Investment Banking vs. Capital Markets - How different are they?

How different are they exactly? I know in IBD you work like a dog and you're in the office from anywhere between 80-140 hours/wk, and traders do about 50-60, but how much do capital markets ppl do? Do they work similar hours to IBD? Any difference in compensation? I still don't get what capital markets guys do. Monkey Business describes them as "the illegitimate bastard child between a banker and a trader" but what the hell does that mean? Do they like sit there and just say "the markets are good" or something like that? How are the exit opps (esp into top PE firms/top bschools)? Just curious.

Thanks!

Capital Markets Job Description

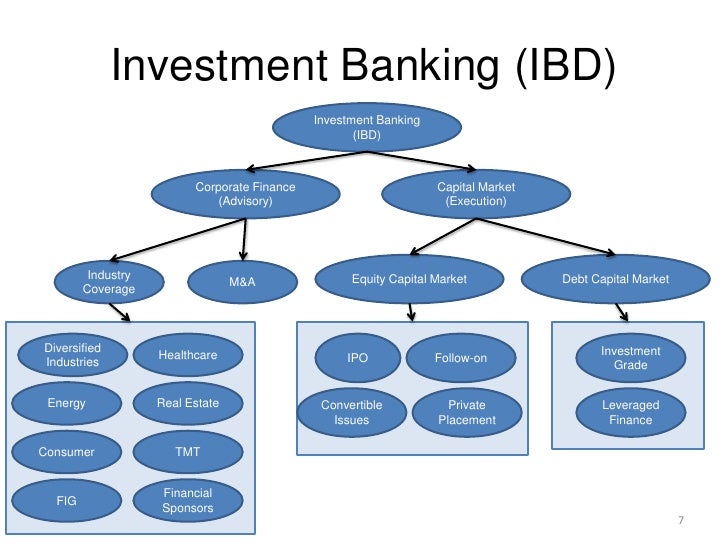

Investment banking and capital markets go hand in hand. Each plays a role in the advisory and capital raising function of "investment banking."

Coverage / sector banking / corporate finance focus on a particular industry (TMT, Healthcare, etc).

Capital markets generally consists of equity capital markets, debt capital markets, and leveraged finance. These bankers focus on their respective products and know the markets for these products inside and out.

Source: https://www.slideshare.net/Human_WSO/unofficial-g…

@ke18sb" says:

The investment banking division makes the product (the model) and the deck. Equity Capital Markets sells the product to investors (the syndicate).

@darthtony" explains that:

At Citigroup, Capital Markets Structuring & Originiation is one of the major groups within the Corporate and Investment Bank. It has two parts, Equity Capital Market (ECM) and Fixed Income Capital Markets (FICM). ECM bankers work very closely with IBD and play a major role in pricing the securities. FICM is consisted of many product groups such as Global Structured Credit Derivatives, Global Structured Credit Products (US CDOs), Domestic Liabilities Management, Financial Institutions, Asset-backed Finance Group, Global structured Solutions, Corporate Derivatives Solutions Group, and so forth.

@TireKicker" says:

ECM is the Chinese Wall (insofar as equity offerings are concerned--just to use that as an example). ECM is the liaison between the industry group (coverage group) and the sales and trading desk. When you are pitching equity to a client, ECM will often accompany the industry group bankers on the roadshow, and their role is to comment on the state of the markets, how receptive investors will be to the company's story, likely pricing (although 95% of the valuation is done by the industry group), etc. It is "investment banking," but not in the sense that most people understand IB. ECM isn’t doing valuation work, models, huge pitch books, etc. They may contribute a few generic pages to a larger pitch done by somebody else.

What do people in capital markets do?

User "JustAnotherBanker" explains that:

"Desirable" work includes being constantly aware of the equity markets (if that's your thing), and there is limited pitch work.

"Undesirable" work includes being called upon frequently to create detailed trading-related reports for sector bankers (e.g. detailed ownership breakdowns and calculations of major shareholders' cost basis).

Capital Markets in the IPO Lifecycle

User "JustAnotherBanker" describes the stage division between the coverage team and the ECM team in an IPO process.

- Source the deal (coverage): Find client. Convince client that an IPO (by your bank) is a good idea. Involves pitchbooks, golf, and booze.

- Take the deal to committee (coverage): Make sure your bank is willing to take the risk (underwriting is risky).

- Negotiate fees (coverage): Set an underwriting/bookrunning fee (~7%). Set the "economics" (the fraction of fees paid to each bank on the deal), haggle over how expenses will be shared, and set provisions such as the Green Shoe (an over-allotment option that helps the underwriter to stabilize the stock price following the IPO).

- Set a target valuation and range (coverage): Come up with a valuation using dcf, benchmarking, and public peers. The client wants a high range, the bank wants a low range.

- Refine roadshow presentation (coverage and ECM): Help management put forth the best possible pitch to institutional investors. Involves re-tooling powerpoint presentations and coaching management.

- Create prospectus (coverage and lawyers): Write up a huge document about the business, its management, its market, the risks involved, and a million other things.

- Due diligence (coverage and lawyers): Make sure the company is legit. Make sure those "factories in Taiwan" actually exist.

- Create internal offering memoranda (coverage or ECM): Turn the information in the prospectus (if there's extra, don't let the SEC find out) into the banking equivalent of Cliff Notes for the sales/salestraders in S&T so that they can stabilize the offering when it finally hits the market (days/weeks later).

- Roadshow (coverage and ECM): Fly around for two weeks with the client, making the same presentation 3 times per day to various institutional investors. Sector bankers prep the client for tough questions and occasionally answer the really ridiculous ones. Sector bankers schmooze the investors and introduce the client. ECM (someone at the VP+ level) provides frequent market updates. ECM "builds the book" -- they take orders from the investors.

- Pricing (ECM): The team in syndicate (a cap markets function) arrives at a final price for the IPO shares based on the order book.

Capital Markets Worklife

@InvestorMA" says:

I know someone in ECM, and he works 6 days a week routinely, often till 12. A really busy week would be 80+ hours. He does no valuation work except in the macro view.

@MonkeyBusiness" explained that:

Supposedly you're supposed to be in by 7AM and accounted for no later than 7:30AM in capital markets so said all my interviewers. Than the higher the rank, the earlier you leave. Usually around 7-8PM on good days. Bad days you can be like the IBD bankers.

