Highly Compensated Employee

A person is considered an employee if he gets paid to work for another person or company

What Is A Highly Compensated Employee (HCE)?

According to the Internal Revenue Service, anyone who has completed one of the following actions is a Highly Compensated Employee (HCE):

1. Ownership

Regardless of the pay they earned or got, at any point in the year or the year before, they owned more than 5% of a business.

Assume Jack, one of the employees in your organization, owned 10% of the plan sponsor in 2021. Jack is regarded as an HCE because she had at least a 5% ownership stake in the business during the year preceding.

2. Compensation

HCE must receive payment from the company above $130,000 in 2021 (or $135,000 in 2022) if the employer chooses, and was in the elite 20% of employees when assessed by compensation.

For example, ABC company starts a retirement plan on January 1, 2022. In 2021, an employee got $200,000 from their company. The employee is regarded as an HCE because 2021 is the tax year prior, and the sum exceeds $130,000.

Bonuses, commissions, overtime pay, and other benefits are all considered part of the employee's compensation and regular recurrent employer payments.

The value of a company's shares is used to calculate the 5% interest rate. It covers the interests in the same company attributed to the employees' interests and those of their wives, kids, and grandkids.

For instance, a person, Roy, owns 2.5% of the stock in a company, his wife owns 1.8%, and their child owns 1.2 %. Therefore, their combined ownership in the business amounts to 5.5%, which is greater than 5% and qualifies them as highly compensated employees.

- Highly Compensated Employee (HCE) is an individuals who either own more than 5% of a business or earn above a certain compensation threshold (e.g., $130,000 in 2021).

- HCE faces limitations on contributions to 401(k) plans due to nondiscrimination tests, ensuring fair treatment for all employees.

- HCE can explore alternative retirement savings options, such as Roth IRA, Backdoor Roth IRA, Health Savings Account (HSA), and taxable accounts.

- Being an HCE may come with higher compensation but also demands higher productivity and work quality, as companies expect more from well-paid employees.

- Key employees are individuals who play a significant role in the ownership or decision-making of a company, often receiving better benefits or remuneration. They are subject to similar tests as HCEs for retirement plans.

Limitations of 401(K) Over HCE

A 401(k) is a retirement savings and investing plan provided by employers. A 401(k) plan offers a tax break on the contributions made by the employees.

A tax break is a tax deduction or exemption received by individuals or businesses to save money. The government generally offers it, reducing an individual's or business's total tax liability.

Contributions are deducted automatically from employee paychecks and invested in funds selected by the employee, such as:

- Backdoor IRA

- Roth IRA

- Health Savings Account

- Taxable Account

In 2022, the annual contribution limit for 401(k)s is $20,500 ($27,000 for those 50 and older).

The 401(k) plan is a defined-contribution, tax-deferred pension plan. Employees can make unlimited contributions to their goals, with a ceiling of $19,500 per year for 2020 and 2021.

Employers may match the contributions up to a specific proportion. Employees take risks and make their own investment decisions. Highly paid employees might contribute more and gain more from the tax deduction, especially in a higher tax bracket.

The IRS places additional restrictions on the number of contributions that HCE may make to ensure that everyone has access to retirement benefits equally.

Every year, the IRS requires all 401(k) plans to undergo a nondiscrimination test. The plan fails the nondiscrimination test if the average contribution-to-salary ratio of highly rewarded employees is more than 2% higher than the ratio of other employees.

For instance, a company's non-highly compensated employees contributed an average of 6% of their annual pay.

The highly compensated workers could only contribute 8% of their annual earnings. The total contribution by an HCE can't exceed the actual contribution by a non-HCE by more than 2%. The plan will not pass the test if it exceeds the 2% limit. The employees must receive all of the contributions.

Highly Compensated Employees—Additional Factors

You can still contribute as much as your employer allows HCEs to contribute without penalty to a 401(k). Nonetheless, you may want to consider ways to supplement your retirement savings beyond a 401(k)So, let's look at some alternatives down below.

1. Backdoor Roth IRA

These employees can make a certain number of 401(k) plan contributions. But, they can enhance their retirement funds through other methods, though.

