Interest-Only Mortgage

Mortgage loans in which the borrower is required to pay just the interest over a period.

What Is an Interest-Only Mortgage?

Interest-only mortgages are mortgage loans in which the borrower is required to pay just the interest over a period.

But does this only mean that interest must be paid? It would have been incredibly satisfying if the situation unfolded as desired. Regrettably, things don't operate in that manner.

The principal amount will be paid either in a lump sum or in subsequent installments.

Interest-only mortgages require only the payment of interest during the introductory period, which is predetermined (typically five, ten, or more years). The interest rate on these types of mortgages is generally on the higher side.

These loans are structured as an interest-only adjustable-rate mortgage (ARM) in which you pay a fixed interest during the introductory period. After the principal + interest payment starts, the interest rates will start to vary.

Suppose you take a 10/1 Adjustable Rate Mortgage, It means that your introductory period, when you pay only interest, will be 10 years, and after that, the interest rate will be subject to change or adjustment once a year.

Typically the mortgage can be structured in two ways:

- Pay interest for the introductory period; after the introductory period ends, you pay principal along with variable interest till the end of the term.

- Pay the interest on the loan for the whole term and the principal at the end of the term.

The person taking a loan has a few alternatives at the end of its term:

- To refinance the loan (with the possibility of getting it at a lower interest rate)

- To sell the property for which the mortgage is taken

- To pay a lump sum or pay interest and principal for the remainder of the period.

As a result, interest-only mortgages allow customers only to pay interest during the initial period. Following the interest-only period, the loan would be amortized over the remainder of the tenure, which can be paid in a lump sum or through the sale of the property.

- An interest-only mortgage is a home loan where the borrower pays only the interest for a specified period, usually 5 to 10 years, and then must begin repaying both the principal and interest.

- Interest-only mortgages are suitable for individuals with variable incomes, low initial funds, or expectations of future income growth. They can benefit buyers starting with lower salaries, allowing them to manage cash flow effectively and build equity over time.

- Lenders typically have stricter qualification criteria for interest-only mortgages. Borrowers may need higher credit scores, lower debt-to-income ratios, and proof of stable or increasing income to qualify for these loans.

- Interest-only mortgages often have adjustable interest rates, which means the interest rate can change periodically based on market conditions. This can lead to unpredictable monthly payments after the interest-only period.

Interest-Only Mortgages vs. Traditional Mortgages

Let’s highlight how an Interest-Only Mortgage differs from a Traditional Mortgage.

Traditional mortgages are loans that the borrower repays periodically, comprising both principal and interest. These payments gradually reduce the principal amount borrowed, building equity in the home over time.

For those who earn a good income and plan to remain at home for an extended period, conventional mortgages are usually the most reliable in terms of time commitments.

They provide the opportunity to accumulate equity and benefit from potential appreciation in the housing market. Traditional mortgages also offer the advantage of fixed interest rates, providing stability and predictability in monthly payments.

| Point | Traditional Mortgage | Interest-Only Mortgage |

|---|---|---|

| Frequency of Payments | The borrower has to pay the principal along with the interest to the lender. | Only the interest payment for the introductory period and the principal, according to the agreement. |

| How common is it? | The most common form of mortgage financing. | A less common form of Mortgage financing. |

| Size of Payments | For the Introductory period: Higher than Interest-Only Mortgage. | For the Introductory period: Lower than Traditional Mortgage After the Introductory period: Higher than Traditional Mortgage |

| Equity Buildup | Consistent property build-up throughout the term. | No buildup of equity in the introductory period, but constant buildup after the Principal+Interest payment starts. |

| Level of Risk | Lower level of risk as compared to Interest-Only loans. | Higher level of risk as compared to Traditional mortgage |

| Who is it most suitable for? | 1. People are ready to pay an equal amount of money throughout the term. 2. Salaried Mid-career professionals are the most common. |

1. People who are not ready to pay higher amounts now due to insufficient funds but will be able to in the future. 2. Businessmen and Early-career professionals are the most common. |

However, one must weigh the pros and cons of Traditional and Interest-Only Mortgages and make a well-calculated decision about which mortgage to choose since this is one of the most significant decisions for one's financial independence in the future.

