Pre-Offer Defense Mechanism

A group of defensive strategies applied in a hostile takeover

What is a Pre-offer Defense Mechanism

"Pre-offer defense mechanism" is a group of defensive strategies applied in a hostile takeover. A firm undertakes the pre-offer defense mechanisms to protect itself from a possible acquirer in a hostile takeover.

Pre-offer defense attempts reduce the likelihood that a hostile takeover would succeed by making the target firm less attractive to a company and less likely to prosper.

These measures can include placing specific corporate governance controls to bind a threatening bidder's ability to vote and make choices.

The defense methods are formed or put in place far before any actual takeover effect, rather than an urgent response to a takeover bid.

Some defense methods may or may not be successful in each nation due to various limits related to a different legal system. Thus, adopting these takeover defenses is also conditional on a firm's geographical scope of operations.

- On an independent level, we may infer that dual-class capitalization and an effective staggered board are the best preventive defensive methods, followed by a poison pill, in terms of efficacy, simplicity of adoption, range, and effects on shareholder wealth.

- Other defense techniques, while successful, contain flaws and weaknesses that allow them to be exploited or, in some situations, have a significant negative influence on shareholders' wealth.

- To fight against a takeover attempt, management employs a variety of techniques. Using a suitable defense mechanism for the company's circumstances is critical.

- Pre-offer acquisition defenses, such as poison pills, poison puts, staggered boards, restricted voting rights, supermajority voting provisions, blowfish, dual-class stocks, and golden parachutes, are more probable to be supported in judicial rulings than post-offer defenses.

Types of Pre-offer Defense Mechanisms

When a firm is seized without the leadership's approval, it is called a hostile takeover. In a conventional takeover, the boards of directors of the target firm would approve the agreement reached by the two businesses.

A bidder has two primary options for an effective acquisition when the target firm's board members object: it can either focus on other stockholders in a proxy battle or the board members directly in a tender offer.

The possibility that the bidder will successfully seize the target's leadership, that is, gaining possession of 50.1% or more of the target shares, makes such hostile takeover attempts attractive.

The important aspects that will probably have the biggest impact on whether a hostile takeover attempt is successful are the target board's first and ultimate recommendations if the bidder raises its original offer and if the target's majority investors are prepared to approve the proposal.

Pre-offer defensive actions are generally classified into many types based on the methods used to reduce the likelihood of an effective hostile takeover. Among these protective systems are:

Poison Pills

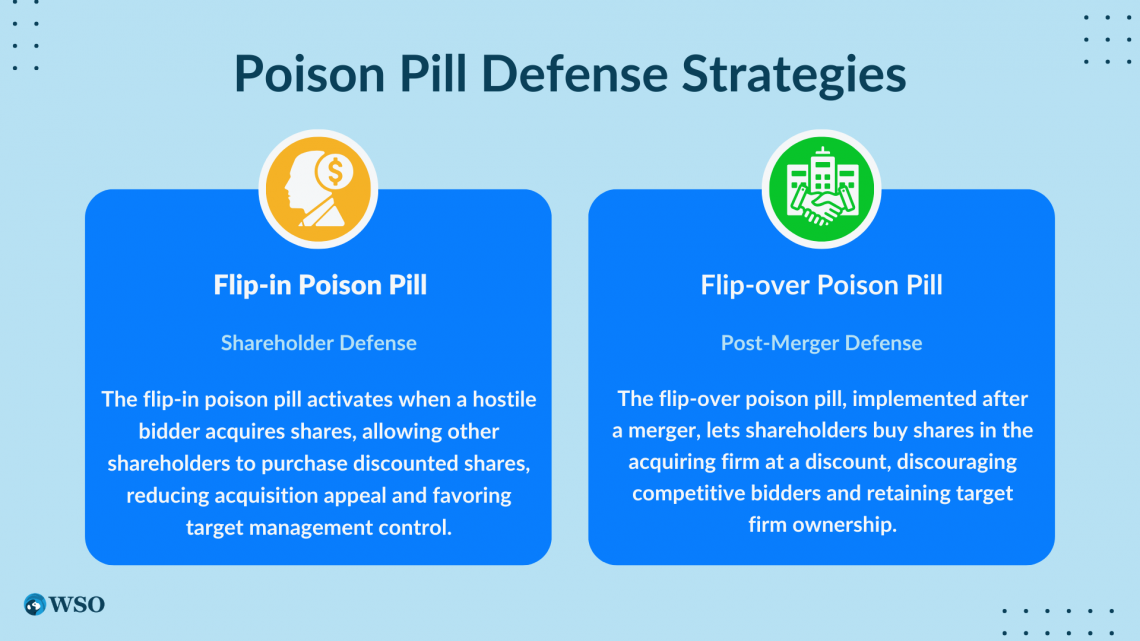

One of the more popular defense methods is the poison pill approach, commonly known as the shareholder rights plan.

