VA Loan

Also abbreviated as a VA Loan, is a mortgage loan program available to eligible veterans in the United States.

What Is a VA Loan?

The Veterans Affairs loan, also abbreviated as VA loan, is a mortgage loan program available to eligible veterans in the United States. It is administered by the Department of Veterans Affairs.

This loan aims to help veterans pay for housing after their service. The veterans themselves do not offer the loans but offer programs to help them pay for them and contact private lenders to provide them with the benefits of the loan.

Eligibility for the loan varies, and individuals must meet specific criteria. Eligible citizens will typically consist of active-duty service members and some surviving spouses of military personnel.

The eligibility criteria for the VA loan are very strict and can even come to how many years the individual served in the military.

A Certificate of Eligibility, or COE, is a document provided by the VA to determine eligibility. This ensures that only the correct personnel are reaping the loan benefits.

One of the notable advantages of this loan is that eligible borrowers can obtain a mortgage without making a down payment. This feature can benefit individuals with little savings for a down payment.

VA loans generally offer competitive interest rates compared to conventional loans. This means the interest rates will be lower, resulting in cheaper monthly mortgage payments. This unique advantage saves borrowers money over the life of the loan.

VA loans are also assumable. The loan can be transferred to a buyer if the borrower wants to sell their home. Assumability can make the home more attractive to potential purchasers since they can assume the mortgage terms are cheaper.

It is important to note that while VA loans offer numerous advantages, borrowers should still meet the lender's underwriting requirements and fulfill their financial obligations.

Additionally, the VA loan program applies to primary residences and has certain loan limits based on the property's location.

- A VA loan is a mortgage loan program established by the United States Department of Veterans Affairs (VA) to help veterans, active-duty service members, and certain members of the National Guard and Reserves purchase homes.

- The VA does not lend money directly but guarantees a portion of the loan, enabling lenders to provide more favorable terms.

- VA loans offer various repayment terms, typically ranging from 15 to 30 years, with fixed or adjustable interest rates.

- Veterans, active-duty service members, members of the National Guard and Reserves, and certain surviving spouses are eligible. Specific service requirements must be met, which vary based on service dates and duty status.