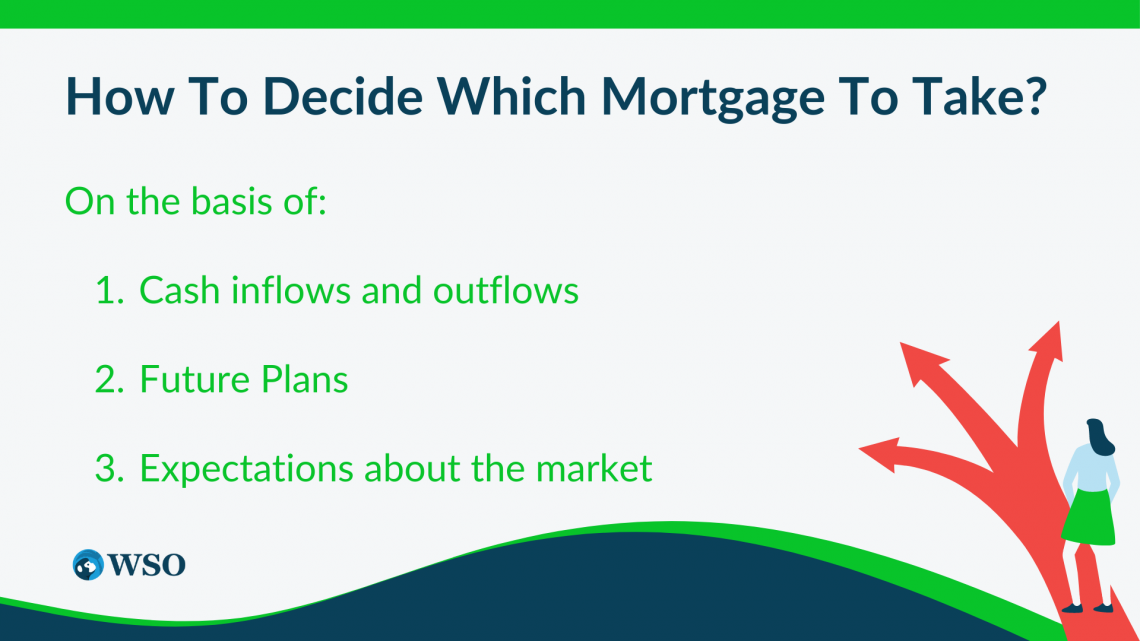

How to decide which mortgage to take?

One can look at various parameters while deciding on the type of mortgage. They are on the basis of the following:

1. Cash inflows and outflows

- Traditional Mortgage

If you have a stable income and can afford a higher monthly payment now. With a stable income, you can comfortably make consistent monthly payments towards principal and interest, gradually building equity in your home. - Interest-Only Mortgage

An interest-only mortgage may be an attractive option for people who have fluctuations in income, struggle to make ends meet, or face low levels of today's earnings but expect them to rise further down the road.

NOTE

By paying only the interest during the initial period, your monthly payments are lower, providing temporary relief until your income situation improves.

2. Future Plans

- Traditional Mortgage: One must also consider using a traditional mortgage when you want to stay in your home for some time. Since you intend to live in the property for an extended period, it makes sense to establish equity through regular payments, taking advantage of the potential appreciation in the home's value over time.

- Interest-Only Mortgage: Interest-only Mortgages may be better suited to you if you are thinking about selling your house soon. This type of mortgage allows you to reduce your monthly payment in the short run while planning a property sale before its principal repayment period.

3. Expectations about the market

- Traditional Mortgage: If you and market analysts expect the housing market to be unstable, a traditional mortgage may be the preferred choice. To protect yourself from possible volatility in the market, you may choose a Fixed Rate Mortgage, which guarantees an unchanging interest rate.

NOTE

The stability helps in budgeting and provides security against rising interest rates.

- Interest-Only Mortgage: If you and market analysts expect the housing market to be stable, an interest-only mortgage can be a viable choice. By keeping your mortgage payments low, you can allocate funds towards other investments or savings, taking advantage of a stable housing market to maximize your financial strategy.

Advantages of Interest-Only Mortgage

We're going to look at how interest-only loans can benefit borrowers in the next section.

1. Low Level of Monthly Cash Outflow

For Interest-Only Mortgages, the borrower shall only be required to pay monthly payments during the introductory period on the interest portion of the loan.

This means that the full EMI (Equated Monthly Installment) consisting of principal and interest will only be payable after the completion of this initial period.

NOTE

This reduced monthly payment requirement, which can be advantageous for borrowers who are short of funds or wish to use the cash flow to fund additional financial objectives or investments, might lead to a smaller outflow during the initial stages of the mortgage.