Similarly, user "JustAnotherBanker" cited:

Hours are typically shorter than in coverage groups but days usually begin earlier (~8am in ECM vs. ~9-9:30 in sector).

Capital Markets Exit Opporunties

When comparing Investment Banking and Capital Markets, the exit opportunities do not compare. Capital markets backgrounds are not as attractive to the traditional exit opp recruiters (PE, HF).

@rat4100" explains that:

Aside from leveraged finance, stay away from ECM/DCM for the purposes of exit opportunities.”

@1styearBanker" commented saying:

I work at a bulge bracket (BAML, UBS, CS) and I know quite a few capital markets people. In my view, capital markets has 0 exit ops.

Summary

In a detailed response @Monkey_Island" explains:

At its most basic level, the difference between capital markets and "investment banking (coverage)" is this:In general, it's pretty difficult for any banker to know everything about everything. To make things simpler and to really provide good insight regarding industries and products that most people won't have, investment banks utilize the services of different types of "experts." Some of these "experts" will focus on learning and covering the healthcare or software or whatever industry, while others will focus on learning and covering the convertibles market, the equities market, or the high yield bond market. Thus, just as you have "specialists" for different industries, you have "specialists" for different products. How this all ties together is a function of individual banks. at some banks, product experts merely contribute pages regarding the market for the product, potential pricing for the product/product comps, and the capital raising process/procedure as it pertains to that product in order to assist the investment banker/relationship manager with execution. At other banks, the relationship manager will simply hand off the execution process entirely to the DCM/ECM banker since that banker is the "expert" on the process and the product. At the end of the days, all of these people are doctors just as ALL ECM/DCM people are bankers. Any analyst who's ever been to a pitch where different products are being put on the table or where different capital raising ideas are being presented will realize that ECM/DCM is front-office advisory position. You may not being advising on pure M&A, but you are providing advice on financing alternatives since most acquisitions are not financed 100% with cash on hand. Thus, in case of a product such as loans or bonds, industry guys would work with DCM to structure the appropriate loan/bond package, which would then be parceled off to the trading floor where institutional sales guys would find suitable investors. Traders would then come in to play by managing liquidity on the secondary market on behalf of clients who wanted to either a) get some of their purchased securities off their books or b) buy in or buy more.

- Capital markets is focused on PRODUCT knowledge.

- Investment banking is focused on INDUSTRY knowledge.

Want to ace your investment banking or capital markets interview?

Check out WSO's investment banking interview course for access to 10+ hours of videos, 203+ technical questions and over 127 detailed behavioral questions and answers.

.

"the illegitimate bastard child between a banker and a trader".

kinda makes you wonder if ECM guys do trader hours but earn banker dough innit.

the ibd makes the product, ie model, deck, prosperous; ecm sells the product, ie gets the investors to put money in

.

140 hours per week? I didn't know Auschwitz had an investment bank....over the line? Yes I'm sorry, had to throw it out there and yes I am Jewish.

Well obviously IBD analysts VERY RARELY work 140 hours...it's just an extremely high end of the range just like 80 is a low end of the range.

Auschwitz Securities LLC. LOL

80 is def not low end thats average, speaking from my experience as well as my friends

At Citigroup, Capital Markets Structuring & Originiation is one of the major groups within the Corporate and Investment Bank. It has two parts, Equity Capital Market (ECM) and Fixed Income Capital Markets (FICM). ECM bankers work very closely with IBD and play a major role in pricing the securities. FICM is consisted of many product groups such as Global Structured Credit Derivatives, Global Structured Credit Products (US CDOs), Domestic Liabilities Management, Financial Institutions, Asset-backed Finance Group, Global structured Solutions, Corporate Derivatives Solutions Group, and so forth.

You guys ever heard of the "Chinese Wall?"

ECM is the Chinese Wall (insofar as equity offerings are concerned--just to use that as an example). ECM is the liason between the industry group (whomever within Corp Fin) and the sales/trading desk. When you are pitching equity to a client, ECM will often accompany the industry group bankers, and their role is to comment on the state of the markets, how receptive investors will be to the company's story, likely pricing (although 95% of the valuation is done by the industry group), etc.

It is "investment banking," but not in the sense that most people understand IB. ECM guys aren't doing valuation work, models, huge pitch books, etc. They may contribute a few generic pages to a larger pitch done by somebody else.

So essentially, the Monkey Business idea is correct...

This statement above makes me wonder what traditional IB is. Go back 50years ago, wasn't traditional investment banking more concerned with capital raisings than M&A which only came into its own since the 1980s...

Monkeyisland, great post. It will definately shut some misinformed people up...

ECM/DCM is jack-you-off middle office. What the fuck is going on here? It is not in IBD. It is a liason between the markets and the IBD. They are not bankers. They do not advise corporations or underwrite securities.

No "group" within a bank underwrites securities. The bank itself underwrites securities.

industry groups are responsible for underwriting D or E

Semantics.

Well, leveraged finance falls within DCM/FICM in some banks and that's a great area to be in (very interesting work, great exit opps). But otherwise, I'd stay away from DCM/ECM.

One thing to note, though, is that project finance generally falls within DCM, and that is interesting/challenging work.

stay away from DCM/ECM in the structural sense. fuckin dcm/ecm IN the IBD is a good way to go, from what i fucking hear at least. ipos and debt offerings... good shit.

Fuck off Dan, everyone here knows that you're a college kid who's never even seen the inside of an investment bank.

Fuck you douche bag. i know more than you know. Who would the OP rather listen to? A Yale student or just another fuck with a tire as his picture. Fuck off.

You think that the OP would listen to a college kid who poses as an investment banker on an online message board? Yeah, you've got a real lot of credibility. You're a joke and are far worse than aspiringmonkey.

Also, i never said or implied that the OP would want to listen to me, because like you, i'm still in uni (though i am interning at Goldman this summer).

No you're not. Goldman SAs aren't even picked yet. fucker.

sure you go to yale, but you must be a dork with thick glasses, and have nothing else in life to look forward to other than banking and prestige you have ......all kidding aside, enjoy your last year of college, go out, drink lot, meet girls, wahtever.....do the things that you won't be able to do once you start banking

There is a world outside the US, genius.

Why would i lie? I'd have to be a complete loser to pretend i'm something that i'm not on an internet forum...

Who the fuck posts a tire picture on an ib board?