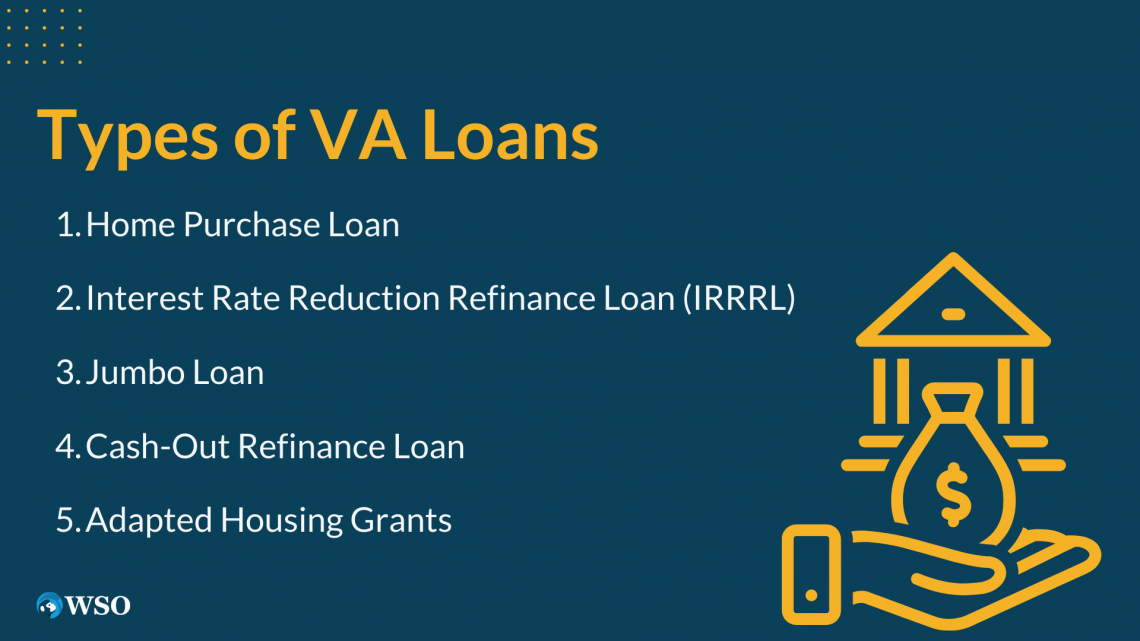

Types of VA Loans

The VA offers several VA loans to help veterans with their specific needs. These aim to give back and support the veterans who helped serve our country.

Here are the main types of VA loans available:

- Home Purchase Loan

- Purpose: This loan type is used for purchasing a primary residence, like a single-family home or townhouse.

- Features: Borrowers can finance up to 100% of their purchase without a down payment. However, there are specific loan limits based on the location of the property.

- Benefits: No down payment requirement, competitive interest rates, no private mortgage insurance (PMI) needed, and flexible credit requirements.

- Interest Rate Reduction Refinance Loan (IRRRL)

- Purpose: This loan is designed to refinance an existing VA loan into a new loan with a lower interest rate.

- Features: The IRRRL program aims to reduce the borrower's monthly mortgage payment or switch from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage.

- Benefits: Streamlined application process with reduced documentation, no requirement for a new appraisal or credit underwriting, and potential for lower monthly payments.

- Jumbo Loan

- Purpose: VA jumbo loans are designed to accommodate higher loan amounts than the standard VA loan, whether it's because of a bigger house or more expensive area

- Features: Borrowers must pay a down payment and require a funding fee.

- Benefits: No private mortgage insurance, competitive interest, or government-backed guarantee.

- Cash-Out Refinance Loan

- Purpose: This loan allows borrowers to access their home's equity by refinancing an existing mortgage and receiving cash proceeds.

- Features: Borrowers can refinance up to 100% of the home's value, paying off the existing mortgage and receiving cash for other purposes, such as home improvements, debt consolidation, or education expenses.

- Benefits: Potential to obtain funds for various needs, competitive interest rates, no PMI, and flexible credit requirements.

- Adapted Housing Grants

- Purpose: The VA offers grants to help disabled veterans modify their homes to accommodate their disabilities.

- Features: These grants can assist with home accessibility improvements, such as ramps, wider doorways, bathroom modifications, and other necessary changes.

- Benefits: Financial assistance to improve housing accessibility and enhance the quality of life for disabled veterans.

While these are some of the main types of these loans, many others might fit one’s needs better. Consulting with a VA-approved lender or the Department of Veterans Affairs would be wise to gain comprehensive information on each loan program.

Note

There are still specific eligibility criteria and program requirements that may apply to each

How to Apply for a VA Loan

Applying for a VA Loan involves several steps and can sometimes be complicated and overwhelming. To make this process easier, we’ve provided you with a couple of steps you can take to apply for a VA Loan.

Here is a list for applying:

- Confirm Eligibility: To determine eligibility for this loan, you must get a Certificate of Eligibility from the VA. This certificate is referred to as the DD214 Form, and obtaining it can take up to six weeks.

- Find a VA-Approved Lender: Research and choose a VA-approved lender who can help you find a loan.

- Gather Required Documents: Collect the necessary documents for the loan application. The lender should provide a specific list of required documents, but they will typically include any identification, proof of income, and employment history.

- Prequalification: The VA-approved lender will help get you prequalified for the loan. They will review your financial information and determine an estimated loan amount you may qualify for. The financial information they review is usually based on your income and other factors.

- Loan Application: Once your offer is accepted for a home, submit a formal loan application to your chosen lender. Your lender should guide you through the application process and provide the necessary paperwork.

