Historical Cost

An accounting principle that refers to the valuation of assets or liabilities at their original cost incurred to acquire or produce them.

What Is a Historical Cost?

Historical cost, also known as original cost, is an accounting principle that refers to the valuation of assets or liabilities at their original cost incurred to acquire or produce them.

It was created on the idea that its original purchase or production cost can objectively determine the value of an item.

The historical principle records assets on a company's balance sheet at their original cost. This approach is used under the General Association of Account Principles (GAAP) to provide a reliable and verifiable basis for financial reporting.

The approach aligns with the “conservatism” accounting principle to increase the accuracy of the financial statements.

This method relies on actual transactions and objective evidence rather than subjective estimates like current market value or appreciation potential. In this case, the subjective value would be the fair market value, which estimates an asset's worth in real time.

This cost method can typically be used for long-term assets such as PPE (plant, property, and equipment) and specific financial instruments and inventory. Long-term assets should be recorded as their cash equivalent at the time of purchase.

Therefore, determining how to record a long-term asset’s cost includes finding all costs directly related to its acquisition or production.

Short-term assets won’t technically follow this cost principle and will generally be reported at their current market value. This is because they are considered highly liquid, and their fair market value can be determined.

Some examples of exceptions to this cost principle would be:

- Cash

- Marketable Securities

- Accounts receivables

This list needs to be completed, but the assets listed have values less likely to change significantly quickly.

On the flip side, the values of certain assets may change over time due to depreciation. Several factors, such as inflation, changes in market conditions, or technological advancements, can cause depreciation.

Some argue that this cost method is dated. Still, proponents of it argue that it provides a reliable and conservative approach to financial reporting, avoiding potential subjective judgments and manipulation of asset values.

- Historical cost is the original monetary value of an asset or liability at the time of its acquisition or incurrence. It reflects the actual amount paid for the asset or the actual amount received from the liability.

- Historical cost is a fundamental accounting principle under the Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS).

- Historical cost provides a clear, objective measure that can be verified by documentation such as invoices and receipts.

- Historical cost ensures that costs are not undervalued and revenue is not overstated. It also ensures consistency in financial reporting, making it easier to compare financial statements over time.

Understanding Historical Costs

Understanding the historical method involves grasping its underlying principles and implications.

Conceptually, this method is grounded in the idea that the original cost of an asset or liability is the most objective and reliable basis for measurement. It emphasizes the importance of actual transactions and verifiable evidence in financial reporting.

Under this method, assets are recorded on the balance sheet at their original cost. This cost includes the purchase price of an asset and any other direct expenses incurred to bring it into its present condition and location.

Liabilities are also recorded at the amount one purchased the item for. For example, if a company issues a bond with a face value of $1,000, the liability would be initially recorded at $1,000, regardless of whether the bond's market value fluctuates.

Note

The historical method was created to encompass reliability and objectivity in financial reporting. It avoids subjective estimates of an asset's value, which could be prone to biased judgments.

By relying on concrete evidence, the historical method enhances the consistency of financial statements.

Accounting relies on consistency. Once an asset is recorded at historical cost, subsequent changes in its market value are generally not recognized in the financial statements.

Instead, the item continues to be reported at its original cost unless evidence of impairment or an event triggers a different accounting treatment.

Since values are stated at their original price, companies often provide supplementary information alongside the financial statements to give stakeholders a complete understanding of an entity's financial position.

Understanding this cost method requires recognizing its conceptual basis and comprehending how the assets and liabilities are valued.

This method focuses on reliability, objectivity, and recognizing the importance of supplementary information to provide a more holistic view of an entity's financial position.

Note

Historical cost is a widely used accounting principle, but there are alternative valuation methods, such as fair value accounting, which attempts to measure assets and liabilities at their current market values.

Why is the Historical Cost Method Important

The historical cost method is vital in accounting for several reasons.

Here's a detailed explanation of its significance:

1. Objectivity and Reliability

This cost method provides a reliable and objective basis for measuring and reporting the value of assets and liabilities. It relies on actual transactions and concrete evidence, enhancing the credibility of financial statements.

2. Verifiability

Original cost is based on actual transactions and documented evidence, making it easily verifiable. This allows auditors, regulators, and other stakeholders to examine and confirm the accuracy of reported values.

Note

Verifiability is crucial for ensuring transparency and building trust in financial reporting.

