Marginal Cost

The costs represent the additional costs a company incurs when producing one more unit of a product, encompassing both variable and direct expenses.

What is the Marginal Cost of Production?

The marginal cost of production represents the additional costs a company incurs when producing one more unit of a product, encompassing both variable and direct expenses.

Producing more goods when a factory runs at full capacity can lead to additional expenses like paying workers overtime.

The marginal cost usually increases as the quantity of production increases. To maximize their total output, manufacturers can use their understanding of marginal cost to inform strategic decisions about resource allocation among production units.

Businesses use the marginal production cost to the unit selling price to determine whether they can produce more units in competitive markets.

Production of an additional unit and sale of that unit becomes profitable when the market price exceeds the marginal cost. Making that unit, however, becomes financially unfeasible if the marginal cost of production is higher than the selling price.

Determining the point at which an organization can attain economies of scale to maximize its production and overall efficiency is contingent upon analyzing marginal cost.

A profit opportunity arises for the producer when the cost of producing a new unit is less than the selling price of each unit.

Businesses should proceed cautiously when considering expanding production, as this may result in step costs related to changes in relevant ranges. Such modifications might necessitate spending money on new machinery or more storage.

- Marginal Cost refers to the additional cost of producing each extra unit. When production rises, the marginal cost tends to rise, impacting resource allocation decisions to maximize overall output.

- When the cost of producing one more unit is less than the selling price of each unit, a profit-making opportunity presents itself.

- The expenses incurred for every extra unit of output are included in the marginal cost of production.

- Organizations can maximize productivity and efficiency by determining the point at which they can attain economies of scale by analyzing marginal cost.

- Businesses in competitive markets decide whether to raise production by weighing the marginal production cost against the unit selling price.

Understanding Marginal Cost

An important idea in managerial accounting and economics, the marginal cost is especially important for manufacturers trying to determine their ideal production level.

Manufacturers closely examine the costs involved in adding one more unit to their production schedules.

The process of producing an extra unit and making money from it after a certain production threshold is met can result in a total cost reduction for the entire product line. Rapidly identifying this critical level is imperative for the optimization of manufacturing costs.

The concept of marginal cost includes all costs that change in response to changes in production levels. For example, the cost of building a new factory that a company needs to increase production is regarded as a marginal cost.

In economic theory, marginal cost is very important because, to maximize profits, a company will keep producing until its marginal cost (MC) equals its marginal revenue (MR).

After this, producing more units is no longer economically advantageous because the expenses outweigh the profits.

Types of Marginal Cost

The Marginal cost of production has the following types:

1. Unit Cost

Unit costs generally adhere to the conventional notion of variable costs, meaning that a commensurate rise in costs accompanies an increase in the production of a single unit.

Use the price of the raw materials needed to make one more smartphone case as an example. These variable costs increase proportionately with each additional unit produced.

2. Batch Cost

The number of batches produced determines the variation in batch costs, not the production of individual units.

Using the coffee mug example again, imagine a ceramic shaping machine that must be brought to the proper temperature before beginning production.

Until production stops, there are no additional costs once it is operating. This startup cost is incurred again when starting a new batch.

3. Product Cost

Product costs are fixed, regardless of the number of batches or units produced. These expenses are closely related to a particular product in a lineup. For instance, the cost of creating and advertising a coffee mug with a holiday theme is independent of the quantity of mugs manufactured.

4. Customer Cost

The number of serviced customers determines customer costs, not any specific production level or product line expansion. Examples include post-purchase servicing or legal fees arising from contractual obligations.

5. Organizational Sustaining Cost

The costs that arise from routine business operations are known as organizational sustaining costs.

Regardless of the volume of production, these expenses must be incurred. These may include things like a company's fixed employee salaries or auditing fees for preparing financial statements for shareholders.

6. Short-term Marginal Cost of Production

When a business temporarily boosts output, short-run marginal costs are revealed.

A business may have limited resources in the near term, and it is up to it to decide how much to produce. To accommodate sporadic demand, modifications such as switching work shifts or adding overtime might be necessary.

7. Long-term Marginal Cost of Production

Additional costs are incurred when a business grows, and all inputs are flexible.

This is known as the long-run marginal cost of production. It frequently entails making significant adjustments, such as increasing staffing levels, expanding manufacturing facilities, or entering untapped markets.

Over time, an organization can more easily adapt to different circumstances to handle increased output levels.

Marginal cost Formula

Marginal cost can be calculated as follows:

Marginal cost = Change in total cost / Change in total quantity

The formula for calculating marginal cost is

MC = ΔTC/ΔQ

where:

- MC represents Marginal cost

- ΔTC represents Change in total cost

- ΔQ represents Change in total quantity

Example of Marginal Cost

If you owned a bakery, producing 100 bread loaves would cost $500 daily. You decide to increase your daily output by twenty loaves to 120 loaves.

