Reverse Morris Trust

Enables a business that wants to spin off and then sell assets to an interested party without paying taxes on any gains from the sale.

What is The Reverse Morris Trust (RMT)

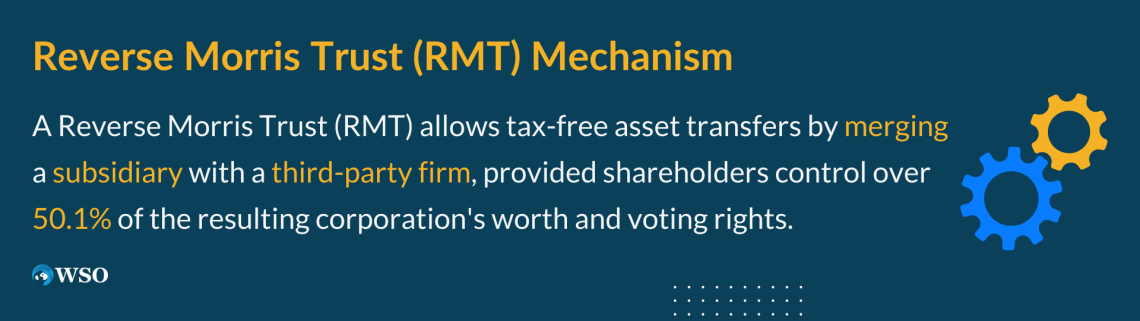

According to American law, a Reverse Morris Trust (RMT) enables a business that wants to spin off and then sell assets to an interested party without having to pay taxes on any gains from the sale. In addition, RMTs are utilized in mergers and acquisitions.

The RMT approach works as follows: a parent business spins off a subsidiary to which it transfers undesired assets.

The subsidiary merges with a third-party firm to form a new, unrelated company; the new company issues at least 50.1% of its voting stock (and consequently control) to the shareholders of the original parent company.

The undesired asset, which the parent business sold tax-free, is now owned by the newly merged entity.

The parent firm can raise money, monetize its stake in the division being a spin-off, and pay down debt through the subsidiary spin-off. As a result, businesses use RMT transactions because they combine the advantages of mergers and products.

For example, it is beneficial when one publicly traded C-corporation wishes to sell an asset worth at least $1 billion to another publicly traded C-corporation.

A parent business can use the Reverse Morris Trust to eliminate all taxes and give the asset to its current shareholders.

Significant synergies can be produced by the spin-off business merging with another operating company, adding value for the parent shareholders. The parent shareholders must own at least 50.1% of the merged company.

The capacity of the merging firm to repurchase shares is usually restricted by a restrictive covenant that is in effect for two years.

Suppose most of the shares are not distributed to shareholders of the original parent company. In that case, the transaction is not an RMT transaction and may therefore be taxable to the parent business and its shareholders.

Key Takeaways

- A Reverse Morris Trust (RMT) is a tax-efficient strategy that allows a business to spin off and sell assets to an interested party without paying taxes on the gains from the sale.

- The RMT process involves spinning off a subsidiary with undesired assets, which then merges with a third-party firm to form a new, unrelated company.

- The parent company's shareholders must own at least 50.1% of the new merged company to maintain the tax-free status.

- RMTs are utilized in mergers and acquisitions to monetize assets, raise funds, and pay down debt while benefiting from tax advantages.

- The RMT structure has certain conditions to be met, and anti-Morris Trust rules were established by Congress to prevent tax-dodging transactions. However, RMTs are not very common due to complexities and limited opportunities for equity and cash consideration post-merger.

Understanding the Reverse Morris Trust (RMT)

If certain conditions are met, a parent corporation may sell a subsidiary tax-free under Internal Revenue Code section 355.

The former subsidiary, which the shareholders of the parent business control but separate from it, merges with a target firm to form a combined entity.

If the former subsidiary is regarded as the target firm's "buyer," the transaction may be largely tax-free under Internal Revenue Code section 368(a)(1)(A).

If the original parent company's and the former subsidiary's shareholders own more than 50% of the combined business, the former subsidiary is the "buyer."

Each structure in the world of mergers and acquisitions is either the product of a legal loophole or is predicated on a court of the land ruling.

For instance, the Morris Trust structures were made possible by the Fourth Circuit of the U.S. Court of Appeals' favorable decision in the 1966 case of Commissioner v. Mary Archer W. Morris Trust.