- VA Appraisal: The lender will order a VA appraisal, where they determine the property's fair market value according to VA's property standards.

- Underwriting and Approval: The lender will review your application, supporting documents, and the VA appraisal. They will assess your creditworthiness and the property's eligibility for VA financing. You will receive a loan commitment letter when approved.

- Loan Funding: After signing all necessary documents, the lender will review and process the closing package. Once satisfied, they will fund the loan, providing the funds to the seller or closing agent.

These specific steps and requirements will vary depending on your lender and any individual circumstances. However, this is the general process for applying for this Loan. Working with a VA-approved lender will ensure a smooth application process.

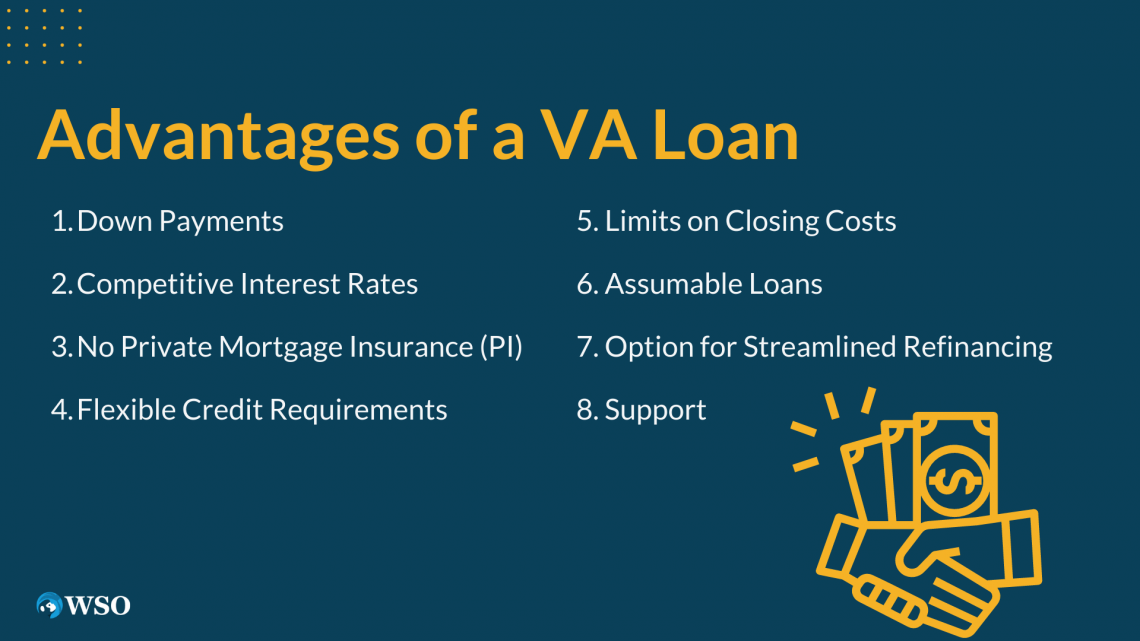

What are the Advantages of a VA Loan

VA loans benefit eligible veterans, active-duty service members, and qualifying surviving spouses. Here are some notable benefits of VA loans:

- Down Payments: One of the most significant features of VA loans is the lack of a down payment. This makes owning a home much more accessible for veterans who might not have been able to save up money for a down payment.

- Competitive Interest Rates: These loans often offer lower interest rates than conventional loans, which helps borrowers save money over the life of the loan.

- No Private Mortgage Insurance (PMI): Unlike many other loan programs, these loans do not require borrowers to pay for private mortgage insurance. PMI is a free borrower have to pay to protect the lender in case you can no longer pay them back. It is typically required for conventional loans.

- Flexible Credit Requirements: While lenders still consider creditworthiness when issuing this loan, borrowers may have more leniency regarding their credit scores and history. This flexibility can make loans more accessible to eligible individuals with questionable credit.

- Limits on Closing Costs: The VA limits the closing costs that borrowers can pay. These limits protect borrowers from excessive fees associated with obtaining a mortgage.

