Compilation Engagement

A service provided by accountants or accounting firms where they take client-provided financial information and create financial statements.

What Is A Compilation Engagement?

A compilation engagement is a type of service provided by an accountant or accounting firm in which the accountant takes the financial information provided by a client and compiles it into a set of financial statements.

These statements might include a balance sheet, income statement, and statement of cash flows. The accountant does not perform any assurance procedures or express any opinion on the financial statements; rather, they simply present the information in a prescribed format.

An engagement is a professional service in which a certified public accountant (CPA) prepares financial statements for a business or organization based on the client's records.

The CPA does not provide any assurance on the information presented in the financial statements and does not perform any testing or verification of the underlying data.

These engagements are typically less time-consuming and costly than audit or review engagements. They are often used by small businesses and organizations that do not need or cannot afford the more extensive services of an audit or review.

Financial statements prepared as part of an engagement are generally intended for use by management and stakeholders rather than third parties.

- A compilation engagement is a type of service provided by accountants where they compile financial statements from client-provided data without offering any assurance on the accuracy or completeness of the information.

- The primary objective is to organize financial information into a professional format that adheres to accounting standards, making it easier for stakeholders to understand the company’s financial position.

- Unlike audits or reviews, compilation engagements do not involve verifying the financial data through testing or analysis. The accountant relies solely on the information provided by the client.

- These engagements are often used by small businesses or organizations that need formal financial statements for internal purposes, loan applications, or regulatory requirements but do not require a full audit.

Purpose of compilation engagements

One of the main purposes of an engagement is to provide a business or organization with financial statements used for various purposes, such as obtaining financing, making business decisions, or satisfying reporting requirements.

Small businesses or organizations that do not need or cannot afford the more in-depth assurance services provided by an audit or review often use Engagements.

Engagements are generally less expensive and quicker to complete than audit or review engagements, as they do not involve testing of the underlying transactions or procedures.

They may be suitable for small entities that do not require or cannot afford the level of assurance provided by an audit or review engagement.

However, these engagements provide limited assurance on the financial statements and may not be acceptable to third parties, such as banks, investors, or regulators.

Differences between compilation, audit, and review engagements

Professional standards, International Standards on Auditing (ISAs), and the International Standard on Review Engagements (ISREs) define the differences between compilation, audit, and review engagements.

These standards set out the requirements for each type of engagement, including the level of assurance provided, the scope of work performed, and the requirements for independence and professional skepticism.

An audit engagement is the most extensive in scope and involves the accountant performing extensive procedures to express an opinion on the fairness of the financial statements.

A review engagement is less extensive in scope than an audit but involves some limited assurance procedures. On the other hand, it consists of no assurance procedures at all.

NOTE

A compilation engagement is less in-depth than an audit engagement.

| Parameters | Compilation Engagement | Audit Engagement | Review Engagement |

|---|---|---|---|

| Level of assurance | Provides limited assurance on the financial statements. | Provides the highest level of assurance on the financial statements. | Provides a moderate level of assurance on the financial statements. |

| Independence | An accountant is not independent of the entity. | The accountant is independent of the entity. | The accountant is independent of the entity. |

| Scope of work | Limited to preparing the financial statements following the applicable financial reporting framework. | Includes testing of the underlying transactions and procedures and an evaluation of the overall financial statement presentation. | Includes procedures to obtain limited assurance on the financial statements, such as inquiries of management and analytical procedures. |

| Professional skepticism | No assurance of opinion is expressed. | An assurance opinion is expressed. | An assurance opinion is expressed. |

Who might use Compilation engagements?

Small businesses and organizations with limited resources are often the primary users. These entities may not have the need or the budget for the more extensive services provided by an audit or review engagement.

Engagements are often less costly than other assurance services, making them attractive for entities with limited resources. Additionally, because a CPA is not providing any assurance on the financial statements, the process is generally less time-consuming.

It does not provide the same level of assurance as audits or reviews, and the financial statements prepared as part of it are generally intended for use by management and stakeholders rather than third parties.

However, even larger businesses or organizations may use it for specific purposes, such as preparing financial statements for a specific purpose (e.g., obtaining financing) or for internal use only.

In summary, it can be a good option for entities that need financial statements for internal use, tax purposes, or lender or other regulatory compliance but do not need or can not afford an audit or review.

NOTE

The statements indicate the company's performance and financial positions but a lower level of assurance than other types of engagements.

Process Of A Compilation Engagement

The process of a compilation engagement typically involves the following steps:

- Engagement letter: The accountant and the entity enter an engagement letter, which outlines the terms of the engagement and the responsibilities of both parties.

- Understanding the entity: The accountant gains an understanding of the entity's business, its operations, and its financial reporting framework.

- Review of accounting records: The accountant reviews the entity's accounting records, such as invoices, receipts, and bank statements, to ensure that the financial statements are complete and accurate.

