Asymmetric Information

A situation that occurs when one party has more information about a good or service than another in economic exchange.

What Is Asymmetric Information?

Asymmetric Information occurs when one party has more information about a good or service than another in economic exchange. The idea of asymmetric information was developed in the 1970s and 1980s as a potential explanation for market downfall.

This theory proposes that incomplete information between the buyer and the seller can lead to market failure. Market failure is when the buying and selling stuff is not fair, and prices are not set right by the forces of supply and demand.

In any economy, asymmetries of information are always there. They allow people and businesses to become more productive with their chosen specialization. For example, a doctor can have more information about a patient's medical condition than the patient.

However, the doctor's superior medical knowledge was attained through years and years of experience and extensive medical training.

It would simply be impractical for the patient to specialize in the medical field at the cost of any other field. Economies thus benefit from an efficient division of labor and shared knowledge.

Another example of asymmetric information can be the market for used cars. So, in used car markets, we can buy second-hand cars, some of which are of bad quality. Let us call the bad quality cars 'Lemon.'

In the market for used cars, the person selling the car usually knows more about it than the person buying it.

This places the buyer of the car in a bad position because he needs to know what he is entering into. He might buy a car accident or a faulty car, and when he gets to know that he might sell the car to some other person, therefore, the lemon gets transferred,

Now, if that happens on a big scale, it will create a problem of lemons because there will be more lemons in the market, i.e., bad quality goods in the market.

- Asymmetric information happens when one party has more information than the other, leading to suboptimal decisions and market inefficiencies.

- Adverse selection is a problem arising from asymmetric information where one party selectively participates in transactions based on their knowledge, often leading to negative outcomes.

- Common examples include situations in insurance, where the policyholder knows more about their health than the insurer, and in used car sales, where the seller knows more about the car’s condition than the buyer.

- Governments and regulatory bodies may intervene to reduce the effects of asymmetric information by implementing disclosure requirements, transparency standards, and consumer protection laws.

Asymmetric Information: Adverse Selection and Moral Hazard

AI can lead to the problem of adverse selection and moral hazard. Let's begin exploring each of these topics in more detail.

Adverse Selection

Adverse selection means one of the two parties, either buyer or seller, has more complete or different information than the other before they reach an agreement. This puts the less knowledgeable party at a disadvantage as it is difficult for them to value or assess the risk of the deal.

Meanwhile, the more knowledgeable party has all the necessary information and, therefore, can evaluate the value of the deal with more accuracy. But, unfortunately, this ultimately leads to poor quality decisions and lower quality goods and services in the market.

An example can be in the case of health insurance agreements. The buyer of the insurance has more information than the seller.

Moral Hazard

A moral hazard occurs when there is asymmetric information between the buyer and the seller and a change in behavior after the deal. This means that a party (usually the buyer) accepts the deal to change the behavior after the deal.

This puts the less knowledgeable party, usually the seller, at a disadvantageous position because they are usually the ones who have to face negative consequences.

For instance, let's say someone purchases insurance for their motorbike but then deliberately rides it recklessly to get money from the insurance company.

The insurance company is in the bad light here because they would not have sold the insurance if they knew.

Asymmetric Information And Lemons Problem

Generally, firms have a better quality of their products than the general public. Here, the buyers who represent us would be suspicious about the quality of the product.

Due to imperfect competition, low-quality products are sold in the market compared to high-quality products.

As a result, high-quality products in the market will remain the same. George Akalof first analyzed the implication of imperfect competition regarding product quality. This phenomenon is called 'Lemons Problem.'

Lemon Problem in the Stock & Bond Market

A potential investor cannot differentiate between good firms with high expected profits and low risk and bad firms with less expected and high risk. In this situation, the investor will be willing to pay the price reflecting the average quality of firms issuing securities.

Thus, the price lies between the value of the securities of bad and good firms.

If owners or managers of a firm know that their firm is good, then they won't be willing to sell their securities at a price the buyer is ready to buy because they know that their securities are undervalued.

