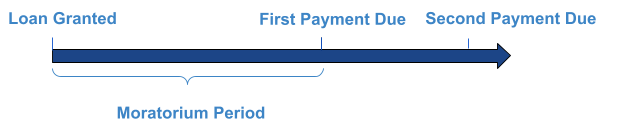

Moratorium Period

A period during which a borrower is not required to make any interest or principal payments on the amount borrowed.

What Is A Moratorium Period?

A moratorium period is a period during which a borrower is not required to make any interest or principal payments on the amount borrowed. This period is standard for home loans and educational loans. Although costs are not needed during this period, interest generally accrues.

These periods are only given as justified. They have to be asked for a good reason, and the lender can approve the request and provide it to the borrower or disapprove it. A moratorium is not guaranteed.

Many borrowers' reason for this period is due to financial hardships. This period allows individuals to have a couple of months to gather the funds before getting back to paying back the lender.

Moratoriums are given on numerous personal, home, credit cards, and educational loans. Educational loans are most common for this period because some students have a gap between graduation and obtaining a job.

Moratoriums are also common for home loans because after buying a house, individuals might need some time to stabilize their finances before continuing to repay the loan.

The period generally starts after the loan is granted. This allows the borrower to sort out their finances before repaying the loan.

There are also instances when the moratorium period starts in the middle of the loan. Although the borrower is not making any payments during this period, interest is still accumulating.

- A moratorium period is a specified duration during which a borrower is not required to make any principal or interest payments on a loan. This period is typically granted at the beginning of the loan term to provide relief to the borrower.

- The primary purpose of a moratorium period is to give borrowers time to improve their financial situation without the pressure of immediate repayment obligations.

- The main advantage of a moratorium period is the immediate financial relief it provides to borrowers, allowing them time to stabilize their finances.

- However, the disadvantage is the potential for increased overall debt due to interest accumulation and extended repayment periods, which can lead to higher total repayment costs.

Example Of Moratorium Period

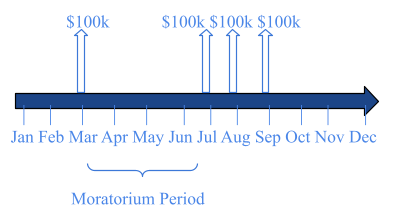

Maria's bank provided a $300,00 loan in February 2020 to help with her store. She agreed to pay fixed monthly payments of $100,000 over four months for a total repayment of $400,000.

However, in March 2020, due to the pandemic, Maria was forced to close her store. Since this was not planned, her bank granted her a moratorium period from March 2020 to July 2020, so she did not have to repay the loan during these months.

The diagram below shows what happened during Maria's repayment process after she was granted the moratorium:

So, instead of her last $100k payment being made in June, her previous cost got pushed back to October 2020.

Here is a real-world example of a moratorium:

In March 2020, the Reserve Bank of India (RBI) offered relief to loans, including educational, personal, and home loans. This lasted from March 1st, 2020, to August 31st, 2020.

In March 2020, the US set a federal student loan moratorium. It was made to help borrowers with economic hardship caused by COVID-19. You can find more information about it at this link.

The federal student loan moratorium is still present, as many individuals are hoping for a longer extension.

Moratorium Period vs. Grace Period

Many people need help understanding the difference between a grace period and a moratorium period, as they are easily confused.

When a grace period occurs, interest does not build. This allows the borrower to make payments during this period before the payment is due. However, interest builds after the payment is due.

In terms of interest, a moratorium is different from a grace period. During this period, interest generally accrues, but the borrower is not required to make any payments.

Another difference between these periods is the lengths. Moratoriums are generally longer than grace periods. Grace periods typically last 21 to 25 days, while moratoriums can last for months.

When a lender grants a grace period, it is generally extended to all customers. This is different from a moratorium because it must be individually requested, and the lender has the power to approve or not allow a suspension.

Benefits and drawbacks of Moratorium Period

If you are considering asking for a moratorium, it is essential to know both the benefits and the drawbacks before deciding.

Benefits

- No impact on credit score: The moratorium does not negatively impact your credit score, so it does not affect the borrower's borrowing capacity.

- Good repayment plan: Moratoriums allow borrowers to make a better plan on how they will repay the loan. In addition, the time moratoriums give individuals can help them accumulate the funds needed to repay their loans.

Drawbacks

- No interest waiver: Although borrowers do not have to pay during moratoriums, interest is still accumulating. The accumulation of interest is the biggest drawback because moratoriums may lead to additional interest charges, resulting in more pressure on the borrower.

- Longer loan tenure: A break in the repayment schedule leads to increased loan tenure. This means that if you had a repayment method set to pay the loan back within four years, it would now be longer than you scheduled.

- A moratorium could be used for individuals who have a good plan. Borrowers usually use it with effective discipline because they will stick to the project they made when they asked for a moratorium.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?