3. Comparability

This cost method promotes comparability across different entities and over time. Since it is based on the actual cost incurred, it provides a consistent and standardized approach to valuing assets and liabilities.

This allows for meaningful comparisons between organizations and enables analysis of trends and changes in financial performance.

4. Simplicity and Cost-effectiveness

The simplicity of this method reduces the need for complex and potentially subjective valuation techniques, making financial reporting more efficient and less prone to error.

5. Legal and Regulatory Requirements

In many jurisdictions, accounting standards and regulations prescribe using historical methods as the primary valuation method for certain assets and liabilities.

Note

Compliance with these requirements ensures consistency and facilitates the comparability of financial statements across entities and industries.

6. Stewardship and Accountability

This cost method aligns with the principle of stewardship, where managers are accountable for the resources entrusted to them.

Recording assets at their original cost provides a clear representation of the resources used in the organization's operations.

This information is crucial for assessing managerial performance and holding individuals accountable for their decisions.

7. Risk Management and Prudence

This cost method embodies a conservative approach to accounting, emphasizing prudence and risk management.

It avoids potential overstatement of asset values by recognizing them at their initial cost rather than their potentially fluctuating market values.

This conservative approach helps protect stakeholders from potential misrepresentation or excessive optimism.

8. Long-term Planning and Investment Decisions

This cost method provides a stable and consistent basis for long-term planning and investment decisions.

Since it focuses on the original cost, it allows managers to assess the profitability of assets over their useful lives. While this cost method has limitations, such as not reflecting current market values or potential appreciation, it remains a vital accounting principle.

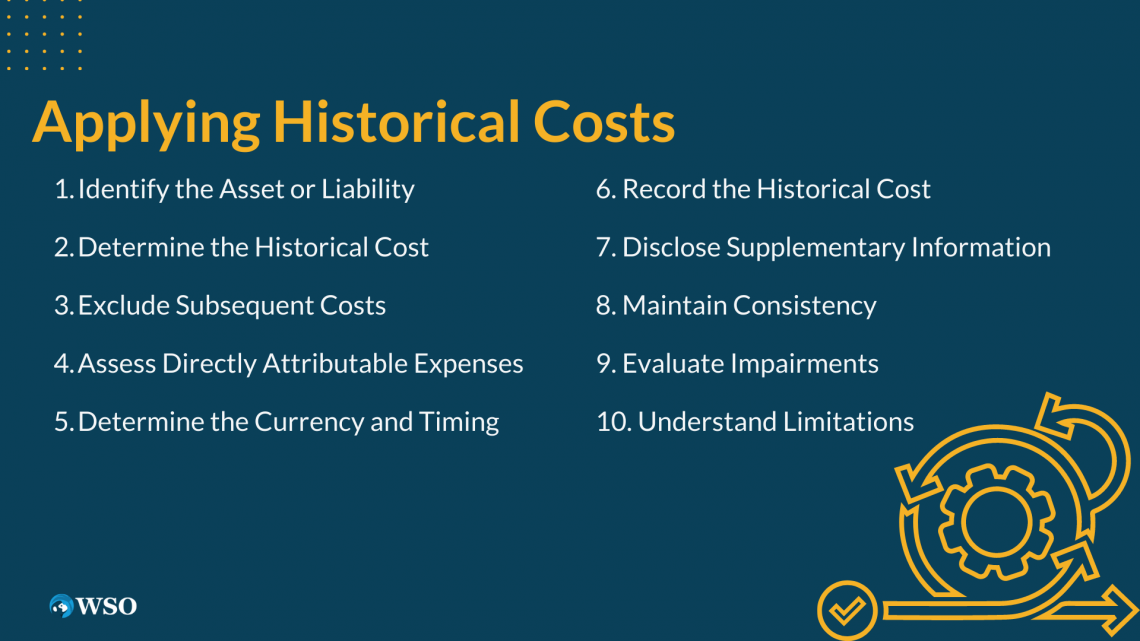

Applying Historical Costs

Applying the historical cost method in accounting involves several steps and considerations. Here's a detailed explanation of how to apply this method effectively:

1. Identify the Asset or Liability

Determine the specific asset or liability to be valued using the historical method. This usually includes long-term assets such as property, plant and equipment, financial instruments, or inventory.

2. Determine the Historical Cost

Gather information about the original cost incurred to acquire or produce the asset or liability. This may involve reviewing purchase invoices, contracts, receipts, or other relevant documents.

