Recession

A business cycle contraction when there is a general decline in economic activity

What Is a Recession?

A recession is a marked reduction in economic activity in a given area as measured by macroeconomic indicators.

It is typically characterized by two consecutive quarters of economic decline, as reflected in the gross domestic product (GDP) and other monthly indicators, such as an increase in unemployment.

According to the National Bureau of Economic Research (NBER), a government organization responsible for officially declaring recessions, when there are two consecutive quarters of real GDP declines, it is still not considered enough for it to be declared as a recession.

The NBER describes it as a prolonged fall in economic activity accompanied by a decline in prices that typically impacts most parts of the economy, lasts for a long time, and has an impact on real GDP, real income, employment, output, and sales.

The main repercussions are unemployment and depression. According to classic economic sayings, unemployment occurs when someone else loses their job, and depression occurs when you lose yours.

You must have a contingency plan in case of an emergency, especially in difficult economic conditions, as your primary source of income is your job.

Since 1857, economic downturns have averaged 17.5 months in length. Among the longest downturns is the economic crisis of 1873, which lasted 65 months, and the Great Depression, which lasted 43 months.

- Recession is a significant economic decline measured by GDP and unemployment.

- Recessions historically last around 17.5 months on average.

- Causes of recessions include shocks, inflation, debt, asset bubbles, and technological changes.

- Warning signs of a recession include inverted yield curves, declining GDP, real income, employment, and stock market drops.

- Preparation for a recession involves monitoring economic indicators and being cautious with investments.

Understanding Recessions

Since World War II, the impacts have become less severe due to shorter periods of economic decline (approximately 11.1 months). In addition, the Federal Deposit Insurance Corporation and the Federal Reserve (somewhat) managing the money supply means that when a bank defaults, it won't mean losing your life savings.

The Great Recession began in December 2007 and ended in June 2009 and was the longest since World War II. The pandemic, on the other hand, reduced the average length by two months.

A recent economic slowdown due to The Covid-19 Effect ended and began again within two months, making it the shortest slump ever recorded in the United States.

A real estate bubble caused the Great Recession (December 2007-June 2009). Although it wasn't as severe as the Great Depression, its duration and severe effects earned it the same name. It lasted 18 months, almost double the length of recent US troughs.

The Dot Com Effect (March 2001 to Nov 2001). In the new millennium, the United States faced several economic problems, including the fallout from the tech bubble crash and the Enron accounting scandal. These troubles led to a brief slowdown, but the economy quickly recovered.

The Gulf War (July 1990 to March 1991). The United States experienced an eight-month economic stagnation at the beginning of the 1990s, which could be partly attributed to the spike in oil prices during the First Gulf War.

recession and the business cycle

There is a widely held opinion among financial analysts and many economists that economic slumps are an inevitable part of the business cycle in a capitalist economy.

At least on the surface, it would appear that the empirical evidence strongly supports this theory. In modern economies, it seems there are slumps every decade or so, and, more specifically, they tend to occur naturally after periods of strong growth.

Historically, economic declines have occurred about every three and a half years, on average, since 1857. Once the government felt these declines would fade by themselves, that was the best solution for all concerned.

After World War II, the average time between economic slowdowns was five years. So it took 128 months from the start of the Great Recession to the end of the last economic expansion.

With this in mind, the pandemic hit us at a time when we were long overdue for a retraction.

An economy's business cycle refers to how periods of growth are interspersed with periods of contraction. At the beginning of an economic expansion, the economy experiences healthy, sustainable growth.

In the long run, the following events take place:

- Lenders make borrowing money easier and less costly

- Encouraging consumers and businesses to load up on debt

- Eventually, asset prices will ride on the wave of irrational exuberance

As the economic expansion ages, asset values begin to rise more rapidly, and debt loads become more significant. As a result, the expansion of the economy will be disrupted if, during a certain period of the economic cycle, one of the phenomena listed as the causes of a slump take place.