You're too unintelligent to think of a comeback so you come up with this? Wow, i always knew that you weren't the sharpest tool in the shed but this is utterly pathetic.

Anyway, if you aren't able to recognise that rim, you obviously know very little about cars (then again, i'd be an idiot to expect any different from a geek like yourself).

I know someone in ECM, and he works 6 days a week routinely, often till 12. A really busy week would be 80+ hours. Pay is fairly decent. Over 100k this year total comp. About 30k-80k bonus range this year. 65k base. No valuation work, except in the macro view. This is a top-tier BB company though, I have no idea about MMs.

I can't believe a perfectly good and informative thread got de-railed to this extent...

Moving on...Capital Markets does tend to pay the same or 10% less than corporate finance with DCM usually having slightly better pay over ECM.

Is there a link to rankings (2000-20006) on the web that state which are the best firms regarding sales, trading and which are the best in IBD?

Just heard that MS is not that "good" reagarding S&T, is that true?

Look there aren't clear cut tables for that and even then, rankings aren't all what they're cut out to be.

You do have some general sayings that go around such as Lehman and Bear Stearns having two of the best Fixed Income desks, UBS has the largest floor in the world in Stamford and is pretty much the leader in Eurobonds and Goldman FICC is a force to be reckoned with.

yeah makes sense, that already helped a lot.

What about structured credit? In which field is DB leading?

Friend of mine turned down GS(M&A) for Lazard, what do you think about that?

The GS for Lazard is not all that bad an idea. Lazard is focused solely on M&A and restructuring so in essence, they are EXTREMELY prestigious in the M&A side since its their bread and butter business. Not to mention the fact that they are EXTREMELY selective.

I'm not familiar with structured credit but I know someone who's in the industry and said that DB is strong in Europe but its still not a full force in North America.

Obviously its strengths are supposed to lie in German and European industries.

monkeybusiness- i sent you a pm; please check; thanks.

GS does not have an M&A group, the industry groups each do M&A.

If you want to work less hours and do less bitch work but get paid slightly less, work in DCM/ECM. Exit op's may not be as large as someone coming from IBK, but I don't think anyone is going to shun a DCM/ECM 2/3 year analyst stint, it is still impressive. DCM work 60-70 hours per week and still get paid big $$$$$$$$$$$$$$$$$.

is almost staggering.

at its most basic level, the difference between capital markets and "investment banking" is this:

capital markets is focused on PRODUCT knowledge

investment banking is focused on INDUSTRY knowledge

in general, it's pretty damn difficult for any banker to know everything about everything. thus, to make things simpler and to really provide good insight regarding industries and products that most people won't have, investment banks utilize the services of different types of "experts." some of these "experts" will focus on learning and covering the healthcare or software or whatever industry, while others will focus on learning and covering the convertibles market, the equities market, or the high yield bond market.

thus, just as you have "specialists" for different industries, you have "specialists" for different products.

how this all ties together is a function of individual banks. at some banks, product experts merely contribute pages regarding the market for the product, potential pricing for the product/product comps, and the capital raising process/procedure as pertains to that product in order to assist the invesment banker/relationship manager with execution. at other banks, the relationship manager will simply hand off the execution process entirely to the dcm/ecm guy since that guy is the "expert" on the process and the product.

at the end of the day, this is really no different from how things are set up at consulting firms, accounting firms, or even in medicine. you need people who can manage the relationship (what most industry bankers do) and you need people that know about particular products/services (i.e. what product bankers do).

take medicine for instance--you have a general practioner or family doctor that serves as your "relationship manager" w/ regard to medicine. however, does this family doctor know everything there is to know about medicine? no, he doesn't. thus, should more specialized needs evolve, your family doctor would pull in the approproate specialists--maybe a cardiologist to evaluate heart conditions, an oncologist to evalute/treat cancer, surgeons to perform more technical procedures, etc. however, at the end of the days, all of these people are doctors just as ALL ECM/DCM people are bankers.

the difference as i've mentioned earlier is industry focused banking as opposed to product focused banking.

and by the way, dan bush, you're dead wrong regarding your "jack you off middle office" comment, as you've either a) never been in banking, or b) are a such a low ranked analyst that no senior banker will give you any real responsibility.

any analyst who's ever been to a pitch where different products are being put on the table or where different capital raising ideas are being presented will realize that ecm/dcm is front-office advisory position. you may not being advising on pure m&a, but you are providing advice on financing alternatives.

and before you say something else that's dumb, there's no way you can challenge my credentials on this issue. i've not only been a bb industry analyst, but i've also been a corporate development guy at a top f50. when "industry bankers" come to make pitches regarding acquisitions, guess who come along?

that's right--the ecm/dcm guys. in the dream world of college ib-wannabes, m&a advisory is separate and off its own bubble. however, in the real world, most companies can't finance acquisitions with 100% cash on hand. thus, in order to do an acquisition, someone's got to finance it and with various ways of doing this (loans, bonds, converts, equity, etc.) you need people who know the individual products and product markets to give you the best advice on which product is best for your financing needs.

thus, in case of a product such as loans or bonds, industry guys would work with dcm to structure the appropriate loan/bond package, which would then be parceled off to the trading floor where institutional sales guys would find suitable investors. traders would then come in to play by managing liquidity on the secondary market on behalf of clients who wanted to either a) get some of their purchased securities off their books or b) buy in or buy more.

Thanks a lot for such a detailed response.

Yes, Monkeyisland's post is much more exhaustive than mine and largely correct. Briefly though, in my own defense, what I meant by putting "investment banking" in quotes above to refer to the Capital Markets guys is this:

The industry groups are by and large the relationship managers and focused on general corporate advisory, because, obviously, those bankers are specialists (for lack of a better term) in whatever their clients do. The guy with the relationship is virtually always an industry group banker. The industry groups are the ones who are constantly going out and pitching different products depending on market environment, a company's needs, and every other consideration you can think of (products being equity and debt...and every permutation thereof--I'm putting M&A in a different bucket, though it's technically still a "product"), and while the product guys certainly attend these meetings sometimes, they're not the day-to-day, year-to-year client contacts.

Product groups don't do valuation, they don't understand a client's business inside and out, and they may not know a single thing about the other products at the bank. They know their product first and foremost, and they execute.

