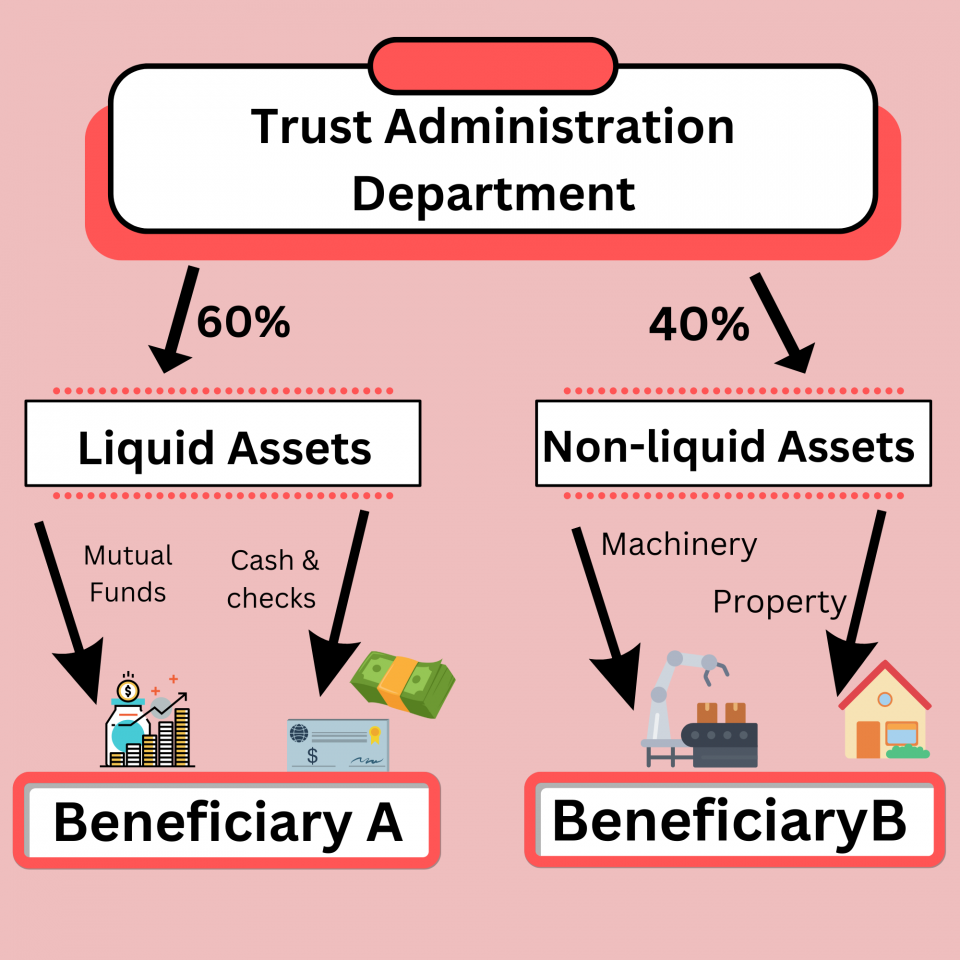

Trust Administration Services

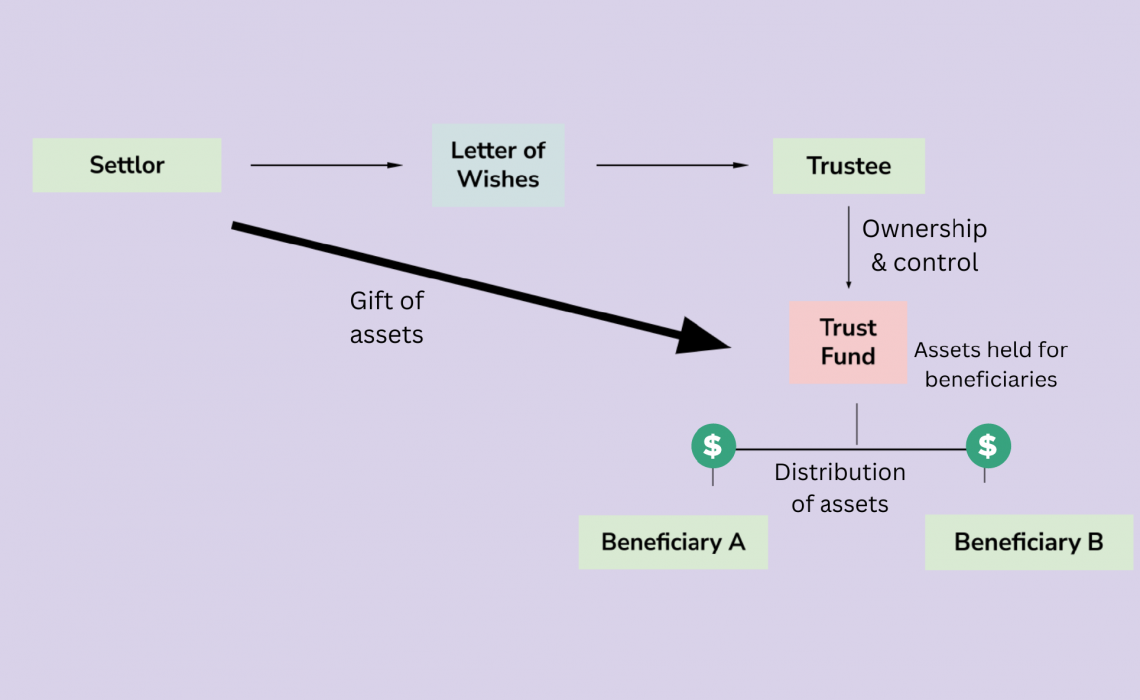

Trust administration involves transferring funds and other trust assets in accordance with the trust terms. The grantor dictates the contract's details, which can vary depending on the case or circumstance.

Administrators take on multiple functions when it comes to managing funds. This includes mainly financial and legal duties.

For most trusts, the bank administrator's critical roles are to collect dividends, ensure asset distribution to the correct beneficiaries, and file tax returns.

Some of the functions of this department of the financial institution are to:

- Serve as a trustee

- Distribute assets

- Assume legal duties

Additionally, they can extend their insurance to confirm that the trust securities have coverage in the event of a loss.

Investment Management Services

Investment management services within a trust institution include performing the duties of investing and divesting trust assets that adhere to the trust requirements.

When managing investments, most trust bank department divisions follow the traditional classes of assets, which are usually stocks, bonds, cash, private businesses, and real estate.