This shock bursts asset bubbles, crashes the stock market and makes those large debt loads too expensive for people to maintain.

Growth contracts and the economy slows down as a result of this sudden shock.

Indicators of a Recession

The indicators of a recession are illustrated below:

1. Inverted Yield Curves

Inverted yield curves predict economic downturns better than stock markets and leading economic indicators. This is when short-term government securities yield more than ten-year government bonds. Inverse yield curves indicate weak growth.

2. Gross Domestic Product (GDP)

The real GDP of an economy is a measure of how much total value it generates (through goods and services) during a given period, weighted for inflation. Declining real GDP tends to indicate stagnant productivity.

3. Real Income

A real income is determined by measuring income, adjusting it for inflation, and discounting social security measures, such as welfare, to come up with a real income. The purchasing power of an individual is reduced as their real income declines.

4. Manufacturing

Exports, imports, trade deficits, and surpluses with foreign countries, as well as the strength of the manufacturing sector, are factors that determine the strength and self-sufficiency of an economy.

5. Wholesale/Retail

The success of a market for goods is gauged both by measuring wholesale and retail sales and adjusting the inflation figures.

6. Employment

Unemployment is a lagging indicator. Rather than predicting future expansion, it confirms contraction. An unemployment rate of more than 6%, as a percentage of the total workforce, is normally considered problematic.

7. Market Trends

An abrupt change in the macroeconomic environment or a structural shift can trigger a slowdown. According to the Real Business Cycle Theory, a business cycle contraction result from unanticipated or negative market shocks.

For example, rising hostilities in Ukraine affected crude oil-importing economies by rising oil prices. Automating factories in a revolutionary way could have a disproportionate impact on economies with a large pool of unskilled labor.

8. Monetary

Stagnation occurs as a result of overexpansion, according to a school of economics called monetarism. During the early phases of a slowdown, it is exacerbated by an insufficient money supply and credit availability.

Interest rates and relationships between goods are strongly correlated with monetary and real factors. Therefore, in addition to monetary policy instruments like interest rates, institutions also respond to anticipated slowdowns.

Benchmark interest rates may be used to predict the shrinking of the economy. The Treasury yield curve inverted during the 18 months prior to each of the last seven US financial crises. Falling equity values also indicate lower expectations for the future.

9. Psychological factors

An economic expansion causes excessive euphoria and risky capital exposure. For example, the 2008 Global Financial Crisis was caused by irresponsible speculation in the US housing market. Pessimism can also curb investment in the real economy.

Causes of a Recession

Economic slumps are caused by a loss of business and consumer confidence. As confidence recedes, so does demand. It is a tipping point in the business cycle when ongoing economic growth peaks, reverses, and becomes ongoing economic contraction.

There are many causes, ranging from a sudden economic shock to inflation that goes unchecked. Below are some of the main causes:

- Demand outpaces supply in overheated economies, resulting in overcapacity and full employment. Spending will eventually fall to match supply. Overheating consists of rising inflation and unemployment below the "natural" rate.

- Financial damage can result from economic shocks. For example, in the 1970s, OPEC cut off oil supplies to the US without warning, causing an economic collapse and long fuel lines. A recent example of a sudden economic shock is the Coronavirus outbreak.

- When businesses or individuals take on too much debt, they may find that they cannot pay their bills. As a result, defaults and bankruptcies may increase. For example, the housing market collapse in the 2000s was caused by excessive debt.

- Asset bubbles -Investing decisions driven by emotion leads to bad economic outcomes. When the economy is performing well, investors become too optimistic.

In the late 1990s, former FED Chair Alan Greenspan famously called this phenomenon "irrational exuberance." This creates a bubble in the stock or real estate market, and panic selling may cause the market to crash when the bubble pops.

Inflation is an upward trend in prices. Excessive inflation is detrimental. Central banks control inflation by raising interest rates. The United States was plagued by inflation during the 1970s. Thus, interest rates were raised rapidly, causing the economy to tank.