That is what I meant. It is still investment banking, but not in the "traditional" corporate advisory sense. Which is what most people understand investment banking to be.

.

Capital markets doesn't have the same prestige to the outsider as M&A but at the end of the day, it's still a crucial part of the bank. I really can't believe the "middle of the office jack off" comment...

Monkey Island, thank you for finally posting an intelligent, coherent and accurate post on this subject. It's about time.

good thread.

normal work hours in DCM/ECM (for an analyst) would be 8am-10pm/11pm/12am

would those hours also be likely for lev fin?

8-10 sounds like the right number of hours...but shift by 1 hr...

Supposedly you're supposed to be in by 7AM and accounted for no later than 7:30AM in capital markets so said all my interviewers. Than the higher the rank, the earlier you leave. Usually around 7-8PM on good days. Bad days you can be like the IBD guys.

Think 2 am my son.

same as ibd industry groups and m&A?

I have BB DCM experience. certainly a lot of client meetings and advisory...its not jack-off blah blah...hours are 8-12 usually.

I've heard that a work in CM related to research or structuring is about being concentrated on a particular product while a work in IB consists of a broader range of tasks and analytical stuff. So it makes people more universal. Moreover, some people say that you're likely to play minor role in comparison to traders or sales. But on the other hand, there is an opinion that junior positions in IB imply a lot of grind.

Does anyone have any ideas about it? What job is more interesting in terms of brainwork and career development?

differs from bank to bank. They certainly work with the markets and therefore have shorter hours. Job functions vary in DCM from derivates, high yield bonds to vanilla corporates

good thread

What would someone who does Corporate Finance Advisory work (valuations, modeling, pitchbooks, proposals) for a large investment bank for IPOs, private placements (and some M&A) be called in the States? That's what I do, but in Asia; modelling, valuation and pitching primarily. Don't work at all on selling the issue as part of the syndicate or sales. Would that be called IB or ECM in the States, assuming that the bulk of my work is still IPOs?

The extent to which equity/debt execution tasks are split between the product groups and sector groups varies by bank and by group. I think that the posts above are seeking answers to two questions:

I'll try to move this discussion along by breaking down an IPO into sample tasks and listing the group most likely to handle it. These tasks aren't in order, nor are they comprehensive, but maybe some will find this useful.

Source the deal (sector): Find client. Convince client that an IPO (by your bank) is a good idea. Involves pitchbooks, golf, and booze.

Take the deal to committee (sector): Make sure your bank is willing to take the risk (underwriting is risky).

Negotiate fees (sector): Set an underwriting/bookrunning fee (~7%). Set the "economics" (the fraction of fees paid to each bank on the deal), haggle over how expenses will be shared, and set provisions such as the Green Shoe (an over-allotment option that helps the underwriter to stabilize the stock price following the IPO).

Set a target valuation and range (sector): Come up with a valuation using dcf, benchmarking, and public peers. The client wants a high range, the bank wants a low range.

Refine roadshow presentation (sector and ECM): Help management put forth the best possible pitch to institutional investors. Involves re-tooling powerpoint presentations and coaching management.

Create prospectus (sector and lawyers): Write up a huge document about the business, its management, its market, the risks involved, and a million other things.

Due diligence (sector and lawyers): Make sure the company is legit. Make sure those "factories in Taiwan" actually exist.

Create internal offering memoranda (sector or ECM): Turn the information in the prospectus (if there's extra, don't let the SEC find out) into the banking equivalent of Cliff Notes for the sales/salestraders in S&T so that they can stabilize the offering when it finally hits the market (days/weeks later).

Roadshow (sector and ECM): Fly around for two weeks with the client, making the same presentation 3 times per day to various institutional investors. Sector bankers prep the client for tough questions and occasionally answer the really ridiculous ones. Sector bankers schmooze the investors and introduce the client. ECM (someone at the VP+ level) provides frequent market updates. ECM "builds the book" -- they take orders from the investors.

Pricing (ECM): The team in syndicate (a cap markets function) arrives at a final price for the IPO shares based on the order book.

KEY TAKEAWAYS: For the sector analyst -- "Desirable" work includes the initial valuation, the potential to spend quite a bit of time with the client (e.g. on the road show), and printing the prospectus (the printing offices sometimes have plasma screens, drinks, billiards, and potentially a place to nap).

"Undesirable" work includes writing internal memoranda (time-consuming, last-minute busy work) and revising the prospectus (ditto). An IPO is extremely stressful, and clients justifiably demand some of the most ridiculous services given the enormous fees they pay. Hours are typically longer than ECM (best guess is ~10/wk).

Exit opportunities vary but are generally perceived to be broader than ECM, but this could just be due to confounding by interests.

For the ECM analyst -- "Desirable" work includes being constantly aware of the equity markets (if that's your thing), the lack of pitching. "Undesirable" work includes being called upon frequently to create detailed trading-related reports for sector bankers (e.g. detailed ownership breakdowns and calculations of major shareholders' cost basis).

Hours are typically shorter than in sector groups but days usually begin earlier (~8am in ECM vs. ~9-9:30 in sector).

Thanks for that. By 'sector' I assume you mean the industry sector i.e. TMT, Industrial etc. My bank is very prominent in the Middle East but it's IB team isn't big enough to be split into groups like that, so everyone pretty much handles everything (although obviously who leads the transaction is dependent on who's done that sort of work before). But what I took away from that is that I'm definitely not in what people would call ECM in the States, despite the bulk of my work being on IPOs.

hours: at worst, you have to be there when the traders arrive in the morning and leave when the bankers leave at night (or morning). at best, 12-15 hrs/day comp: IB probably makes more, though it would depend on the group you're in one thing they do: syndication, pricings exit opps: i've been told that DCM gives better exit opps into PE v. ECM, don't know how much of that is true though

Really good thread, thank you everyone.

I am curious about where does lev fin fit in all of this?

And what are the hours like?

How does Equity Capital Markets compare to M&A -the hours, pay, etc. (Originally Posted: 08/16/2006)

How does Equity Capital Markets compare to M&A -the hours, pay, etc.

I had the exact same question. Can anyone in the industry answer this please.

hello

adds no value.

hour = good pay = pretty good you work like 7-7 as analyst (aka trade assistants) usually 5 days a week. some kids add 2-4 hours on sunday afternoon.