The method's basic aim is to dilute the firm's shares and focus control among current shareholders to make it harder for a potential buyer to assume ownership of a firm in an acquisition.

For example, in 2012, Netflix Inc. employed a poison pill to prevent Carl Icahn from launching a hostile takeover bid. Netflix instantly went on the defensive after discovering that Icahn had purchased a 10% ownership in the firm.

Any effort to purchase a big ownership position in Netflix without board approval would end in a rush of new shares, making any investment acquisition too costly.

A poison pill technique is divided into two subgroups:

1. Flip-in Poison Pill

When a hostile bidder gets a particular portion of the shares, the flip-in poison pill ignites and grants all shareholders, excluding the hostile bidder, the option to buy more shares at a discounted price.

This dilutes the shares, making the acquisition less tempting. As a result, target firm control is reallocated in favor of the target management and board.

2. Flip-over Poison Pill

This occurs following a merger and permits shareholders to acquire interests in the acquiring firm at a reduced price. This dissuades competitive bidders who may be worried about the valuation of their firms.

Following the hostile takeover, such methods ensure that the target firm owns a considerable portion of the newly combined firm.

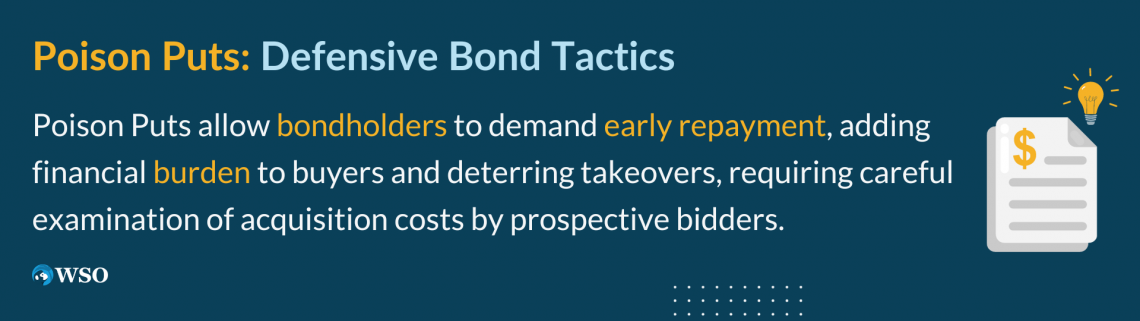

Poison Puts

Poison Puts enables current bondholders of the target firm to request prompt settlement of their loan. Unfortunately, this is done to place an added financial load on the buyer, perhaps leaving the deal worthless.

Likewise, the target firm offers bonds to shareholders that can be repaid at a discount before their expiration. However, it should be noted that the bonds can only be honored before expiration if a hostile takeover bid is submitted.

Suppose a target firm uses the poison put defense tactic. In that case, a prospective bidder should closely examine the cost of acquiring a majority position in the target company and any related expenses, such as the target's debt obligations, and verify that it has adequate money to meet all acquisition costs.

Although this form of takeover defense is lawful, business leaders must still act in the best interests of the shareholders.