Deflation can be worse than runaway inflation. Deflation occurs when prices decline over time, which causes wages to contract, further lowering prices. If deflationary feedback loops get out of control, people and businesses stop spending, which damages the economy.

To fix deflation, central banks and economists have few tools at their disposal. As a result, the severe decline that Japan experienced during most of the 1990s was caused by deflation.

Technological change. In the long term, innovations are beneficial to productivity and the economy, but adjusting to technological breakthroughs can be difficult in the short term. The 19th century saw waves of labor-saving technological advances.

As a result of the Industrial Revolution, entire professions became obsolete, causing unemployment and hard times. There is a concern today that robots and artificial intelligence may have a similar effect by eliminating entire categories of jobs.

What Happens in a Recession?

Economic decline causes the economy to struggle; people lose their jobs, companies make fewer sales, as well as the overall nation's economic output, decreases. It is difficult to predict when an economy will officially fall into a slump, as so many factors are to consider.

As a result of sluggish production, falling demand for goods, and tightened credit, the economy began to subside. As a result, unemployment, investment losses, and reduced living standards lead to lower living standards.

ETFs and mutual funds are great ways to invest in stocks during periods of stagnation. This is because an investment fund tends to be less volatile than a portfolio of stocks, and investors rely less on single stocks than they do on economic growth and a boost in market sentiment.

Due to falling demand, houses also tend to become cheaper because of falling prices—since more people are worried about making a big move, prices fall to entice those who remain.

During a downswing, the price of food is usually stable. However, if this persists, then its severity can result in a period of deflation (sliding prices across the board). Therefore, it is likely that food prices will drop by a similar amount.

It is common for interest rates to fall early in a downturn and then rise again when the economy begins to recover. In other words, if you take out a loan during the downturn, the adjustable interest rate is more likely to rise once the downturn ends.