Gee, if the pay is good and the hours are good, maybe the IB guys are the true idiots here.

u didnt understand what ECM is..... back that asset up.... is not trading

ecm hour 7-8am til 10pm on average... now and then 3 am 5 am allnighter...

how do the functions differ from M&A

ECM - Equity Capital Markets. Think IPOs, convertibles, follow ons, block trades...M&A- mergers and acquisitions, strategic advice. ECM is a product group. You'll be issuing equity and working in the equity markets. M&A is advisory....likely will work with M&A on a transaction if a company is going to fund the acquisiton by issuing more equity but you wont be doing any of the nitty gritty modeling or valuation work for a merger. You'll rely on comps a lot more than valuation models and rely on the markets perception of an assets value as opposed to a possible intrinsic value (vis a vis dcf etc.).

how is the pay and is this group considered prestigious like M&A?

any idea about this goup in IBD? i believe Citigroup and Lehman has one ..

M&A is the generally considered to be the most prestigious group in ibanking...

ECM is not even close to M&A in terms of prestige.

Difference between i-banking and Capital Markets Structuring & Origination (Originally Posted: 12/11/2006)

I am little confused about the differences between Investment Banking and Capital Markets Structuring & Origination. Would someone please explain the differences between the two.

check out this topic... http://www.ibankingoasis.com/node/1697

TIL WSO used to be IBO

capital markets and IBD (Originally Posted: 09/08/2007)

could someone speak to the merits of working in Global Capital Markets as opposed IBD proper? what are the differences in terms of prestige and exit opportunities?

is a position in GCM at say Morgan Stanley equal to or better than IBD at BoA or CS? thanks.

at MS, GCM is "Equity Capital Markets, Fixed Income Capital Markets, or Leveraged & Acquisition Finance." take your pick.

ECM exit opps are not that great. but all three of these areas are vastly different, and in fact LevFin is a pretty traditional 'IBD proper' job. don't let the organizational BS confuse you.

hmm so would you recommend GCM only if in the Leveraged and Acquisition Finance division?

Do you actually have an offer?

alot of people in general have said that groups like ecm do not have good exit opps. i think that is a poor statement and is largely a matter of perspective. for instance, i could say that m&a has poor exit opps, because it won't teach you how to trade derivatives, or to structure, or to get a market sense for pricing securities, etc etc, and that your only real exit opps are doing just more valuation work at a pe/hf. whereas ECM will give you some sense of valuation skillset, and a very strong sense of equity markets, with exit opps being trading, and then eventually moving to a Citadel/SAC Capital/aqr/etc etc. my point is that all of this is ultimately a matter of perspective; certain tracks are good for certain things. i think if you are disenchanted with banking, but not sure what you want to go into, then capital markets is a great place to be, cause you can trade later on if you think that is your cup of tea (great thing about cap mkts is that they know everyone on the trading floor). this is what i am thinking about doing; i have had great attention from h/f's, but only for doing more valuation work (which is what i do now); i'll never learn to trade properly if i go down that route. it's really just a matter of perspective and what you want.

lateralguy - Why would an ecm banker have exit ops into a quant fund like Citadel? Where have you actually seen ecm bankers go in terms of pe shops and hfs but also internal moves?

Difference between IBD and Capital Markets? (Originally Posted: 07/04/2008)

I was wondering what the difference between IBD and a Capital Markets Group was. Seems the same to me. I'm sure I am wrong though. Thanks!

The Capital Markets Group basically helps firms go public or raise more capital. Banking is more advisory based in the sense that you tell them how to go about a certain acquisition etc. capital markets usually involves a lot of traveling, especially for DCM when you go on roadshows trying to raise capital. Banking has longer hours, DCM and ECM involve less modeling, ECM especially. For DCM, you do a lot of market updates for clients, pricing mechanisms for bonds, bond structuring as per client needs and order book allocation. As per bonuses and pay, they are very similar to banking, perhaps a slight bit more if you do more deals than the M&A group in senior levels, but your skill-set isn't as strong. Usually an attempt to raise capital never fails, so fee generation is pretty damn good. The fee is about 50 - 90bps based on deal size, deal type (144A/reg S) etc. You meet a lot of people, and you build very good contacts, possibly better than M&A since most of your investors tend to be hedge funds, asset managers, buy side/private equity and your issuers tend to be government organizations and corporations. People in DCM usually stay in their field but people who get bored of the job end up going to leveraged finance (which is pretty much dead now), trading desks or even banking. If you make strong contacts, you can also end up going to PE or a hedge fund.

Capital Markets vs IBD (Originally Posted: 03/14/2009)

What makes someone chose to do work in capital markets over investment banking? I understand that the work is somewhat different, and that capital markets faces the "Banking Lite" derision from their IBD counter-parts, but I was curious if those in the industry had any insight to offer into what differentiates the two types of positions.

i worked FIG/DCM at lehman last summer and the question came up frequently. here's what i learned-

senior members of the group with experience in both IBD proper and DCM told me they preferred DCM - because the hours were more predictable; true especially as you get more senior - you close deals more frequently, read: instant gratification (less laboring on a model for a year only to have it get thrown out the window) - faster pace appeals to market junkies, you spend alot of time watching markets (closer to the ground as it were)

I will be returning to (BB?) IBD FT, not sure which group specifically. PM me for more info, hope this is helpful.

best

I had friends at lehman, none of them were in before 9...were you in S&T? The markets being open have no effect on our day to day job...

He said he worked in DCM, which definitely starts at ~7am...

BB Capital Markets vs Mid-Market bank (Originally Posted: 11/26/2009)

I was fortunate enough to be extended offers for a Capital Markets Group at a large BB (BAML, UBS, CS) and for a corporate finance IBD position at a top mid-market bank (Jefferies, Piper Jaffray).

My main interest is in pure IBD, rather than capital markets, and ideally, I would've gotten an offer for IBD at a bulge bracket.

How hard is it to transition from Capital Markets to IBD? Would it be better to start off at a strong Mid-Market, and try to break into the BB?

PJC and jefferies are both bad but IBD > capital markets.

"How hard is it to transition from Capital Markets to IBD?" - Answer: Very hard.

It makes more sense to start with a bigger name on your resume (BAML, UBS, CS) than it does a smaller shop, especially one that's middle market. Starting your career with a bulge bracket is definitely better than starting at a smaller shop. The only reason I'd urge you to reconsider is if you had an IBD offer at a top boutique (Evercore, Lazard, Macquarie, etc.)