The only firms willing to sell will be bad firms (because their securities price is higher than what they are worth). Therefore, the potential investor does not want to hold bad securities and will decide not to invest in the market.

This analysis is similar if an investor considers purchasing a corporate debt instrument in the bond market rather than an equity share market.

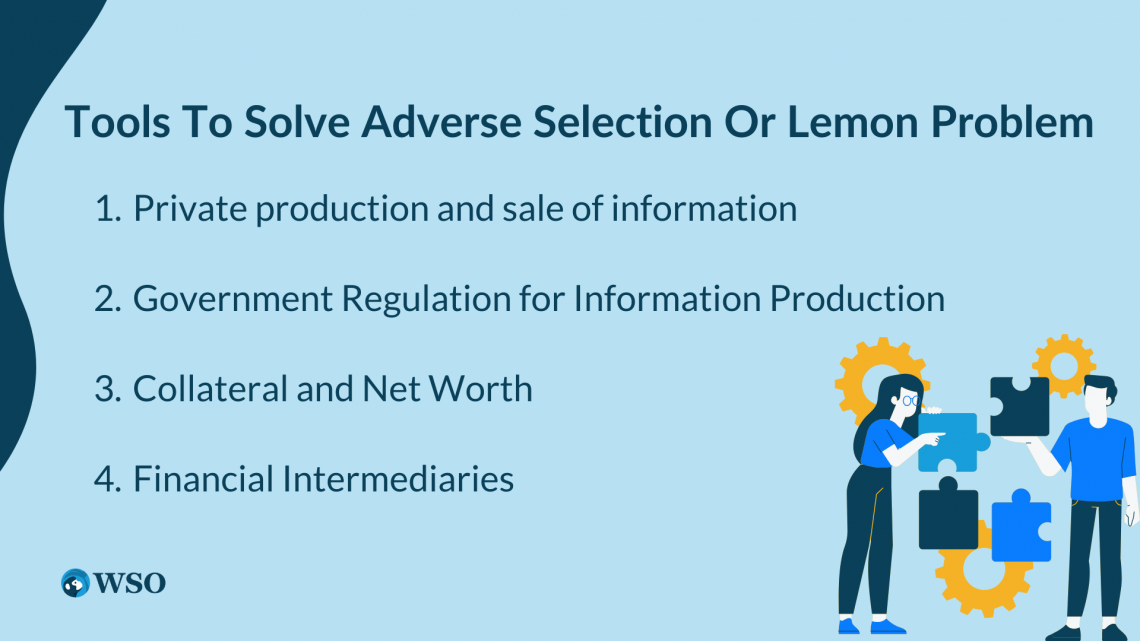

Tools to solve adverse selection or lemon problem

Various tools are available to us for solving the problem of adverse selection or lemon problem. These tools are explained below

Private Production and Sale of Information

To eliminate adverse selection, information must be made available to the investors. This could be achieved through private firms or institutions providing the information for a service fee.

Stock analysis firms use the data from reports of companies and furnish them to investors. There are many rating companies in India, namely CRISIL, ICRA, CARE, etc. However, more is needed to solve the problem completely as it results in another problem. The problem of 'Free Rider.'

The free rider problem occurs when people who do not pay for the information take advantage of the information that others pay for. Free riding by other investors significantly reduces the gains from the private purchase of information.

Government Regulation for Information Production

When profits from privately arranged information get reduced due to free riding, customers prefer to avoid buying the information, leading to a fall in the firms' business.

A solution, then, is the introduction of the government as a producer of information, where it releases the data on behalf of companies for the investors.

The government could produce the information to help the investors distinguish between Good form and bad form and provide it to the public free of cost.

Investors can determine how good or bad the firms are. Even with the heavy regulation, the problem of adverse selection still exists. Because companies and firms still have greater information than investors.

Collateral and Net Worth

Adverse selection occurs if a lender suffers a loss when a borrower cannot pay for loans, and thereby there is a default of the lender.

Collateral (property promised to the lender if the borrower defaults) reduces the consequences of adverse selection because it reduces the lender's loss even in case of default.

