In my last post, I looked at HP's disastrous acquisition of Autonomy for $11 billion in 2011 and its subsequent write off of $8.8 billion. While it stands out as a particularly egregious example of a bad deal, it is unfortunately not the exception. In fact, the evidence suggests that a growth strategy built around acquisitions, especially of other publicly traded firms, is more likely to fail than succeed. To back this statement, you can look at three pieces of evidence:

(a) the behavior of the acquiring company's stock price, around the announcement of an acquisition

(b) the post-deal performance (stock price & profitability) of firms after acquisitions

(c) the overall track record of acquisition-based growth strategies, relative to other growth strategies

The acquisition date: Uninformed investors or Delusional managers?

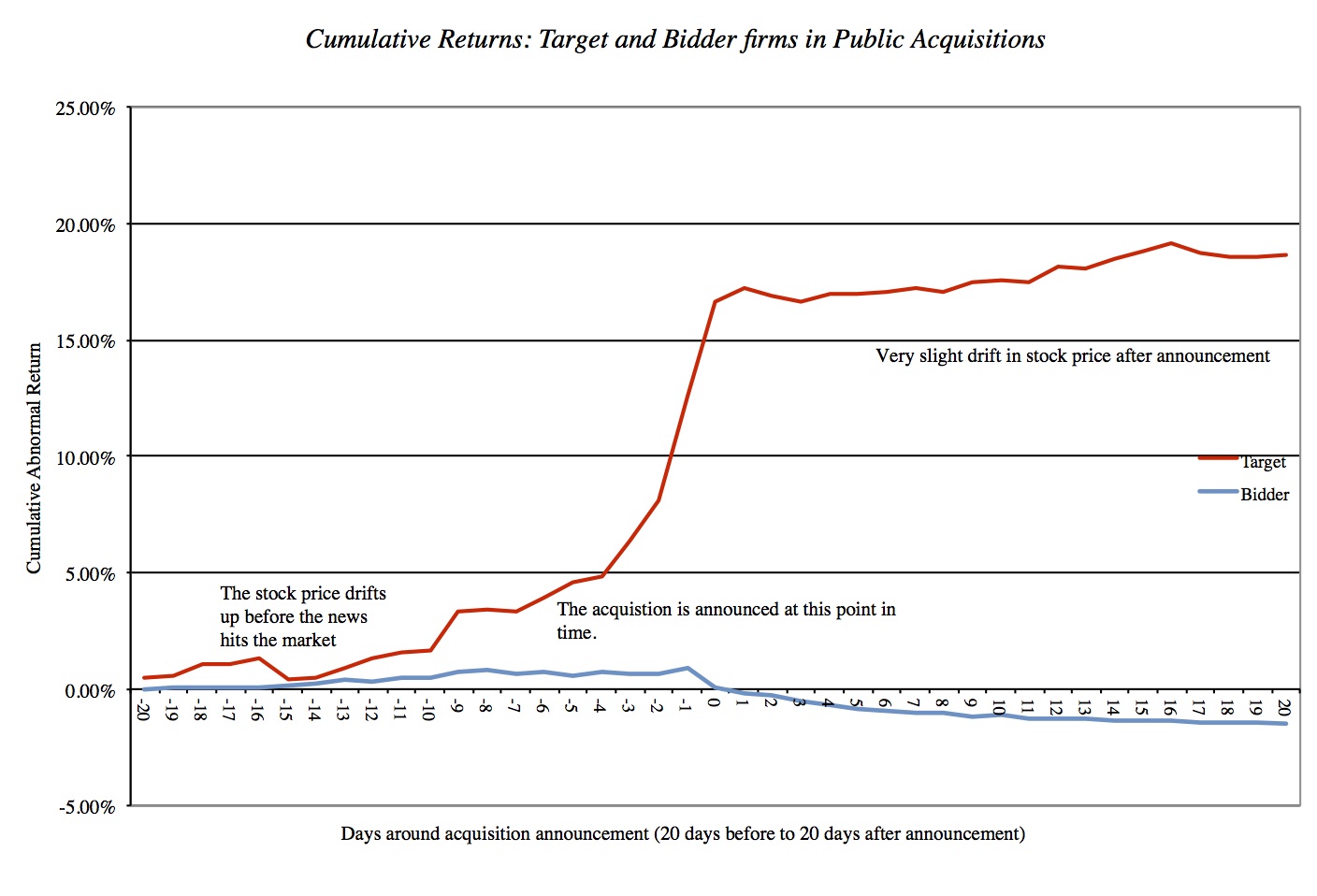

When an acquisition of a publicly traded company is announced, the attention is generally on the target firm and its stock price, but the market's reaction to the event is better captured in what happens to the acquiring firm's stock price. In this figure, a look at the target and acquiring firm stock behavior in the twenty days before and after the acquisition announcement across hundreds of acquisition announcements.

The winner in public company acquisitions is easy to spot and it is the target company stockholders, who gain about 18% over the 41 days. On average, bidding company stockholders have little to show in terms of price gains; the stock price for acquiring firms drops about 2% during the announcement period and about 55% of all acquiring firms see their stock prices go down. Note that while the percentage price drop is small (relative to the price increase for the target firm), acquiring firms are typically much larger than target firms and the absolute value that is lost by acquiring firm stockholders from acquisitions can be staggering. A study of 12,023 acquisitions by large market cap firms from 1980 to 2001 estimated that their stockholders lost $218 billion in market value because of these acquisitions. While this number was inflated by some especially bad deals done between 1998 and 2000, they illustrate the potential for massive value losses from acquisitions and the reality that one big, bad deal can undo decades of careful value creation in a company.