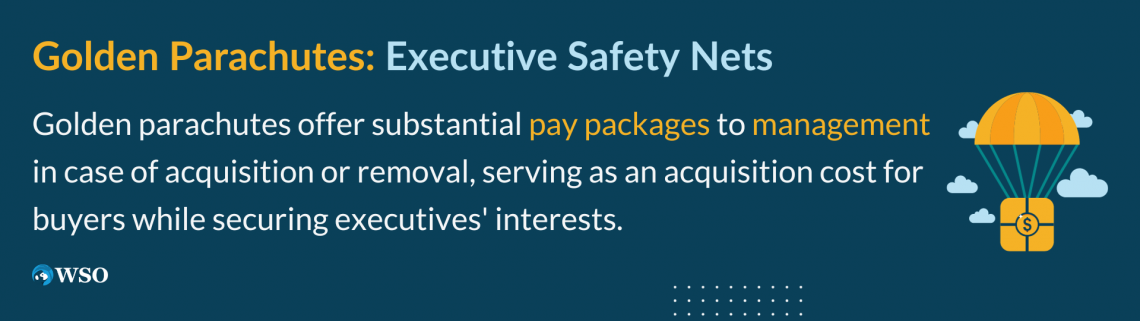

Golden Parachutes

The golden parachute is a contingency, or additional pay, offered to management if the firm is bought by another company and/or if the acquirer forcefully removes or releases the management from their roles.

It creates a significant provision for management pay, whether cash, shares, or both. As a result, it functions as a costly provision for the acquirer, who must bear these expenses.

The acquiring company may not consider the golden parachute approach to be very useful, given that they have to pay a higher price to buy the firm, and thus are prepared to spend a little extra on the outgoing management team for the payout package, as they can then introduce their managerial group to best meet their goals.

Meg Whitman, CEO of Hewlett-Packard Enterprise, stood to gain over $91 million if the firm was bought under her leadership. She was also guaranteed more than $51 million in severance pay if fired. After the corporation was downsized, she earned $35.6 million.

In 2016, Dell teamed with storage titan EMC. As a result, EMC's CEO got $27 million in pay under the conditions of his golden parachute.

Supermajority Provisions

A supermajority provision is a corporate charter modification that needs a sizable majority of shareholders (usually 67 percent to 90 percent) to allow significant changes such as mergers and acquisitions.

A condition can be added, needing a majority of greater than 51 percent to support a takeover. For instance, if a rule is included asking at least 75 percent of the votes to be in support of the purchase for it to proceed, a shareholder with just a 26 percent holding can also oppose the takeover.

At a general meeting of shareholders, a supermajority of votes is counted. Based on the type and importance of the topic being voted on, this can be a yearly meeting or a non-regular gathering held during the year.

When passed, a supermajority vote can be helpful, but the reverse can also be true. For example, a supermajority vote might result in a standstill in which no decision is taken, which can harm the entity.

Staggered Board of Directors

This is one of the most popular pre-defensive tactics put into a company's corporate charter to avoid a hostile takeover effort or to react in the most acceptable way possible.

The central concept behind a staggered board system is to prevent the entire board from being changed simultaneously.

For example, certain members are selected for a time that finishes in a year that differs from the term completion of the other board members.

As a result, an acquiring company cannot change or convince all board members to seek total power over the target. As a result, the purchaser must wait or continue to pursue the target for two or more years in a row to gain a majority on the board.

As there aren't many highly driven entities ready to chase the target for several years in a row to take possession of the firm, this method prevents hostile attacks.

Blowfish

One of the defensive mechanisms companies use involves a plan in which the business concentrates on purchasing new assets to build its asset base, pushing the business towards a growth emphasis and lowering the firm's liquid asset base and possible extra cash on hand.

This acquisition-led growth method raises company value.

The main idea behind this defense method is that the greater (higher) company value can frighten the bidder from trying to pursue their path of acquisition because the improved (higher) company value would result in a greater price and, thus premium to be charged in the course of acquisition.

As a result, a buyer with limited funds available is constrained in completing the deal. Furthermore, the lower liquidity of the resources aids in resisting the buyer by reducing the desirability of the target firm.

Dual Class Stock

The primary principle behind the dual-class stock defense mechanism is that a company can issue two types of stocks in the market—those with considerable voting rights and those without.

Dual-class stock is frequently classified as Class A and Class B, with Class B usually, though not necessarily, having more powerful voting power. Both forms of shares are ordinary shares.

Dual class stock is intended to provide certain stockholders with voting power. Classes of stocks with uneven voting power may be issued to please investors who do not wish to give up ownership but would like the public equities market to offer to fund.

Thus, the management or the board of directors can keep a majority of these voting rights shares while freely floating the stocks without the floating rights to investors. As a result, management and the board of directors may establish strong control over the firm.

Researched and Authored by Raghav Dharmarajan

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?