I think this is a no-brainer. Go bulge bracket.

Listen, guys from BBs (IBD, not Capital Markets) would obviously have an easier time getting PE jobs after 2 yrs as an analyst. Jefferies is a decent bank and there have been people that have gone there and ended up at good PE shops. Capital Markets will not get you there. I don't buy the argument of the name being important in this case. Even guys in ops can put GS on their resume, does that equal pedigree? No. Relevant experience is more important.

If you want any chance of getting into PE, take the IB position. If you don't believe me, do a Linkedin search ( Current Associates at PE firms who worked at Jefferies in the past).

If you take the Capital Markets Group, you may never break into PE. If PE is the end-goal, going to the BB would be a big mistake.

Hope you make the right decision. Congrats on the offers!

Ignore bracelet. Rofl at him including Macqurie in there, he probably works there. Macq is a piece of crap (excuse my language) to the "elite boutiques" listed. The only 'no-brainer' is the fact that this kid is a complete retard.

Second of all, Advisory is right. Pick MM IBD over BB capital markets. Capital markets has 0 exit ops. At least MM IBD can get you into MM PE or lateral into BB IBD.

Lol, exactly my reaction.

You idiots keep saying this over and over, and it's untrue. If I remember correctly, you work at a lower-tier bank (Citi or something) so maybe the fact that all the analysts at your firm have 0 exit ops is informing your view.

To the OP - you should probably take the MM IBD since IBD is your main interest. The BBs you mentioned aren't all that anyway.

^Well then it would be perfect considering that the op is considering capital markets at "BAML, UBS, CS". I happen to work at one of those banks and I know quite a few capital markets people. So yes, this is MY VIEW and it is quite accurate given the context. They do have around 0 exit ops.

Meanwhile, you don't even work yet and you're in S&T, which I consider a lower tier itself since you will be in SALES. Judging from your username you probably got in through affirmative action ms. senorita.

God, the women on the site are insufferable. Enjoy your senior year and enjoy your sales job but leave the banking threads (including banking hybrids like capital markets) to those who actually work in the industry. Advisory pretty much got it right, there is good advice there.

Which I'm sure you couldn't master in a dozen lifetimes. I've interned in banking as well, at a top BB (GS/MS) which automatically gives me more credentials than even a 3rd year associate at your lowly firm!

By the way, if the capital markets folks at your firm have "0 exit ops" what do they do? Stay there forever? Kill themselves?

You sir are a tool, i was really starting to understand your opinion but then you continued,

Signed, A black woman who does IBanking at the top bank on the street

Congrats on affirmative action? I will surely cry myself to sleep at your dominance, especially among the latino women in the world.

I've already pm'd the answer to several who have asked but they usually progress within the bank (within capital markets) and/or go to MBA school or exit the industry altogether (consulting, law school, even HR).

Rather than flame me, perhaps next time you could have just asked me as I am more than happy to share information such as where my past peers have gone.

Furthermore, you should at least read the OP's post and keep his interests in mind when responding. Here are some IMPORTANT snippets:

"My main interest is in pure IBD, rather than capital markets, and..." "How hard is it to transition from Capital Markets to IBD? Would it be better to start off at a strong Mid-Market, and try to break into the BB?"

Enjoy.

I should have realized that your views were informed by the second-rate analysts from second-rate schools at your second-rate bank. I know a different set of people so I'll save my opinions for a thread asking about exit ops of a Princeton grad at GS or something like that. Although, you will notice that I recommended to OP to go straight into IBD.

By the way, great job turning to the sexist and racist insults right off the bat. Stay classy there.

You're a moron. Signed, white male.

Senorita: So rather than read the posts you will assume every exit op topic is some "Princeton grad from GS". Gotcha, makes sense. You should go post in the Piper Jaffray threads, give them some false hope too perhaps?

Let's just all agree that 1styearbanker is an idiot. Nobody who is above the age of 14 talks like this.

But I try not to inflict narrow-minded views on other people as you and many of the banking-or-die freaks on this board seem to do (S&T is "lower tier" than banking? LMAO). For one thing, OP didn't say where he went to school. We don't know what kind of talent he has. For another, there is a benefit to being a big fish in a small pond vs. small fish in a big pond in terms of exit ops. Just because you happen to know only dumbasses, some of whom are in capital markets, doesn't mean OP falls in the same category.

Why are you arguing with me anyway? Don't you have some fonts to change in a pitchbook? After all, that's what all the smarties in banking are doing. Oh wait, maybe you're taking a break to post racist shit on another message board.

I'm in a similar situation. Any more feedback from full-timers in the industry?

banker and advisory are right though, do IBD over capital markets since you want to do IBD. do not do capital markets unless u wanna stay there

Dude ... you just posted about not getting any FO offer whatsoever and having to do IT... and you feel qualified to comment on the exit ops of capital markets? Based on what knowledge exactly?

Just another example of the idiots I'm talking about.

If you agree then chillax lol. I didn't say I didn't get FT offers, I didn't even start internship search yet? Just asking questions like everyone else. Calm down.

Not that capital markets has no exit ops. Frankly, "nontargetguy", I don't think you should be doling out advice to anybody considering how little you know.

^ You're the bigger tool for bragging about being black and working at a "top bank". Way to play down AA stereotypes... NOT!!!

IBD vs. Capital Markets (Originally Posted: 02/01/2010)

Which one would you choose?

If im not mistaken, capital markets is a group within IBD...

Do you mean M&A or capital markets?

Im sure most will say M&A

IBD no brainer.

It's like if you were asking what would you choose between a SUV and a sport car - it is a matter of interest / things you are ready to give up

M&A, would be more appropriate, but get in first.

IBD Classic vs. Capital Mkts would be most appropriate

Typically (varies by firm), "IBD" is split into normal IBD (M&A, TMT, FIG etc) and "Financing/Capital Markets"

Normally, one would pick IBD classic over financing/capital markets if the end-goal is to get into PE. HOWEVER, the one major exception to this is that Leveraged Finance, a product group, is almost always within the Capital Markets vertical.