One option is they can open a backdoor Roth IRA or make post-tax contributions to conventional Individual Retirement Accounts (IRAs).

2. Roth IRA

Contributions are not tax deductible, but withdrawals are not subject to taxes. Employees making more than $139,000 annually are not eligible for Roth IRA. Still, the backdoor Roth IRA gives highly compensated workers the chance to convert their standard IRA accounts to Roth IRAs.

3. Health Savings Account

Health Savings Account (HSA) is a tax-advantaged savings account used to pay for specific health care or medical costs. HSA withdrawals are tax-free and can be funded with pre-tax income. Moreover, a person can quickly transfer the funds to your savings or checking account.

HSAs provide tax advantages to its holder, but the withdrawal policies are highly burdensome. There are specific cons attached to HSA:

First, before age 65, withdrawals for non-qualified costs will be taxed and subject to 20% penalties. Another negative would be the high cost of transaction commissions and monthly maintenance fees.

4. Taxable Account

A taxable account is an account that allows the investor to deposit funds & buy and sell investments through the report.

You can also think about putting some money into taxable assets. But, of course, you can always create a brokerage account for yourself and invest in assets like mutual funds, bonds, equity, debt, and small cases, regardless of your income.

In addition, regardless of your income, there are no contribution caps. You would also have access to your investments whenever you needed them.

Being a highly compensated employee has an appealing ring to it. This may also imply that you will have a few chains on your retirement nest egg, but be thankful that an HCE has many other options.

An HCE can open a Roth or Backdoor IRA or convert your traditional IRA. Opening an HSA can also provide you with tax benefits while allowing you to save for future medical expenses. Furthermore, regardless of income, you can always create & invest in taxable accounts.

HCEs can maximize their retirement contributions by considering all available options, such as 401(k) plans and traditional IRA conversions or others. However, they should also carefully weigh each opportunity's benefits and drawbacks to maximize their tax return savings.

Cons of a Highly Compensated Employee

Everyone wants a job that pays well and can provide job satisfaction or is enough to make a living. Still, it is surprising to learn that there are certain drawbacks of being a "highly compensated employee," or HCE.

It is essential to learn that an HCE doesn't necessarily enjoy a superior status in the organization.

A highly-paid job always comes with some drawbacks. In return for higher compensation, companies or employers can also demand higher levels of productivity or higher work quality to be achieved by the employee.

The IRS is responsible for conducting nondiscrimination tests for companies' 401(k) plans. These tests are:

- Actual Deferral Percentage (ADP)

- Actual Contribution Percentage (ACP).

The primary purpose of conducting these tests is to ensure that average and highly compensated employees' 401(k) contributions are proportional to each other. The other main motive of these tests is to identify which employees are HCEs and which are NHCEs so that an organization can't discriminate between the two.

Suppose an employee is affected by the HCE rules. In that case, he/she can reach out to the employer or financial advisor to get advice on how to keep saving for retirement when 401(k) contributions are maxed out beyond the prescribed limits.

Who are Key Employees

The phrase "key employees" may also be used about highly compensated workers; therefore, who are key employees?

An employee who plays a significant role in the ownership or decision-making of a company is referred to as a key employee.

Key personnel typically receive more excellent benefits or remuneration in comparison to other employees. Therefore it is essential to classify each employee in the organization appropriately.

HCEs can also work as key employees. But one of the following given conditions must be met:

-

A company officer sponsoring the plan earns $200,000 or more in actual compensation for the 2022 determination year (or $185,000 for the 2021 determination year).

-

Employees who own more than 5% of the company or are related to someone who does are subject to the 5% owner test.

-

Employees who own more than 1% of the company and earn more than $150,000 are subject to the 1% owner test (not adjusted for inflation).

Similarly, you may determine if your person is a key employee by using the exact tests mentioned above.

Knowing how many HCEs and critical employees a company has can help identify whether your retirement plan is top-heavy.

When the organization's owners and highest-paid employees (or key employees) control more than 60% of the value of the plan assets, the arrangement is referred to as a "top-heavy plan."

What is a Nondiscrimination Test

Every year, all 401(k) plans must submit to a nondiscrimination test by the Internal Revenue Service (IRS). Well-compensated employees and non-highly compensated employees are divided into two groups by the exam.