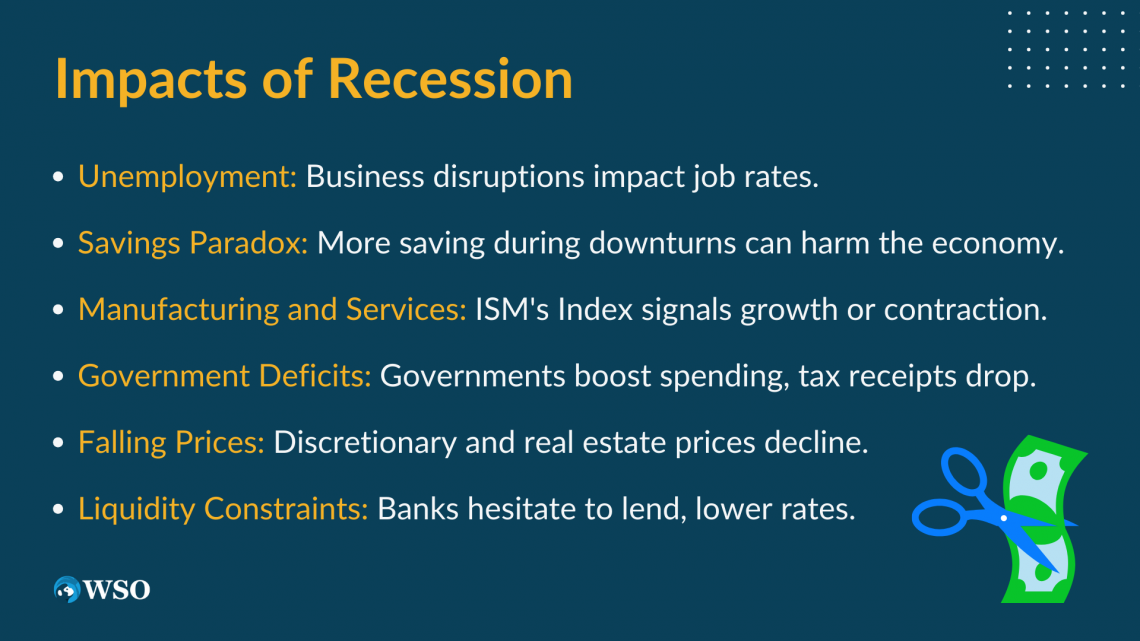

1. Unemployment

Business cutbacks and closures can increase unemployment, but the degree of disruption can vary. For example, the relatively mild slump of 1990–1991 barely exceeded 7.0%, but it rose after the downturn ended.

2. People may save more, but this can backfire

In slowdowns, people who are still employed tend to spend less for fear of being laid off. Unemployed people naturally cut back on their spending. The "paradox of thrift," coined by Keynes, can arise if too many people reduce their spending.

As one person's spending determines another's income, if too many people limit their spending, the result is a downward spiral that results in progressively reduced income and higher unemployment. Individual decisions can harm the economy.

3. Manufacturing and services can decline

From the last recession to our current pandemic-induced decline, the Institute of Supply Management's Purchasing Managers' Index has recorded 131 consecutive months of manufacturing growth. A contraction index of below 50 follows a growth index of over 50.

4. Prices can fall

The prices of discretionary items and real estate can fall during severe slumps. Consumers focus on low-cost necessities. During the 1980s and 1982 recessions, the US Federal Reserve kept interest rates well into the double digits as a way to combat inflation.

5. Liquidity can dry up

In the event of an economic downswing, banks become less inclined to lend because they fear not being repaid. In addition to this, interest rates tend to fall, which causes banks' profit margins to shrink.

6. Deficits can increase

To counteract the effects of the downswing, governments often increase spending. As a result, as well as the decline in corporate and personal income, tax receipts also drop.

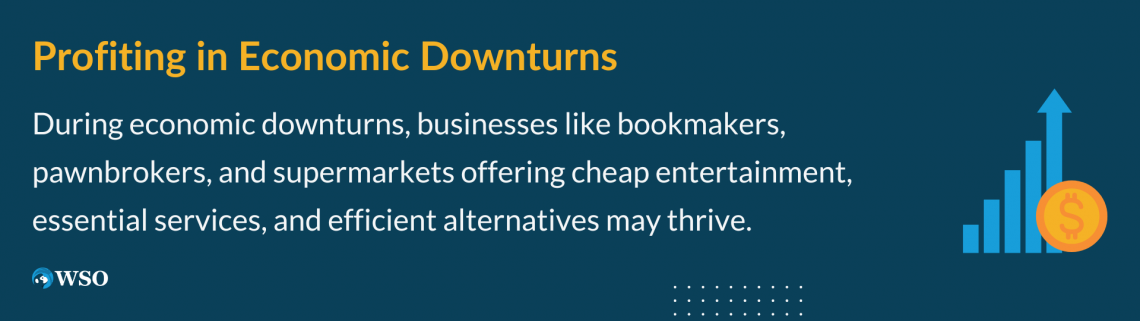

Who benefits from a business cycle contraction?

Some businesses and individuals may still be able to prosper even during a period of a slowdown in economic growth.

Examples of this include:

1. Businesses offering cheap entertainment

Bookmakers and pubs normally do well in a downturn because people like to 'drown their sorrows' with small bets. The demand for online streaming and entertainment will likely have arisen during the 2020 Coronavirus Pandemic.

2. Companies dealing with bankruptcies and loss of income

Pawnbrokers and firms that sell payday loans - people who are short of cash turn to loan sharks to borrow money when they need it.

3. Retailers are selling inferior goods

Supermarkets and second-hand shops won't be adversely affected by the downturn because their goods have a higher demand when income falls, such as valuable goods. Despite cutting back on luxuries, consumers are unlikely to cut back on food.