The historical cost includes the actual purchase price or production cost and any directly attributable expenses.

3. Exclude Subsequent Costs

Exclude any costs incurred after the initial acquisition or production of the asset or liability. The historical cost is based solely on the actual expenses and does not include subsequent improvements, maintenance costs, or any changes in market value.

4. Assess Directly Attributable Expenses

Identify and include any directly attributable expenses related to the acquisition or production process. These expenses should be specific to the asset or liability in question and incurred to bring it into its present condition and location.

Examples include delivery, installation, legal, and transportation charges.

5. Determine the Currency and Timing

Ensure that the original cost is recorded in the appropriate currency and reflects the prevailing exchange rates at the time of the transaction.

Note

The transaction date accurately reflects the historical context and adjusts for any changes in prices or inflation over time.

6. Record the Historical Cost

Once the original cost has been determined, record it in the appropriate accounts on the balance sheet.

Depending on the nature of the asset or liability, it may be classified under different categories such as property, plant and equipment, financial assets, or inventory.

7. Disclose Supplementary Information

While the historical cost is the primary valuation method, consider providing supplementary information alongside the financial statements.

This could include additional disclosures on market values, fair values, or other estimates that provide stakeholders with a more comprehensive understanding of the asset or liability's current economic value.

8. Maintain Consistency

Consistency is crucial when applying this cost method. Ensure the method is consistently applied across similar assets or liabilities within the organization.

This promotes comparability and avoids confusion or inconsistencies in financial reporting.

9. Evaluate Impairments

Regularly review the carrying amount of assets to determine if any impairment indicators exist.

If an asset's historical cost exceeds its recoverable amount, an impairment loss should be recognized, and the carrying value adjusted accordingly.

10. Understand Limitations

Recognize the limitations of the cost method. While it provides a reliable and verifiable basis for financial reporting, it may not reflect the current market value, potential asset appreciation, or depreciation over time.

Note

Consider providing supplementary information to address limitations and concerns.

By following these steps and considering the specific requirements of each asset or liability, you can effectively apply the historical cost method in accounting.

Historical Cost Example

The historical cost principle is best represented by working through real-life applications. Let's consider an example to illustrate its implications.

ABC Industries is a manufacturing company that purchases machinery for its production line. The machine costs $100,000, and additional costs such as transportation and installation amount to $5,000.

According to the historical cost principle, ABC Industries would record the machinery at its historical cost of $105,000.

In this example, the principle is applied to value the machinery at its original cost. Here's a breakdown of how it is implemented:

- Identification of the Asset: The asset to be valued is the machinery purchased by ABC Industries.

- Determination of Historical Cost: The historical cost includes the purchase price ($100,000) and any directly attributable expenses for acquiring the machinery. In this case, the additional costs for transportation and installation amount to $5,000. Therefore, the historical cost of the machinery is $105,000 ($100,000 + $5,000).

- Recordation on the Balance Sheet: ABC Industries would record the machinery on its balance sheet at its original cost of $105,000. This valuation would be reported under the appropriate category, such as property, plant, and equipment.

- Consistency: ABC Industries would apply this principle consistently across similar assets within the company to maintain consistency. This ensures that assets are valued on a standardized basis.

Note

Any costs incurred after the acquisition of the machinery, such as repairs or maintenance expenses, are not included in the historical cost.

Summary

Historical cost is an accounting principle that values assets and liabilities at their original cost. It is based on the idea that the actual amount paid or incurred in acquiring or producing an item is the objective and reliable basis for measurement.

This cost includes the purchase price or production cost and directly attributable expenses. This principle is important because it provides reliable and verifiable information for financial reporting.

For regulatory reasons, companies in the United States must follow this principle under GAAP. GAAP is responsible for making sure financial accounting statements are reliable and accurate.

This principle enhances the objectivity and credibility of financial statements by relying on actual transactions and concrete evidence. It promotes comparability across entities and, over time, facilitates meaningful analysis and decision-making.

This cost method is commonly used for long-term assets. It simplifies accounting processes to reduce the need for complex valuation techniques. Accounting standards and regulations in various jurisdictions often mandate this approach.

Historical cost is an essential and widely used accounting principle that provides a reliable and standardized basis for valuing assets and liabilities. It contributes to transparency, comparability, and the responsible stewardship of resources.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?