Director

Industry Detail

Private Equity

Group/Division/Type

Infrastructure

City

London

Year

2019

Status

Regular Full Time

Average Hours Per Week

60-70 hours

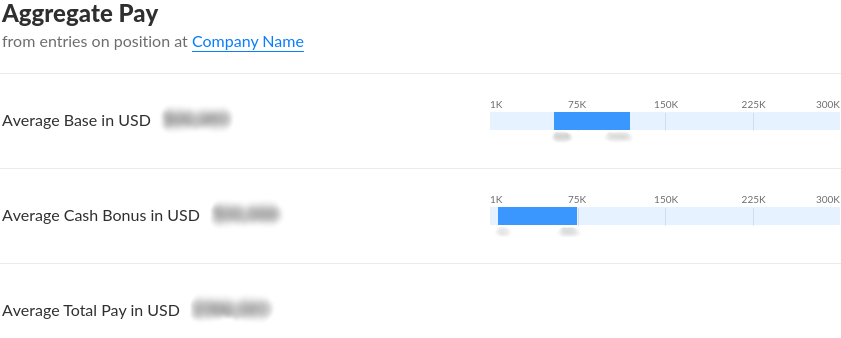

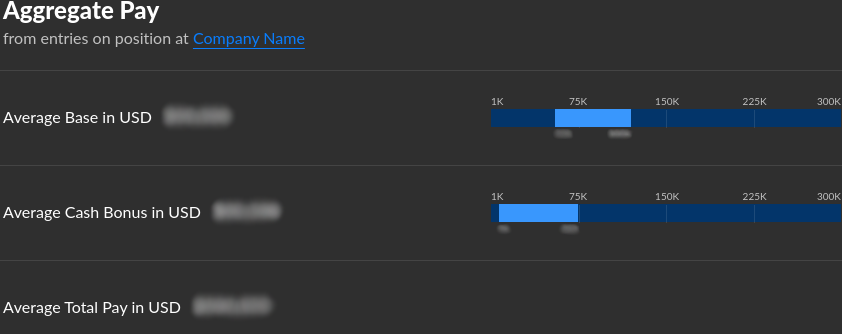

Compensation

Annual Salary in USD

Cash Bonus in USD

Total Pay in USD

Benefits

Health Benefits

Medical / Health

Retirement Benefits

None

Stock Bonus

$0

Profit Sharing

$0

Commission

$0

Relocation Bonus

$0

Sign On Bonus

$0

Weeks of Vacation

5

Want Access to these Alinda Capital Partners Aggregate Pay?

- Free 1 month access by adding just 1 salary datapoint here

- REAL salary bonus data across 1,000+ companies

- Plus free 1 month access to 10,000+ interview insights

Was this review helpful?

How many stars would you give to this salary insight?

or Want to Sign up with your social account?