The distributing corporation ("Distributing") in the case of Commissioner v. Mary Archer W. Morris Trust, 697 F.2d 794 (4th Cor. 1966) was active in the banking and insurance industries.

The insurance company was transferred to a new corporation, and the new organization's shares were spun off to its stockholders. Then, it is merged with another bank for legitimate non-tax commercial reasons.

The court found that because the previous shareholders of Distributing got 54% of the shares of the merged entity, the continuity of stockholder interest criteria was satisfied, making the transfer a nontaxable spin-off.

It was thought that the Morris Trust rule was being utilized to transfer undesired corporate assets without subjecting the transfer to corporate tax because the previous shareholders had no ongoing interest in the business.

Based on this evaluation, people started exploiting the benefits.

The Internal Revenue Service subsequently established section 355(e) for the Reverse Morris Trust in1977, defining several conditions that must be satisfied to qualify for tax advantages.

Every time a 50% interest in a spin-off firm is transferred tax-free two years following a spin-off, this rule levies additional taxation on the distribution made at the spin-off stage.

How a Reverse Morris Trust (RMT) Works

RMTs were first used due to a 1966 decision in a lawsuit against the Internal Revenue Service, which offered a tax loophole for the sale of undesired assets.

A parent business that wants to sell assets to a different company initiates the RMT. The parent business then establishes a subsidiary, and the third-party firm and that subsidiary merge to form an independent corporation.

The unrelated firm then issues the shareholders of the original parent business shares. The RMT is finished if shareholders possess at least 50.1% of the unrelated firm's economic worth and voting rights.

The assets have been legally and tax-free transferred from the parent business to the third-party firm.

After an RMT's establishment, the original parent company's stockholders must control at least 50.1% of the combined or merged company's assets and voting rights to maintain the RMT's tax-free status.

Due to this, the RMT is only appealing to third-party businesses similar in scale to the spun-off subsidiary or more minor.

It's also important to note that, although having a non-controlling interest in the trust, the third-party firm in an RMT has more freedom in selecting its board of directors and top management.

However, it is essential to ensure that all of the requirements outlined in Section 355 are met for at least two years after the merger.

Anti-Morris Trust Rules

Since then, businesses have continued to use this kind of tax-dodging transaction. In 1997, Congress took action to plug the loophole by establishing the so-called "anti-Morris Trust" legislation.

The regulations are listed in Internal Revenue Code Section 355(e) and Treasure Regulations 1.355-7.

According to Section 355(e), also referred to as the anti-Morris Trust rule, a corporation that distributes the stock of a subsidiary to its shareholders in an otherwise tax-free spin-off realizes a taxable gain if 50% or more of the vote or value of either the distributing corporation's stock or stock of the spun subsidiary is acquired as part of a plan that includes the spin-off.

Such an acquisition is regarded by Section 355(e) as "part of a plan" if it occurs two years before or following the spin-off.

However, no such tax will be applied if it can be shown that the acquisition and spin-off were not part of a plan.

The anti-Morris Trust rule implies that the acquirer must be smaller than the target business, resulting in a minority (less than 50%) ownership position in the combined company.However, suppose a potential acquirer is only marginally more significant than the target.

In that case, it might be possible to either increase the value of the target by shifting leverage to the parent before the spin-off or decrease the value of the target by reducing the value of the acquirer through a dividend or share repurchase.

In any instance, before moving forward with a planned Morris Trust transaction, the distributing corporation should get a private letter ruling from the IRS supporting tax-free treatment of the transaction.

Examples of a Reverse Morris Trust (RMT)

A few examples are:

1. Verizon Communications and Fairpoint

In 2007, Verizon Communications announced that it would hand over certain landline operations in the Northeast to FairPoint Communications. Verizon allocated its shares to its current owners and moved undesirable landline business assets to a different subsidiary to qualify for a tax-free transaction.

Then, Verizon and FairPoint completed an RMT reorganization, giving the original Verizon shareholders a majority interest in the combined corporation and giving the FairPoint management team the go-ahead to govern the newly created company.

2. Lockheed Martin and Leidos Holdings

Another illustration is the 2016 exit of Lockheed Martin from its Information Systems & Global Solutions (ISGS) business division.

Like Verizon, it underwent an RMT by creating a new branch business that later merged with Leidos Holdings, a company specializing in defense and information technology.

Leidos Holdings made a cash payment of $1.8 billion, while Lockheed Martin reduced the number of its outstanding common shares by about 3%.