LevFin/M&A > Coverage groups > ECM/DCM

is Global Capital Markets easier than ibd/s&t? (Originally Posted: 12/24/2010)

For SA positions, is it easier to get a position in gcm as opposed to s&t and ibd? Or are there less spots in gcm and so the difficulty balances out?

what is the difference between gcm and s&t?

yes

I thought GCM was s&t.....huh

Global Capital Markets is ECM and DCM. I would not say it is not any easier to get into. A lot of banks group capital markets recruiting with normal IBD recruiting. Even if it is separated, it is still just like a normal IBD internship.

ECM? DCM?

Pardon my ignorance.

Equity Capital Markets and Debt Capital Markets.

You should be going after the position because the work interests you, not because you think it's easier to get into than S&T or IBD... They are all competitive and all require slightly variant skill sets/interests... do some research and go after what you really want because they aren't all the same thing and if you are expecting them to be and you pick one randomly you could very well find the position to be frustrating/not what you were looking for...

After reading through some of your other posts, rufiolove, it seems like you really like making assumptions. Where did the OP say he was pursuing a GCM role because it's an easier position to obtain than an IBD or S&T role? You come off as condescending.

I'm pretty sure that the advice I gave was not only legitimate but constructive. Of course I should probably rethink my whole approach to responding to questions on this forum now that the guy who just read Monkey Business finds it condescending...

What other conclusion would anyone reading the OP's question logically draw besides the fact that he was trying to evaluate which Division would be easier to break into?

So essentially, my advice was fine and you're an overly defensive douche who just read Monkey Business... Congratulations!

^^^^ Now that was condescending...

Lmao

GCM like IBD is inside the Chinese Wall. Lev Fin, ECM, DCM fall into the GCM category. In terms of getting an internship, it is no different than S&T or IBD. Depending on the bank, it could be more or less competitive.

Between IBD and S&T: Capital Markets?! (Originally Posted: 06/30/2011)

I am currently work at a top tier bb as a sophomore and have the opportunity to transfer to either S&T or IBD for next year. I would not consider myself very quantitatively inclined, but am familiar with the markets and am more then capable of the requisite mental math work (or accounting for finance). I enjoy learning about the markets and staying up on the news/discussing it, but understand that Sales in S&T may be relatively limiting for exit opps

In the same way, I don't know if I want to sacrifice my life for classic IBD and modeling experience does not really appeal to me as it seems to mean you are in excel all day every day playing with numbers. Whether its as an analyst in IBD or an associate in PE, I imagine that would get old.

How do people feel about Capital Markets in that case as sort of a middle ground? I have read many posts on this forum so far, but I am curios how people feel about Lev Fin (non-modeling group), ECM, DCM in terms of pay, exit opps and how interesting the work would be in contrast to more classic IBD or S&T.

Thanks!

do what you enjoy more, and I mean that

Are you generally interested in higher salaries and bonuses or do you want to learn a lot ?

Well which one is which

Personally I think capital markets offer a nice career (emphasis on nice: not great, not terrible) and I like the blend of markets and corporate banking. But to cover yourself only shoot for Lev Fin as the other two pigeon hole.

Got FT for capital markets position at BB but want to switch over to IBD (Originally Posted: 04/28/2014)

My school is not a target school, and I was able to land a FT offer in a capital markets division at a BB. However, I am highly interested in pursuing IBD. I have an MSF (or will be graduating with one soon), and did an IBD SA internship at a boutique, and a couple other finance internships. My UG major was also finance/accounting. Mentioning this because I feel like I do have a pretty good understanding of valuation, modeling, etc. but I am aware that it does not compare to experience in IBD.

Do I make my intentions known early on to my team? I don't want to give my team the wrong impression that IDGAF about the work were doing and just trying to switch to IBD ASAP.

Also, I actually had two senior alums in the IBD division for the firm that I applied for actually refer me for the position, which is how I landed interviews. When exactly should I reach out to them again and pretty much say I am interested in IBD? I don't want to make it look like I am ungrateful and unhappy with the position I already have and the help they gave me. Hope you understand my points.

I am assuming lateraling after 1-2~ years is the most feasible possibility, but I want to position myself as best as I can. I also would not mind lateraling to a diff BB as well.

congrats.

Are you in DCM? I would try and switch to LevFin (some overlap) and then to PE. Interested to hear what other's have to say...

Start up, work hard, and network into IBD after a year or two. I know several guys that did it at BBs, starting in DCM and lev fin into IBD. Even ECM is doable. Just work hard and meet as many people as you can that's all it really is.

Congrats on the offer

Looking to get into FS/LevFin group for PE eventually, possibly a coverage/M&A group. Will work my ass off regardless.

How open should I be with my supervisors after a year or so? Cause they could possibly help and push for me when I try and lateral internally. I could be wrong though and that could ruin things if I am open with them. Thoughts?

I would evaluate where you are at around the time of your one year review. If at that time you have been doing good work then you might want to drop that over the next year or so you would like to start to make the transition, that gives them time to recruit someone and you time to see deals through. Anything before that seems a bit presumptuous and gives people the wrong impression of you, right or wrong.

Gotcha. Great responses. Definitely right about establishing myself first in my position, and then feeling out what the possibilities are based on how I do. My goal is to get to PE, which is why I am trying to position myself as best as possible given that I am not in a traditional IBD group.

Hi there, I am a currently in a similar situation as yourself (incoming ECM SA) and I want to go into IBD. I will be at a BB next summer in the ECM group, and I am interning at a lower Middle market M&A shop this summer before my junior year of college (non-target). I got a IBD SA offer in at a diff BB but not in NYC, but I turned it down for the BB ECM SA offer in NYC. Do you mind sharing how you made the switch from capital markets to IBD? I'd truly appreciate any tips you could provide. Thanks!!

What's the difference between ECM/DCM and IBD? (Originally Posted: 06/30/2013)

What is the difference between ECM, DCM and IBD? I've went through sites like M&I, and I still don't get a clear distinction between them. Are ECM/DCM exclusively product groups while IBD is an exclusively industrial group?

Also, it seems to me that S&T, ER and ECM/DCM are commonly categorized under Investment Banking, however, there seems to be an Investment Banking Department under Investment Banking itself, does this mean the coverage group?

How competitive would you say it is to get into ECM/DCM vs. IBD? How different are the skillsets required for ECM/DCM vs IBD?

Thanks. Much appreciated.