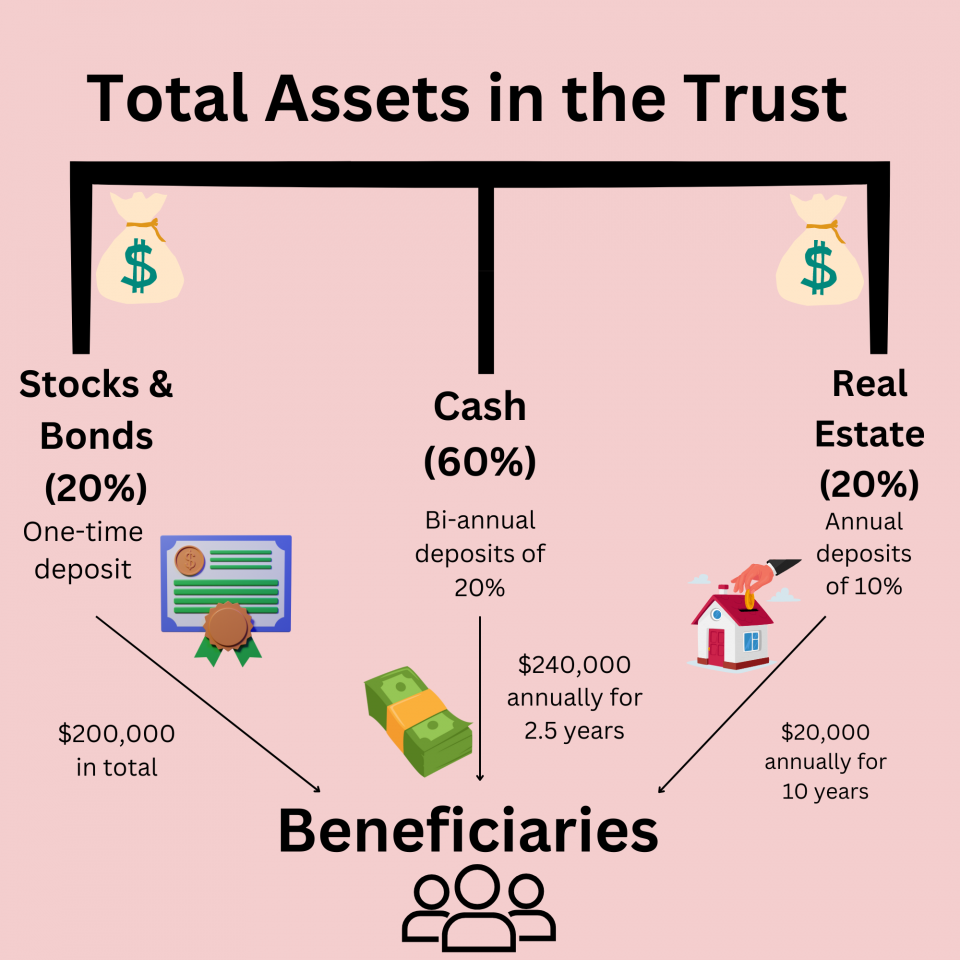

For example, say you put $300,000 in a trust for your grandchildren to grow that wealth slowly over time.

The investment agent may manage a diverse portfolio of financial holdings, including blue-chip stocks, treasury bills, real estate investments, and gift-edged bonds.

Bank services dealing with investment categories perform similar but slightly different roles than those handling administration services.

Some of these roles include:

- Handling specialty assets

- Upholding standards of care

When it comes to ensuring security over trusts, investment management departments tend to be more conservative than those of a standard brokerage account since the advisers act as fiduciaries.

To ensure the utmost security over a client’s funds, the investment management agent must treat those funds as if they were their own.

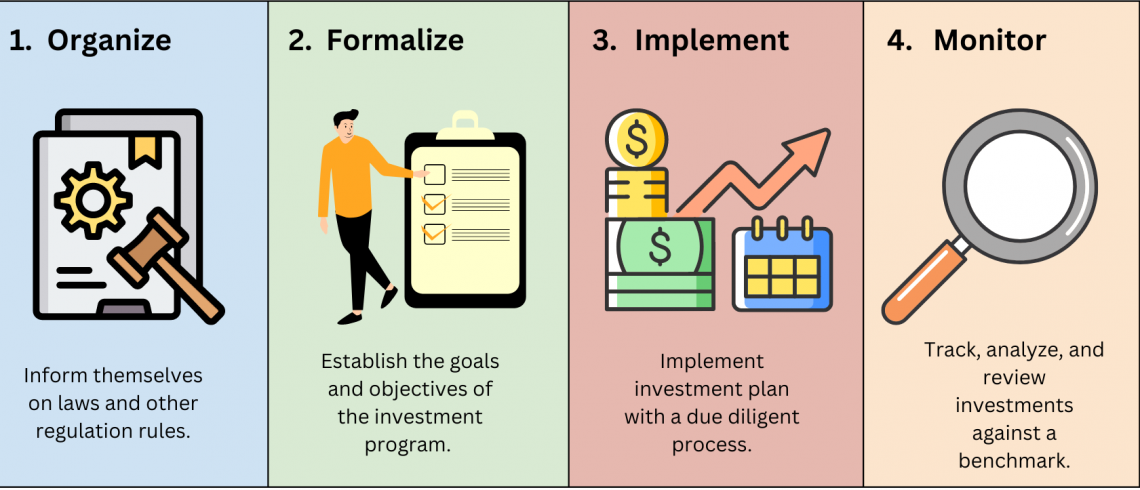

Creating a Trust

The main reason for fabricating a trust is to have control over who receives your securities and how it’s done.

Creating any sort of will, revocable or irrevocable trust, begins with examining your goals and intentions, especially since it is a beneficial financial instrument for your overall wealth plan.

Note

Before jumping into the process, it is essential to consult your attorney and wealth advisor to decide your objectives so that they can make sure that the necessary regulations are set up in your plan.

You should consider hiring a trust bank company. Before doing this, you must consider the following questions regarding your plan.

Will you choose your trustee, or will you need to hire one from the bank? Is your motive to invest your assets or to simply keep them guarded? Will you need assistance with composing the rules? Are your assets standard or niche?