- Preparing financial statements: The accountant prepares the financial statements per the applicable financial reporting framework.

- Review and approval: The accountant reviews the financial statements with the entity's management and obtains their approval before finalizing them.

- Communication with management: The accountant communicates with management to obtain the necessary information and explanations for preparing the financial statements.

- Report to management: The accountant issues a report to management stating that the financial statements have been prepared following the applicable financial reporting framework.

NOTE

The above list is not exhaustive, and the exact steps involved in an engagement may vary depending on the specific circumstances of the engagement.

Advantages & Disadvantages Of Compilation Engagement

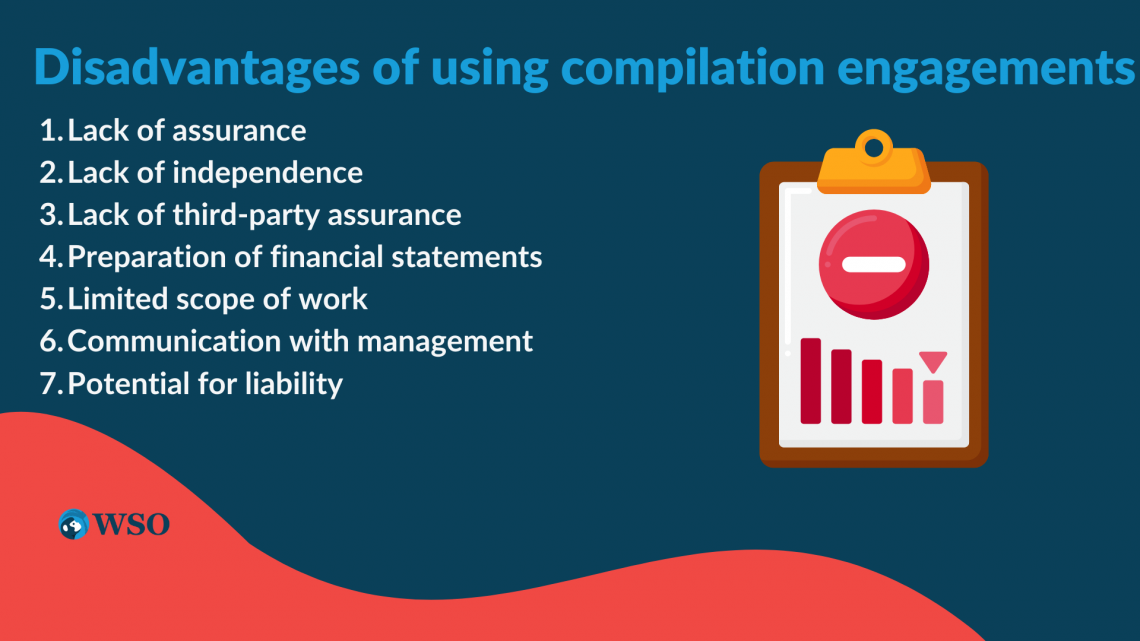

The potential disadvantages of using compilation engagements involve the following:

- Lack of assurance: As mentioned, engagements do not provide any assurance about the reliability or accuracy of financial statements. It can be a disadvantage if the financial statements are being used for a purpose requiring some assurance.

- Lack of independence: The accountant is not independent of the entity whose financial statements are being compiled. The accountant may have a financial interest in the entity or a close relationship with it or its management.

- Lack of third-party assurance: Because engagements do not assure the financial statements, they may not be acceptable to third parties, such as banks, investors, or regulators.

- Limited scope of work: The scope of work is generally limited to preparing financial statements following the applicable financial reporting framework.

- Potential for liability: Although the accountant does not express an opinion on the financial statements, there is potential for the accountant to be held liable for any errors or omissions in the financial statements.

The advantages of using compilation engagement are

- Cost: Engagements are generally less expensive than audit or review engagements, making them a cost-effective option for businesses or organizations with limited resources.

- Ease of use: Engagements are generally less complex and time-consuming than audit or review engagements, making them a more straightforward option for businesses or organizations with limited accounting expertise.

- Flexibility: Engagements offer more flexibility than audit or review engagements, as the accountant is not required to follow specific procedures or standards. It allows the accountant to tailor the engagement to the client's needs.

- Time: Engagements are generally quicker to complete than audit or review engagements, as they do not involve testing of the underlying transactions or procedures.

- Suitable for small entities: These engagements may be suitable for small entities that do not require or cannot afford the level of assurance provided by an audit or review engagement.

Best practices for selecting an accountant or accounting firm for a compilation engagement

When looking for an accountant or accounting firm to handle this engagement, it's crucial to keep certain things in mind.

To make the best decision, consider the following best practices:

- Expertise and Experience: Ensure the accountant or firm has the appropriate expertise and experience. It can be complex, and working with an accountant who understands financial statements and how to present them in a prescribed format is essential.