The total you pay now is $560.

To determine the marginal cost of making twenty extra loaves of bread:

Change in quantity = 120 loaves - 100 loaves = 20 loaves

Change in total cost = $560 - $500 = $60

Marginal cost = $60 / 20 = $3 per additional loaf of bread

When making 20 batches of bread, the marginal cost of making an additional loaf is $3.

You can choose prices based on this $3 marginal cost knowledge. For instance, you would profit an additional $2 if a loaf of bread sold for $5. Your earnings would rise by $40 if you produced and sold twenty additional loaves of bread.

Marginal cost curve

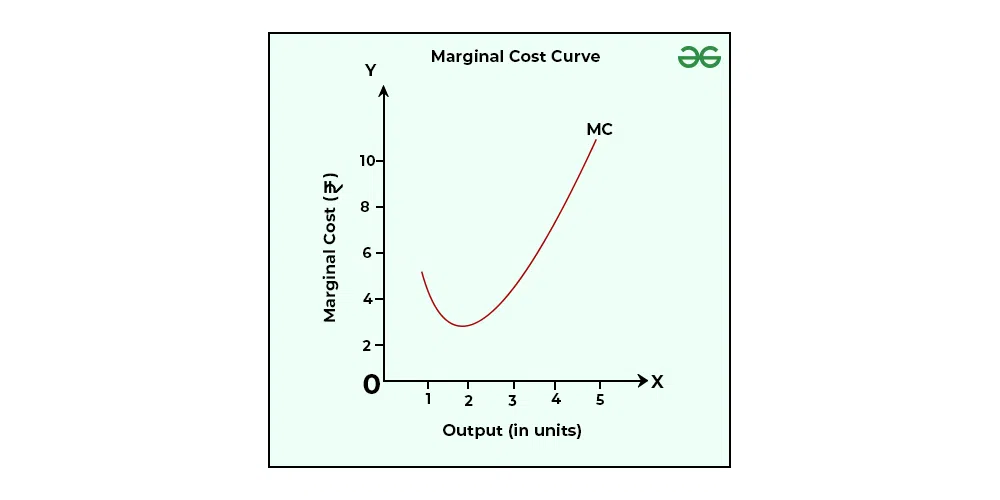

When shown graphically, the marginal cost of producing different quantities of products usually has a U-shaped pattern. The costs are somewhat high at first, but they go down as production reaches the break-even point, at which fixed costs are met.

As a result of the need to make additional investments in labor, raw materials, equipment, and other resources, costs begin to rise as production keeps rising.

The procedures below are how you generate your marginal cost curve:

- Determine Cost Drivers: Be mindful of the elements—such as labor, raw materials, and shipping—that influence your manufacturing costs.

- Marginal Cost Calculation at Various Production Levels: Analyze how costs vary with increasing production levels.

- Graph the Curve: Make a graph using the computed data with the x-axis denoting product quantity and the y-axis denoting cost per unit.

- Examine the Curve: Make tactical choices based on the graph. If you see declining marginal costs, also known as economies of scale, consider raising production. If you observe growing marginal costs (diseconomies of scale), consider holding off on further expansion and looking into efficiency gains.

Note

Setting a price for your product higher than its marginal cost makes sense to maximize profitability. If the price is less than the marginal cost, you might need to modify your pricing strategy or take cost-cutting measures.

Conclusion

When determining the optimal production level to guarantee profitability before costs start to climb, marginal cost plays a crucial role in assisting businesses. It can be compared with marginal revenue to determine profitability and helps monitor changes in variable costs.

The variable and fixed costs that a business incurs when manufacturing a good or providing a service are significantly impacted by inflation. Businesses can design strategies based on marginal cost and marginal revenue to adjust and prepare for these cost variations.

Consider a cloth manufacturer in the fashion industry as an example. In response to rising material costs, they may choose to alter their garment designs, using less expensive materials while maintaining the same retail prices.

As an alternative, a manufacturer of tech gadgets with the authority to determine their prices might decide to increase the cost of their goods in reaction to growing marginal costs.

If price increases exceed the inflation rate, they will be able to maintain or increase their profit margins. However, the pressures of inflation can reduce a company's overall revenue.

Consequently, a business might have to reduce the amount of goods it produces, spend less on raw material purchases, and possibly lay off production and service personnel.

The requirement for additional fixed costs related to growing manufacturing operations may be delayed during a recession-induced business downturn. However, now is the perfect time to put strict cost-control and cost-cutting measures in place.

.webp){kind=link}

or Want to Sign up with your social account?