4. Greater efficiency in the long term

Some economists believe that a slump might boost the economy's productivity in the long run. During a slump, new firms emerge as inefficient firms disappear. When some businesses fail, new innovative firms grow.

Some efficient firms may also be forced out of business due to cash shortages and a temporary drop in income during an economic decline. Not all businesses that go out of business are inefficient. Losing firms also means losing expertise.

In an environment where asset prices are declining, buying a house at a lower price may be possible. This is especially true for first-time homebuyers. This can have a positive impact on reducing wealth disparities.

The Great Depression increased life expectancy in areas where unemployment was high. This may seem counterintuitive, but the unemployed may have more leisure time, which could boost their health. For retirees and people on fixed incomes, lower inflation can be a good thing.

Can you predict a recession?

It is extremely difficult to predict downturns based on economic forecasts. COVID-19, for example, appeared seemingly out of nowhere at the beginning of 2020, and within a few months, the US economy was in ruins. As a result of the pandemic, the US economy contracted.

However, there are still some signs that may indicate that trouble is on the way in the near future. Here are some warning signs that can help you figure out how to be prepared for an economic downturn long before it occurs.

A yield curve that is inverted shows a graph of market values for bonds with different maturities. The market value of long-term bonds is higher during a healthy economy. When long-term yields start to decline, investors become concerned. An inverted yield curve signals the start of a business cycle contraction.

1. Consumer confidence decreased as a result of the economic downturn

A drop in consumer confidence could also indicate trouble ahead for the economy. In the event that consumers decide not to spend money due to their fear of doing so, the economy is likely to slow down.

2. A drop in the Leading Economic Index (LEI)

The LEI aims to predict future economic trends. It considers factors such as unemployment insurance claims, new manufacturing orders, and stock market performance. A decline in the LEI may indicate a downturn in the economy.

3. A sudden decline in the stock market

There is a strong likelihood that a sudden and significant drop in stock markets could indicate an approaching slump because investors sell part of their holdings, and sometimes even all of them, in an attempt to take advantage of an economic slowdown.

The loss of jobs is an obvious sign that the economy will suffer. Even if the National Bureau of Economic Research (NBER) has not declared a recession yet, a few months of steep job losses is a big warning of an impending decline.

The bottom line

Often, declining GDP growth is cited as a cause of a contractionary business cycle, but this is more of a warning. By the time the GDP turns negative, the recession will have already begun. It occurs when GDP decreases for more than two consecutive quarters.

When consumers lose confidence, they stop buying and become defensive. As a result jobs are lost, retail sales fall, and panic ensues.

Manufacturers reduce production when orders fall, leading to an increase in unemployment. Governments often step in to restore confidence.

When interest rates rise, it limits liquidity and the money available to invest or spend. As a result, the Federal Reserve often raises interest rates to maintain the dollar's value. It did so to battle the stagflation of the late 1970s, and this contributed to the 1980 recession.

An abrupt drop in investor confidence can lead to a bear market, depriving businesses of funds. A decline in manufacturing orders is also an indicator of a slump. Orders for durable goods started declining in October 2006, long before the economic crisis of 2008.

If homeowners lose equity and cannot refinance, they are forced to reduce costs. A complex investment based on declining home values ultimately lost money to the banks.

Removing crucial safeguards can also lead to a slump. The 1982 Garn-Saint Germain Depository Institutions Act contributed to the S&L crisis and recessionary phase of the economy. This law removed loan-to-value restrictions on these banks.

Bad business practices often cause slumps. One recent example is the savings and loans crisis of the 1990s. Land flipping, questionable loans, and illegal activities caused more than 1,000 banks with $500 billion worth of assets to fail.

Historically, wage and price controls have only led the economy towards it once. Richard Nixon froze wages and prices in 1971 to stop inflation, but employers could not reduce wages. As incomes fell, so did demand. Companies were unable to lower prices, which led to the 1973 economic crisis.

Researched and authored by Saif Ali | Linkedin

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?