Value investors come in two types, the ones who will look at financials, and the ones who won't. If banking is your forte I would encourage you to read the paragraph on my approach then come back for my next post. If banking is intimidating or difficult to understand hopefully this post will be educational and break bank investing down into easy to understand pieces. The bank I use as an example is not a good investment, but I'll cover why. I think readers will understand how to analyze a bank better by understanding what's bad about banks instead of showing a perfect banking investment. If anyone thinks I'm long winded something to consider; this post is based off a presentation I gave to my company and I covered this material in under four minutes, I can condense when I need to.

Approach

My approach to bank investing is very similar to my approach to buying any other cheap stock. I prefer to buy banks at 2/3 of tangible book value and sell when they approach 1x tangible book value. There are many banks trading at or above tangible book value, and a bank that's profitable should be trading above it, yet many don't. A lot of stocks trade below TBV due to management mis-deeds, or the inability of a company to earn their cost of capital. I believe the reason for bank cheapness now is different, we just went through a banking crisis and banks are still considered toxic investments. Beyond this the market has lost interest in smaller community banks conduct the boring business of gathering assets and re-loaning the money. Many of these community banks emerged from the crisis unscathed, and in a lot of cases overcapitalized and trading at incredibly low valuations. Unfortunately market psychology doesn't care much about this, the banks are still considered risky.

Banking basics

Banking is the ultimate commodity business, and at the same time the ultimate niche/moat business as well. At the most basic level banks are all the same, they take in deposits and loan against those deposits making a spread. Banks have the ability to work at the edges, but the fundamental business is the exact same for a bank in Peoria Illinois as it is for a bank in Sevilla Spain.

Banks are very simple, they gather money in the form of deposits then they loan that money back to those same people and collect interest on the loans. Bank financial statements are a bit strange to look at because we think in terms of ourselves most often. A person's asset might be cash, which deposited at a bank is a liability. A liability to a person such as an auto loan is an asset to a bank. The assets and liabilities are flipped from what you are used to seeing on a normal financial statement. The good news is you only need to learn this once, all banks report in the same manner.

One thing that's interesting about banking is how sticky customers are. For how commodity the bank industry is many banks have what might be considered a moat. Bank switching costs are high, it's very difficult to open and close an account, and most customers don't consider it worth the hassle. I opened an account at a bank a few months back and took my son with me thinking it would be a quick errand. He's three years old, I could count the time it took to open the account by the number of Dum-Dums he ate while waiting, hint his mother will never know the true tally. I think from start to finish it was about 45 minutes, that time alone is an impediment for customers to switch accounts, not to mention having to switch billpay and auto-draft numbers.

Introducing Atlantic Bancshares

The bank in this example is Atlantic Bancshares (ATBA), which is a tiny bank located in South Carolina. The bank has some issues with bad loans which you'll see in a few minutes, but the valuation is attractive. The bank has equity of $7.2m and is currently trading with a market value of $1.4m, or 19% of book value. The bank publishes their annual reports on their website, with the most recent update from the summer. I'm going to use last year's annual report for this example, it's a little outdated, but it doesn't matter much, the principles are universal.

The balance sheet

Assets

Here is the bank's balance sheet as it appears in the annual report:

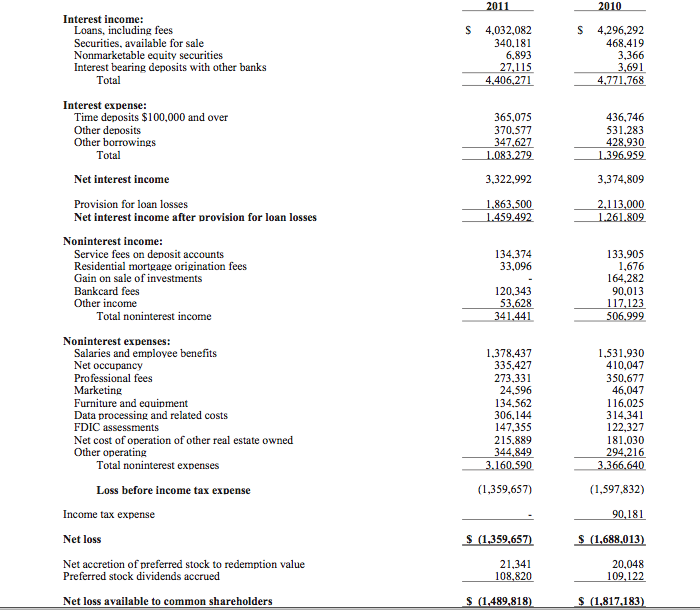

Here is the bank's income statement:

Compared to the balance sheet a bank's income statement is very straightforward. Expenses are itemized at a detail level that's unusual for a non-financial company. What I like about the income statement is it clearly shows the drivers for a bank's profitability. A few quick calculations can be made, take the interest from loans and divide it by the loans outstanding and you can see the interest rate on the bank's loans. Take interest expense and divide it by deposits to see what the bank's paying on deposits.

Most of a bank's profitability hinges on two components, their expense management, and their interest margin. If the net interest margin is too small because they have a high cost funding base they will struggle to maintain profitability. Likewise if the bank's expenses are out of control there will be no profit left for shareholders.

Concluding thoughts

Astute readers will note I left out two things, a discussion of loan losses, and any discussion of a cash flow statement. The cash flow statement isn't as useful when analyzing banks as it when analyzing a non-financial. In a non-financial cash flows can be used to ferret out fraud, for banks other measures need to be used. Banking fraud does happen, but it requires a bit more ingenuity because banks are so highly regulated. The biggest risk to a bank investment isn't fraud but stupidity. If a bank gets lazy and starts writing loose loans they will sink from lax lending standards quicker than anything else.

The second point is much more important, the banks loan losses and trend of losses is vital in determining the safety of an investment. If the bank has too many non-performing loans they will either fail or be required to raise capital. The level of NPA's is important, but the trend is just as important. I didn't touch on this in too much detail because this isn't a comprehensive banking guide, different investors have different NPA preferences, I prefer lower and safer amounts, but some people do well riding momentum as losses start to moderate.

I hope this post has been helpful in explaining bank investing at an entry level. There are a variety of resources to learn about each aspect of banking at a deeper level, but there is no substitute for practice. The best way to learn how to value banks is to get out there and start valuing.

Damn. SB

Stuff like this should be front paged.

Excellent write up.

More like this.

Such a great post! Thanks for this

Wonderful post! Maybe one day you can bestiw upon the WSO community a write up about analyzing a non-financial company. Great work and thank you!

Great post! Do you have any links to more detailed resources?

I will get out there and start valuing! Thanks for the informative post.

Great write up, thanks for the post.

you sir just took my SB away.

Write more and how do i subscribe to you?

Glad you enjoyed the post, I write a few times a week on my blog: http://www.oddballstocks.com

Awesome! I follow the OP's posts on his blog. Pretty good stuff

Concur with above. SB.

Very informative. Thank you for this.

Excellent write up.

Great stuff! Current employer is shifting me to working more with financial companies and banks, so any resource on this is awesome. Very happy to be able to compare my thought process and analyses with yours. Thanks

Most banks these days are trading off of tangible book.

For bank valuation: P/E x ROTCE = P/TBV. P/E reflects that company's growth. ROTCE (Return on Tangible Common Equity) measures profitability.

Can you do a structured finance primer?

Bought JPM on Thursday. P/E level is attractive.

Et vel ut distinctio est. Rerum quaerat qui ut libero soluta.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...