- Assumable Loans: VA loans are assumable. This feature can make the home attractive to potential purchasers, especially with higher interest rates.

- Option for Streamlined Refinancing: VA loans offer streamlined refinancing options, such as the Interest Rate Reduction Refinance Loan (IRRRL). These programs allow eligible borrowers to refinance their loans to secure favorable terms.

- Support: The VA’s mission is to provide benefits to those veterans. Therefore, they support borrowers throughout the life of their loan. The VA has resources and programs to help borrowers facing financial difficulties.

While these loans offer numerous benefits, borrowers must still meet the lender's underwriting requirements and fulfill their financial obligations. This loan's leniency is not a substitute for refusing to meet the lender's standards.

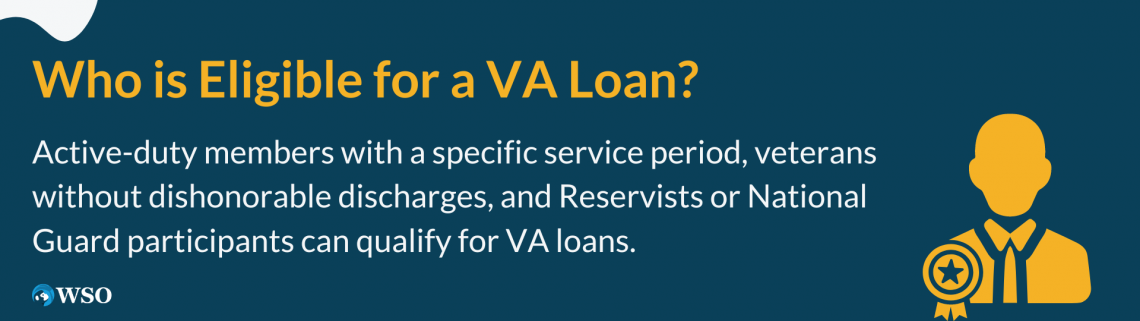

Who is Eligible for a VA Loan

The VA determines the eligibility for this loan. There is a general criterion, but it usually consists of individuals who have or are currently serving. However, there are certain outliers to these requirements.

Of course, current active-duty members may be eligible for VA loans. However, the minimum continuous active service period is 90 days during peacetime or 181 days during wartime.

Current active-duty members can take advantage of this loan, and Veterans may also be eligible. If a Veteran has not been discharged under dishonorable conditions, it’s safe to assume they can obtain this loan.

Note

The specific length of service requirements may vary depending on when and how long the individual served.

The VA acknowledges your service if you were a Reservist or National Guard member outside of the military and navy. Therefore, a Reservist or National Guard participant who completed 6 years of service will also be eligible for the loan.

If you are an individual who did not serve, you still may be able to qualify for this loan. Suppose you are a surviving spouse of any military service member who had died in the line of duty or due to a service-connected disability. In that case, this loan is accessible to you.

Summary

A VA loan is a mortgage program designed explicitly for eligible veterans, active-duty service members, and qualifying surviving spouses. This loan is VA-backed to help those who have served in the military.

These loans have many advantages compared with conventional loans. One of the many advantages of this loan is that it doesn’t require a down payment. This is because service members typically need to have the luxury of saving money while on duty.

VA loans also offer competitive interest rates, often lower than conventional ones. In addition, VA loans do not require borrowers to pay for private mortgage insurance (PMI).

The eligibility requirements for a VA loan depend on the individual's military service history. Eligibility can only be established by obtaining a COE from the VA.

While these loans come with numerous benefits, some considerations must be remembered. These include funding fees, specific property eligibility requirements, and potential limitations on loan amounts.

It's important for prospective borrowers to consult with a VA-approved lender to evaluate the best options for their specific circumstances.

Overall, VA loans provide a valuable opportunity for eligible individuals to achieve homeownership with favorable terms and financial advantages.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?