- Reputation: Consider the accountant's or firm's reputation. You want to work with an accountant or firm with a good reputation in the industry and is known for producing high-quality work.

- Responsiveness and Communication: Look for an accountant or firm that is responsive and communicative. You'll want to work with an accountant who is responsive to your needs and willing to answer your questions and concerns.

- Fees: Consider the fees charged by the accountant or firm. They are generally less expensive than audit or review engagements, but it's still essential to get a sense of the fees that will be charged and whether they are reasonable.

Common pitfalls to avoid In A Compilation Engagement

Compilation engagements can be complex, and it's important to be aware of potential pitfalls that can arise.

The common pitfalls to avoid.

1. Not considering the company's specific needs and requirements.

It's essential to consider the specific needs and requirements of the company when choosing an accountant or firm for the compilation engagement. This will ensure that the engagement is tailored to the company's specific needs and that the resulting financial statements are useful and relevant.

2. Not properly reviewing the compiled financial statements.

It's important to properly review the compiled financial statements for accuracy and completeness before issuing them. Failure to do so could result in errors or inaccuracies in the statements.

3. Failing to provide complete and accurate financial information.

It's important to provide the accountant with complete and accurate financial information, as any errors or omissions could affect the integrity of the compiled financial statements.

4. Not fully understanding the limitations.

It's important to be aware that it does not provide any assurance about the reliability or accuracy of the financial statements. Users of the financial statements should be aware of the limitations.

5. Not communicating effectively with the accountant.

It's important to communicate effectively with the accountant to ensure that it is completed to your satisfaction. Be sure to ask questions and clarify any issues that arise.

Alternatives to compilation engagements

The alternatives to compilation engagements that businesses and organizations might consider, depending on their specific needs and circumstances.

These alternatives include the following.

Self-preparation of Financial Statements

Some businesses or organizations may choose to prepare their financial statements using in-house accounting staff or with the assistance of accounting software.

It can be a cost-effective option but requires a certain level of accounting expertise and can be time-consuming.

Review or Audit Engagements

For businesses or organizations that require a higher level of assurance about the reliability and accuracy of their financial statements, a review or audit engagement may be a better option.

These engagements involve more extensive procedures and provide a higher level of assurance, but they are also generally more expensive and time-consuming.

Other Types of Assurance Services

In addition to review and audit engagements, there are other assurance services that businesses and organizations might consider, such as agreed-upon procedures or internal audit services.

These services can provide a tailored level of assurance depending on the client's specific needs.

Current Trends and Developments

A few of the current trends or developments in the field of these engagements that businesses and organizations should be aware of:

- Increased focus on technology: Many accountants and accounting firms now use technology, such as cloud-based accounting software, to streamline the compilation process. It can help reduce the time and cost of an engagement and improve efficiency.

- Changes to professional standards: The accounting profession is constantly evolving, and changes to professional standards can impact how engagements are performed. It's important to keep up to date with these changes to ensure that engagements are completed following the latest standards.

- Use of cloud-based solutions: More and more companies are using cloud-based solutions for financial data management. This allows for easy accessibility of financial data from any location and collaboration between different parties.

- Tailoring engagements to specific needs: Companies are increasingly looking for accountants and firms that can tailor compilation engagements to their specific needs and requirements.

- Increased competition: The accounting profession is becoming more competitive, and businesses and organizations may have more options when selecting an accountant or accounting firm for an engagement. It's important to shop around and compare the offerings of different firms to find the best fit for your needs.

Tools Used in a Compilation Engagement by an Accountant

The accountant is responsible for presenting financial information in a prescribed format and providing basic information about the company's financial performance.

To achieve this, the accountant typically uses a variety of tools. These tools include

- Financial statement preparation software: The software prepares financial statements following the applicable financial reporting framework.

- Accounting records: The accountant may review the entity's accounting records, such as invoices, receipts, and bank statements, to ensure that the financial statements are complete and accurate.

- Questions and inquiries: The accountant may ask questions of the entity's management and review relevant documentation to understand the entity's business and financial position.

- Analytical procedures: The accountant may perform analytical procedures, such as comparing the entity's financial performance to prior periods or industry benchmarks, to identify any unusual trends or discrepancies.

- Professional judgment: The accountant uses their professional judgment to interpret the applicable financial reporting framework and determine the appropriate financial statement presentation.

- Cybersecurity measures: It plays a crucial role in engagements to ensure the safety and confidentiality of sensitive financial information.

- Encryption is one of the key measures accountants use to protect financial information stored on their systems and communications between the accountant and the company.

This helps to prevent unauthorized access to the information. Additionally, accountants use secure communication channels, such as virtual private networks (VPNs) and secure file-sharing platforms, to transmit and share financial information.

Researched and authored by Ashish Singh | LinkedIn

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?