Many companies handle trust securities, and it is also necessary to figure out which bank would be most suitable for you and your financial plan.

Before deciding which bank to work with, you should consider if that bank is innovative and if the services are easy to use.

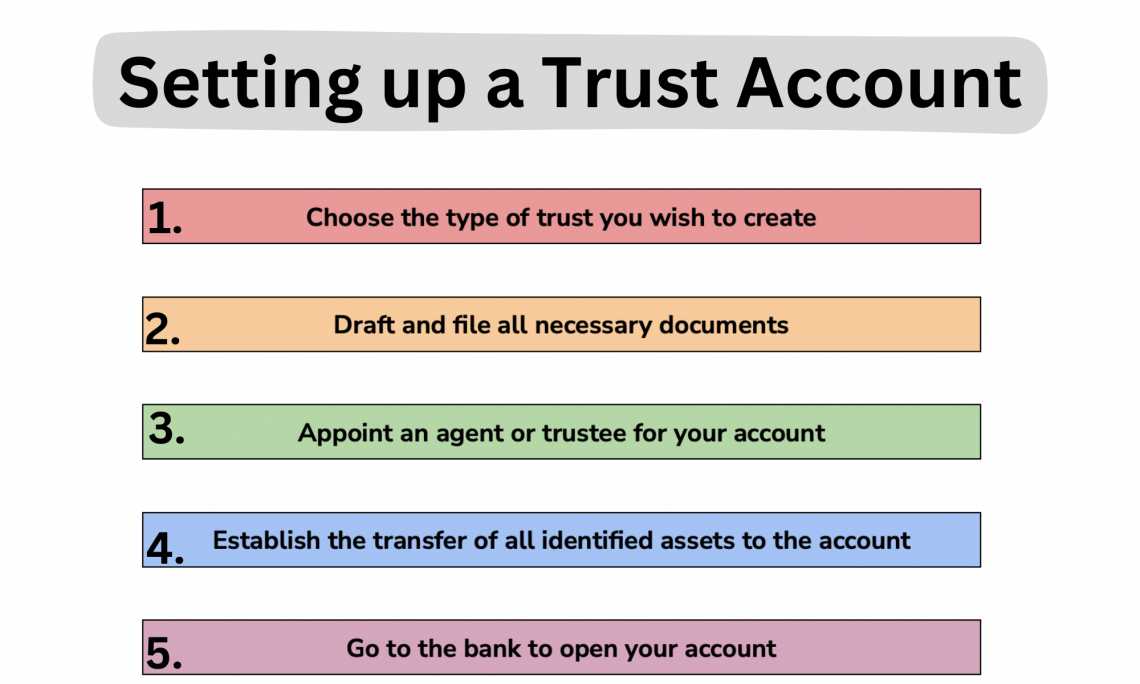

Before creating any type of trust, you must first set up a trust account. The process for setting it up depends on several things, including the kind of trust you wish to place your assets in and the beneficiary or beneficiaries that will receive those assets.

Trust Bank Account

To set up an account, you must choose how your trust’s assets will be managed and distributed.

Then, you must appoint a trustee or group of trustees, such as your attorney or family members, to verify the motive of the trust and govern and allocate the funds according to your goals.

It is essential that you also determine how you want your funds distributed.

This could be a lump sum on a specific date or in specific quantities paid at regular intervals, such as yearly, monthly, or biannual.

The next step is to transfer your assets into an account after you consult your agent or attorney and choose which bank to use.

To do so, you need to choose the amount of money you want to put into your account. Trust funds can be categorized into a range of assets, such as cash, stocks, bonds, real estate, cars, artwork, family items, collectibles, etc.

You can place these assets into a fund all at once or make a series of deposits over some time.

If you choose to transfer these assets into the trust from a different bank or financial institution, various paperwork would need to be completed to warrant the process.

Once your assets are transferred, and the trust is funded, your trustee or agent will be responsible for supervising those assets in accordance with the contract for the benefit of the beneficiary and the trust.

If you own various holdings and securities in your trust, it would be wise to contact an attorney to confirm that your faith is properly set up and that the administrative duties are operating smoothly.

or Want to Sign up with your social account?