Collateral acts as an incentive for both lenders and borrowers. The lender becomes more willing to give collateralized loans, and borrowers, too, get an assurance to receive the loan at a lesser interest rate.

Note

Net Worth is the difference between a company's assets and liabilities. It also performs a similar role as collateral.

If a firm has a high net worth, then if it engages in an investment that causes it to have negative profit (loss) and so default on its debt payments, the lender can make a claim against the firm's net worth and take little of the firm's net worth and recover their losses.

The higher the net worth a firm has, the less likely it is to default because they have more assets to pay for their liabilities.

Financial Intermediaries

A financial intermediary, such as a bank or Mutual Fund Company, is an expert in producing information about firms so that they can distinguish between good firms and bad firms.

Then it can acquire funds from depositors and lend to good firms because a bank can lend loans to credible people and pay less interest rate to depositors than it charges from the loan takers.

The resulting profits that the bank earns give its incentive to engage in this information production activity.

Asymmetric Information: Moral Hazard in equity contract

In most companies, owners (Principals) cannot monitor everything managers (Agents) do. As a result, managers have more information about the performance of the firms than owners. This imperfect information creates a principal-agent problem.

The problem is that managers may pursue their own goals (like their salaries, tenure, reputation, etc.) even at the cost of the company's profit.

Equity holders/ Shareholders are the company's owners but are still challenged by the Principal agent problem. The shareholders are the principal owners of the business, as they hold the ownership in the form of equity.

Appointed managers are the company's agents who act on their principals' behalf. In this structure of an organization, where owners are different from controllers, this leads to the problem of moral hazard.

The managers lack the incentives to act on behalf of their owners or shareholders and have substantial opportunities to work for personal gains.

Example

Let's understand with an example:

B is looking to invest in a new business opportunity offered by his friend A. Himself invests 25,000 as a 10% equity of the business, and he offers B 90% of the shareholding instead of 845,000.

A manages everything and gets a salary of 25000 for his work.

When the Company earns profit, both people distribute the profit in a 90:10 ratio after the salary deduction. And Still, A gets very little share than B.

Here the problem starts. Now A started enjoying the money B, he established a lavish office, relaxed on B's money, and avoided the hassle of fieldwork. It causes loss for the company because A has started doing Moral Hazard Activities here and wants to maximize his gains.

Tools to solve moral hazard in equity contracts

In this section of the article, we shall be looking at the tools that can be used to solve the moral hazard problem in equity contracts.

Private Production of Information or Costly State Verification

Shareholders can try to arrange for information regarding fund utilization and monitor management actions through Audit. The problem is that the monitoring process can be expensive in terms of money and time; that's why it is called costly state verification.

Another issue here is Free Ridership. Other shareholders can take advantage of the information you paid. In such a case, people will not pay for the information and avoid participation.

Government Regulation

Government Regulations (Like the Companies Act 2013 etc.) stop managers and corporates from misusing their power to manipulate funds. Govt. makes accounting standards for firms to stop such manipulation, fraud, etc.

Govt. also passes laws to impose criminal penalties on people who commit fraud by stealing or hiding profits. But after all this, people commit financial frauds like Harshad Mehta Scam, Yes bank Scam, etc.

Financial Intermediaries

A financial intermediary reduces the problem of moral hazard by arranging the information and avoiding free ridership.

A venture capital firm eliminates the problem of moral hazard by pooling funds arranged from several small investors and investing them in the funds directly.

Venture Capitalists insist the firm include its members as part of the board of managers or directors.

With such a system, they secure the interest of the shareholders and investors and prevent the managers from diverging and engaging in malpractices/frauds.

Debt Contract

Equity contracts don't guarantee returns since the companies can decide when to pay the returns out of profits. In case of losses, the firms easily escape this burden. Debt contract offers regular returns on investment irrespective of the firm's performance.

Debt holders are least concerned about the company's activities as long as they receive their payments and only interfere when such payments are hampered.

Debt Contracts require less monitoring and provide claims to the company's assets in the event of failure.

Researched and Authored by Garv Mittal | LinkedIn

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?