This is actually a question to which there is no 100% correct answer. Some banks categorize ECM/DCM under the Investment Banking Division, which usually also includes research. Some banks, although I think this is becoming more uncommon, categorize them under Sales and Trading. Some banks even categorize ECM under IBD and DCM under S&T (or FIC, or FICC, or whatever).

The difference really is that ECM and DCM are product groups that are close to the capital markets, and therefore it makes more business sense to put them closer to the S&T groups (physically and/or operationally). M&A is a product group, too, but the nature of their work makes it more logical to organize them closer to the industry coverage teams.

They're all "investment bankers" though, in the sense they are client-facing, do high-profile transactions, and make a lot of money.

ECM/DCM is less modelling intensive, more market-focused and a little "softer" in terms of the skill set. M&A is very modelling intensive and analytical, but a lot of guys in it only know how to model and can't see the forest from the trees. M&A tends to be more competitive to get into, but in reality the standards are not that much different.

As far as skillset required to get into M&A versus ECM/DCM: beyond taking an accounting or corporate finance course, it doesn't matter -- you have no skillset right now, nor does any other college sophomore/junior.

.

if you have a focus under ECM, like healthcare for example, you can switch into healthcare coverage on the buyside.

difference between IB and ECM/DCM (Originally Posted: 03/05/2010)

I'm thoroughly confused on what ECM/DCM does. I know IB is M&A, IPOs, advisory, etc. but where does CM fit in? It's not like S&T so...

Capital Markets groups are the actual source of execution with the bank. DCM provides indicative pricing and issues securities. The banking group "covers" a client sector and handles the relationship with clients.

When a client calls the bank, he calls his banker. The banker then reaches out to the various products (M&A, DCM, LevFin, etc.) depending on client need.

Think about a BioTech company wanting to do an M&A transaction but it needs financing via bank loans, investment-grade debt issuance, and maybe a convertible bond transaction. The banker reaches out to his respective product bankers and organizes a deal team.

You won't be getting any valuation skills in a DCM group. Instead you'll be learning how to keep track of the debt capital markets.

LevFin, M&A, Restructuring, and Industry Groups.

Ipsum dolor similique sapiente facilis ipsum sed perspiciatis iste. Dignissimos laborum omnis magnam non officiis impedit quisquam. Accusantium ipsum et inventore dicta aut. Facilis qui aut voluptatem reiciendis et corporis et.

Debitis qui et sit accusantium voluptatem dolorem. Tempora nulla repellendus nulla odio dolorem voluptatem sit ut. Tempore exercitationem dolorem eos in ea sequi.

Sint velit repudiandae ad maxime non. Voluptas aliquid deleniti harum minus omnis est quis. Officiis itaque aliquid facere necessitatibus qui tenetur.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...

Deleniti molestiae ea praesentium non sed dolorem repudiandae. Architecto magni dolores hic quo. Ipsam numquam numquam harum et. Velit quia ducimus qui est.

Illum eos odit sit omnis assumenda sed. Esse illo sed quod officiis. Atque qui et dolorem veritatis et ut. Quos ipsa dolorem adipisci nulla amet. Ea commodi repudiandae veniam ab non dolore voluptas.

Molestiae ex ut eos nemo. Magnam maiores aliquid a debitis commodi sed aut. Quibusdam totam et cumque consequatur non neque laborum. Est deleniti alias consequuntur voluptate illo aut eaque.

Voluptate voluptas nisi ipsum sint quisquam qui. Ducimus qui nihil excepturi ea doloremque. Voluptas quae distinctio sunt aut adipisci. Consectetur repellat ad non sed aut explicabo iste.

Rerum odit amet quia ipsam inventore pariatur. Temporibus nobis nisi nulla velit rem beatae nihil. Et sequi asperiores quas quo perspiciatis cum. Aut rerum odit at eum aliquid. Rerum quam aliquid veniam cupiditate.

Rerum sit debitis fugiat totam et necessitatibus ad similique. Vel eum adipisci temporibus placeat. Sit nobis aliquid et tempore iure ratione dolores repudiandae. Et fuga delectus hic ad non quo minima. Nisi totam et ut dolorem. Est facilis quo repellendus repellat quia velit. Doloremque accusamus eveniet corrupti neque.

Ab libero facilis neque rerum sint sunt aut. Quia sint asperiores nisi quo omnis iure. Illo et voluptate sit rerum. Ducimus et veritatis quos incidunt accusantium.

Qui voluptatem dicta placeat rerum repellendus atque nam. Placeat id voluptates blanditiis dolores omnis sint. Est sunt ipsum aut quia est. Quibusdam a optio omnis. Ab qui qui amet sunt et natus.

Exercitationem fugit omnis quod. Adipisci enim maiores voluptatibus dolorum veritatis et. Delectus voluptatibus velit velit accusamus aut.

Assumenda temporibus et quam quia ullam autem ipsam. Consequatur sequi tempore dolor soluta asperiores.

Ab fugit ipsum dolorem sapiente libero libero aut. Sit cum assumenda saepe nemo est.

Recusandae nulla voluptas maiores dolor animi. Ut qui ut eaque omnis. Mollitia deleniti ipsam cum sed. Officia autem natus odio. Eos ducimus enim recusandae minus reiciendis ullam atque.

Odit facere quis provident aut dolorum illo. Numquam aperiam odio distinctio temporibus accusamus est consectetur. Libero molestiae dolor porro omnis non. Est iusto eligendi provident fugit dolores.

Sed illum omnis magnam voluptate quibusdam officia. Non ex quam maiores maiores dolorum et aut. Et velit facilis adipisci est dolores aut.

Cumque voluptatibus id ex facilis doloribus unde cumque doloremque. Distinctio corporis rerum consequatur tempore. Non doloremque enim nihil rerum non repellat debitis voluptatibus. Fuga natus eum sint ut deleniti. Quia aliquid rem harum doloribus nihil. Hic quaerat corrupti in quos atque.

Ut vitae quaerat voluptatem quia cupiditate modi quasi. Omnis non quibusdam debitis sit. Consequatur unde ratione voluptatem repudiandae. Dolorem non amet est occaecati asperiores nihil.

Labore non accusantium voluptatem in corporis et. Et et sit et aut perferendis fugit. Nobis beatae ratione et voluptas eum.

Dolore aut est aut voluptate mollitia possimus velit praesentium. Rerum eos accusamus quis enim dolorum facilis ipsa. Excepturi repellat voluptatem blanditiis neque error voluptatem.