2. Increased Savings in the Initial Period

By having lower monthly payments, homebuyers with interest-only mortgages have the advantage of increased cash flow during the introductory period. This surplus of funds can provide greater support in managing monthly expenses and can be utilized for saving purposes.

NOTE

The ability to save more in the initial period can be advantageous for borrowers who want to build up their savings, allocate funds towards emergency reserves, or invest in other important ventures such as education, starting a business, or making other investments.

3. Freedom of Payments

Some interest-only loans allow borrowers to begin making full EMI payments earlier than initially decided. This gives borrowers the freedom to choose when they can afford to start paying the principal amount along with interest.

This arrangement enables the borrower to have more control over their mortgage payments. It adapts them according to their economic situation, regardless of changes in income.

4. Favorable for Young Buyers

Interest-only mortgages can be particularly favorable for young buyers, especially those who have recently entered the workforce and started with a lower salary.

For young professionals who prefer homeownership over renting an apartment, an interest-only loan allows them to manage their cash flow more effectively by deferring the larger principal payments to a later stage when their income is expected to increase.

This can provide a stepping stone into the property market while still having the ability to meet their current financial obligations and gradually build equity in the property over time.

Disadvantages of Interest-Only Mortgage

Like every coin has two sides, the concept of interest-only mortgages also comes with its share of disadvantages and potential drawbacks.

No Equity in the Property

Equity represents ownership of a property and can be used as an asset for future financial endeavors. Interest-only loans enable the borrower to pay interest on a loan that does not include any principal amount.

This means the borrower has built no equity in the mortgaged property over the introductory period. Without building equity, the borrower does not benefit from ownership and cannot accumulate wealth through property appreciation.

Uncertainty of Income

One drawback of an interest-only loan is its dependence on the borrower's capability to make timely principal payments. It may be difficult to fulfill these requirements if the borrower's income is not growing as anticipated.

NOTE

Since the principal payments are often significant and sometimes due in lump sums, the borrower may struggle to fulfill these obligations, potentially leading to financial difficulties or even defaulting on the loan. This could lead to foreclosure.

Fluctuating Interest Rates

The interest rate may be adjusted and updated to align with the current rates as soon as a period passes during which it is necessary to make its primary payment for an interest-only loan.

This adjustment will ensure that the loan can still take into account changing interest rates and reflect current market conditions.

By making this adjustment, the lender can ensure that the borrower's payment structure remains in line with the current interest rate trends, potentially resulting in changes to the overall repayment obligations for the loan.

NOTE

It can be challenging to foresee and budget for loan repayment if interest rates remain uncertain, in particular when they increase significantly. This could make it difficult to afford your mortgage payments.

Unreliable Housing Markets

Housing markets can be volatile and impact your interest-only mortgage. Your home's value could decrease if the housing market continues to decline. It will be difficult to sell your house and pay off the mortgage.

The 2008 crisis is an example of the same.

NOTE

To comply with the larger amount of payments and pay back the loan if necessary, borrowers should carefully estimate their anticipated cash flow over some time. These loans may also increase the risk of default.

Interest-Only Mortgage FAQ

For calculating the monthly payments during the interest-only period:

- Determine the loan amount

- Identify the interest rate

- Determine the loan term

- Calculate the monthly interest payment

Monthly Interest Payment = Loan Amount × Monthly Interest Rate

The monthly interest rate can be found by dividing the annual interest rate by 12

- Calculate the monthly payment:

Monthly Payment = Monthly Interest Payment

For an Interest-Only Mortgage, lenders require various proofs to prove that the prospective borrower is able and will be able to repay the loan.

Some of the things that show that one is, and will be capable of are:

- Adequate Down Payment

- Strong Credit history and Credit score

- Cash reserves

- A consistent flow of income

- Co-borrower / Assurer

However, it is recommended to consult with each lender and select the most suitable deal depending on your needs and conditions, as this list differs from one lender to another.

Many agreements done under Interest-Only Mortgages have the provision to advance the payments for the principal amount. The best thing to do would be to check with the individual mortgage provider about the matter.

The process of refinancing involves acquiring a new loan that replaces your current mortgage. Refinancing can be pursued for various reasons, including adjusting lending conditions, obtaining more favorable interest rates, or altering repayment arrangements.

However, different factors, such as the terms and conditions of an agreement, repayment structure, etc., are likely to determine if a loan can be refinanced.

When seeking guidance on interest-only personalized mortgages and their suitability for your specific situation, it is recommended to seek advice from a mortgage professional or financial advisor.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?