There is one final interesting statistic that can be gleaned from the announcement date market reaction. If you take the cumulative market value of the target and acquiring firms, just before the acquisition announcement and just after, that combined value increases, on average, across mergers. For better or worse, this is what the market seems to be telling us at the time of acquisitions announcements: it believes that there is value added from synergy or other sources in the typical merger, while at the same time also believing that acquiring firms over estimate the value of the synergy and pay too much.

The long term: Post-deal blues?

The defense that is offered by acquiring company managers, when confronted with the market's negative reaction to the acquisition announcement, is that the reaction is rooted in ignorance. Acquiring company managers claim to have access to information and forecasts that stockholders don't have and argue that they are in a better position to value "synergy" and "control". It is of course true that managers have more information on target firm than their stockholders do, but the proof is ultimately in the pudding. To make a judgment on whether this superior information pays off in superior performance, let's look at whether acquiring firms deliver on the promised synergy and other benefits.

Post-deal stock price performance: KPMG studied the 700 biggest mergers between 1996 and 1998 and compared the stock price performance for a year after the deal was closed to that of the peer group to conclude that 83% of the companies underperformed after acquisitions. Thus, the negative reaction to acquisition announcements does not seem to dissipate over longer periods. In some good news, KPMG has updated its M&A study five more times since its 1999 study and reports that there has been some improvement between 1999 and 2011. While only 31% of deals made in the last study (looking at 2007-2009 deals) were value adding, that is an improvement over the 17% from the 1999 study.

For better or worse, some companies choose to grow primarily through acquisitions and it is true that some succeed. For instance, Cisco transformed itself from a small technology company to the largest market cap firm in the world (very briefly in 1999) by acquiring dozens of other companies.

Firms are often attracted to an acquisition-based growth strategy, because it seems to offer a speedier pathway to success, but acquisitions are not the only option for growth. A company can develop new products, take existing products in new markets or try to capture a higher market share of an existing market. The question then becomes not whether a company should grow, but the most efficient way to seek out that growth. Drawing again on a McKinsey study of different growth strategies in the consumer goods industry over several decades, we see a disturbing picture.

The payoff to investing in growth is greatest for new-product development, where a million invested in the strategy generates additional value of $1.75 million to $ 2 million, and generates the most bang for the buck (with share prices doubling with relatively small revenue growth of 5-6% from the new products). The payoff to growth investing gets steadily worse across the next four strategies and is worst with acquisitions, where a million investing in acquisitions generates between -.5 million to $.2 million in additional value.

There are shades of nuance that are missed in this aggregate picture. As I will note in a later post, there are subsets of acquisition strategies that do better; buying smaller rather than larger companies, private as opposed to public companies and strength-focused rather than me-too acquisitions. Notwithstanding these pockets of success, it remains true that it is difficult to create value with an acquisition-based growth strategy and it becomes even more so as the company gets larger. In fact, Cisco is a good example of the diminishing returns to acquisition-based growth, as the same strategy that worked to great effect in the 1990s worked against the company between 2001 and 2010.

And the disease is spreading

The scariest aspect of the acquisition disease (which destroys value) is that it is now spreading to emerging markets. Emerging market companies, which used to be targets for richer developed market companies, are now in a position to be acquirers and some of them are targeting developed market icons. Looking at the prices they pay, and the practices they adopt, it is also clear that emerging market companies are making the same mistakes that their developed market predecessors did. A study of the stock price behavior in the days before and after the announcement of 114 acquisitions of US companies by Indian companies illustrates the problem.

While the initial reaction to acquisition announcements is positive, market disillusionment with the acquisition sets in quickly and the cumulative returns deplete over time, turning negative as you get to 20 days after the announcement.

Why do companies persist?

Given this history of value destruction, you would think that companies would become more measured in pursuing acquisition-based strategies. That, unfortunately, does not seem to be the case. Not only do we continue to see big, bad deals, but we often see the same company repeatedly making bad deals and the same mistakes repeated over and over by other companies. Not only is there no learning built into the process, but this repeated losing behavior would suggest that there is some collective irrationality at play (a euphemism for insanity) or that the acquisition process is flawed, and in the posts that follow, I will take a closer look at both possibilities. I will begin by by putting the objectives and incentives of the key players in the acquisition process under a microscope, starting with the top managers in both the acquiring and target companies, following up with the "advisors" (investment banks, commercial banks and consultants) on these deals, and ending with the accountants whose job it is to provide information on the deals. I will then look at the mechanics of the process, first focusing on common errors that I see in acquisition valuations and then looking at how best to value "control" and "synergy". I will close with a post on how to improve the odds of success with an acquisition-based growth strategy, drawing on lessons from history.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

very interesting read

Quia laudantium est iste a voluptas inventore. Enim eligendi aperiam ratione similique suscipit. Consequatur iusto quae quia esse non. Animi similique est harum et maxime praesentium consequatur.

Quas ut non et itaque veritatis doloribus. Et ut corporis ipsa.

Et odit et ipsam et nisi. Placeat nisi deserunt asperiores sint. Nam ipsum possimus magni ratione eum. Laudantium repellendus occaecati id minus accusamus magni quod. Deleniti magnam aut maiores voluptas eum. Et sint occaecati non recusandae ea.

Officia sed earum ad fuga voluptatem laudantium exercitationem. Exercitationem sed autem et eveniet. Fuga et at aut sint velit laborum.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...