At the time of the deal, Leidos was held by 50.5% of the Lockheed Martin investors concerned. The transaction's estimated total value was $4.6 billion.

Entercom announced the acquisition of CBS Radio on February 2, 2017. A Reverse Morris Trust was used to carry out the sale to make it tax-free.

Rules for a tax Advantage under the Reverse Morris Trust (RMT)

To be qualified for tax advantages under the Reverse Morris Trust structure, Section 355 requirements must be satisfied.

These requirements are:

- The original parent business's ownership stake in the newly combined company must continue to be 50% after the merger. Usually, this rule is in effect for at least two years.

- Following the merger, the corporation cannot sell equity. It should stay within 50% of the threshold limit if sold.

- The debt-to-debt or debt-to-equity swap ratios can be calculated. However, it must still fall under the stated limitation of 50% ownership.

- Before implementing the RMT structure, parent and subsidiary enterprises must have five years of continuous active trade or operation history.

- The newly merged company must continue operating for a predetermined time after the merger.

- The parent firm must own at least 80% of the subsidiary's assets that it wants to sell.

- For the relative values to a function, SpinCo (the spin-off subsidiary) needs to be larger than the merger partner.

- Like an IPO, SpinCo must present two years of audited financials.

- A legitimate business purpose must underpin the transaction (as opposed to distributing earnings).

Advantages and Disadvantages of Reverse Morris Trust (RMT)

The advantages of RMT are as follows:

1. Avoids Corporate Taxes on Gains

The main benefit of the Reverse Morris Trust structure is that it makes it possible to implement tax planning strategies within the framework of the applicable laws.

2. Silent Asset Movement

Immediately following the sale of the shares to the shareholders, the assets will be spun off. It will make it possible for assets to move freely since no further clearances are required.

The same management, staff, labor, and resources will be used together with the same company philosophy. It won't affect the company's regular operations in any way. It is therefore seen as a silent transfer of subsidiaries.

3. The Net Book Value of the Transmission Assets Remains the Same for the Former and the New Owner

In the RMT arrangement, the company must transfer all the assets to the third company at the book value. Therefore, it doesn't lead to a pointless rise in the assets' overvaluation.

4. Acquirer's Stock Is the Consideration Paid

The buyer can pay in equity shares, which makes this arrangement particularly appealing to businesses.

The disadvantages of Reverse Morris Trust (RMT) are as follows:

1. Limited Opportunity for Equity Issue Post-Merger

After the merger, the parent company, as the original shareholder, must retain a 51% ownership stake. Therefore, it does not allow for post-merger share issues.

2. Limited Capacity for Cash Consideration

Due to the need to maintain the equity requirement, consideration will be limited to equity. Consequently, there is a limited range for the issuance of care in money.

Why isn't Reverse Morris Trust (RMT) More Common?

Only a small number of RMTs occur annually. On the other hand, numerous traditional spin-offs are announced.

This is partially due to the rules that apply to reverse Morris trusts: only specific businesses may use them and must have earned positive income in the five years preceding the transaction.

Morris Trusts are not frequently used because it is difficult to identify a strategic buyer smaller than the target but not so small as to make the transaction impractical.

Suppose a prospective buyer is too tiny to carry out a Morris Trust deal alone. In that case, it might think about teaming up with a financial sponsor to fund the acquisition (such as a private equity investor), but this adds another complication to an already complex transaction.

The make-up of the board of directors and management team of the combined business could prove to be a sticking point in talks between the purchaser and seller.

Since it is technically the buyer, the acquirer wants to keep its management team intact and desires a majority of board seats.

But from the standpoint of the seller and/or the target, the acquirer is a minor player in the merged company with limited power to decide who will be on the board of directors or the management team.

A Morris Trust deal also signifies a significant transformation in the corporate structure of the buyer.

A potential buyer's management team and/or shareholders may have severe doubts about pursuing such a sizable (relative to the buyer's size) transaction, especially when there is uncertainty surrounding the anticipated synergies.

This is true even if the deal is anticipated to be accretive to the buyer's shareholders.

Reverse Morris Trust (RMT) FAQs

A firm may decide on a reverse Morris trust to concentrate on its main business and sell assets tax-efficiently. This enables the parent firm to raise funds and aid in debt reduction while selling unwanted corporate assets.

High-debt corporations may benefit from this kind of transaction.

In contrast to a reverse Morris trust, a Morris trust involves the parent firm merging with the target company rather than creating a subsidiary.

or Want to Sign up with your social account?