The compliance test examines HCE contributions to see if all employees in the organization are treated fairly under the company's 401(k) plan. The anti-discrimination provisions are in place to prevent employee retirement plans from favoring highly compensated workers.

The IRS was able to control deferred plans and ensure that businesses weren't merely creating retirement plans to benefit their CEOs by defining highly compensated employees.

The 5% criterion is determined by either voting power or the share price. A person's interest includes the interest that is attributed to their spouse, parents, children, and grandparents but not to their grandchildren or siblings.

A worker who owns exactly 5% of the business is not regarded as a highly paid employee (HCE); however, someone who owns 5.01% of it is.

An example: An employee A who owns 3% of the company, for instance, will be regarded as an HCE if their spouse owns 2.2% of the same business, making it an overall of 5.2%.

The nondiscrimination test ensures that HCEs do not overly utilize plans in their benefits.

Highly compensated workers and key staff must adhere to a predetermined contribution rate during the testing. In addition, every year, 401(k) plan employers must pass a nondiscrimination exam.

You can use the following for nondiscrimination testing:

-

Highly compensated employees - Ownership test OR compensation test

-

Key employees - Officer test OR 5% owner test OR 1% owner test

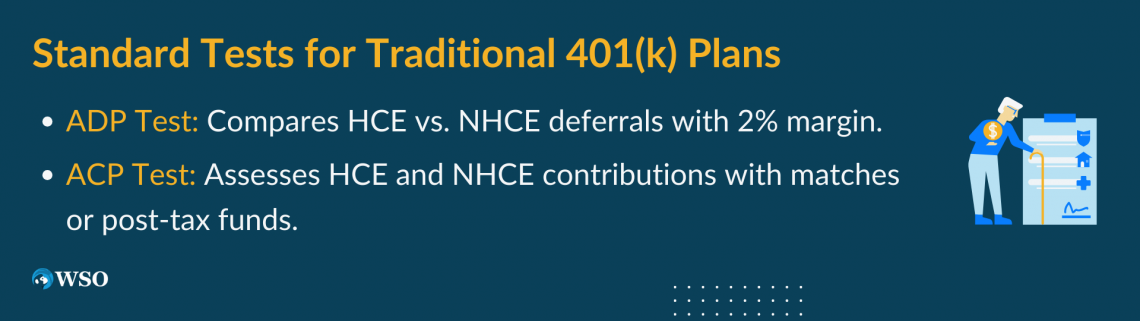

Standard tests for traditional 401(K)

Along with the above tests, you may also decide to use standardized tests for traditional 401(k) plans. The standard tests include:

-

ADP test

-

ACP test

1. Actual deferral percentage test

The actual deferral percentage test (ADP) compares the average salary deferral of participating highly compensated employees (HCEs) to that of non-highly compensated workers (NHCEs). The result percentage represents the participation of each employee in the retirement plan.

You must figure out two percentages to pass the ADP test:

- Calculate the average yearly employee deferral rate as a percentage of the HCEs' total pay by adding the HCEs together.

- The average yearly employee deferral rate as a percentage of total remuneration is determined by adding all the NHCEs.

- If the HCE group's average falls within a specific range of the NCHE average, the plan passes the ADP test.

- That margin is typically two percentage points. For instance, the HCE average cannot be greater than 4.50% if the NHCE average is 2.50%.

- The NHCE average affects the permissible percentage even if the normal guideline is two percentage points. If you're utilizing the ADP test, refer to the chart below:

| NHCE Average | Maximum HCE Average |

|---|---|

| 2% or less | NCHE average X 2 |

| 2 – 8% | NHCE average + 2 |

| More than 8% | NHCE average X 1.25% |

2. Actual contribution percentage test

Only companies that offer a 401(k) match or after-tax contributions are subject to the actual contribution percentage test (ACP).

It is similar to the ADP test; the same calculations and breakdowns are used. They may factor in employer matches and post-tax contributions when making their computations.

Calculate the average contribution rate for HCEs and NHCEs, for instance, considering a 401(k) match (if appropriate).

Researched and authored by Purva Arora | LinkedIn

Reviewed and Edited by Raghav Dharmarajan

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?