Statement of Cash Flows

One of the three main financial statements that tracks all of the cash and cash equivalents flowing into and out of a business over a period of time

What is the Statement of Cash Flows?

The cash flow statement (CFS) is one of the three main financial statements, and it tracks all of the cash and cash equivalents flowing into and out of business over a period of time.

The CFS is arguably the most important of the three main financial statements for two reasons. First, these flows are an important indicator of financial health. Second, the CFS links the income statement and the balance sheet and can be used to recreate both.

Public companies typically follow two types of accounting methods: accrual and cash. The income statement relies on the accrual accounting method, so profits do not necessarily reflect cash coming in.

On the other hand, the statement uses the cash accounting method, which more accurately depicts when cash enters the business.

The difference in accounting methods used on these two statements means that profitable companies may not adequately manage their cash position, which is why the CFS is such an important tool for investors.

- The cash flow statement (CFS) is a crucial financial statement that tracks the flow of cash and cash equivalents into and out of a business over a specific period.

- The CFS is considered the most important among the three main financial statements because it provides insights into a company's financial health and links the income statement and balance sheet.

- There are three types of cash flows tracked in the CFS: cash flow from operating activities, cash flow from investing activities, and cash flow from financing activities.

- Cash flow from operating activities reflects the cash generated or used in a company's primary revenue-producing activities and indicates its operational efficiency and liquidity.

- The presentation of cash flow from operations can be done through the direct method (listing cash receipts) or the indirect method (reconciling net income with cash flows). The indirect method is more commonly used.

Three Types of Cash Flow

The CFS tracks the three types of cash flow: CF from operations, CF from investing, and CF from financing.

1. CF from Operating Activities

Operating cash flow comes from the firm's primary revenue-producing activities. It is the money the firm earns and spends from conducting its day-to-day business, which results in changes to its operating assets.

This first line item of the statement is net income, which is the final line on the income statement.

Then, non-cash operating assets and liabilities are either added back or subtracted to reconcile net income to net cash from operating activities.

Finally, changes in operating assets and liabilities are accounted for.

2. CF from Investing Activities

This section of the CFS reflects changes in capital expenditures (CapEx) and long-term assets. Investing flows result from purchasing and selling property, plant, and equipment (PP&E), other non-current assets, and financial assets.

3. CF from Financing Activities

Financing cash flow is the cash the firm receives and gives in the form of external financing. It is the flow between a company and its creditors and shareholders, resulting in changes to the firm's capital structure (debt vs. equity).

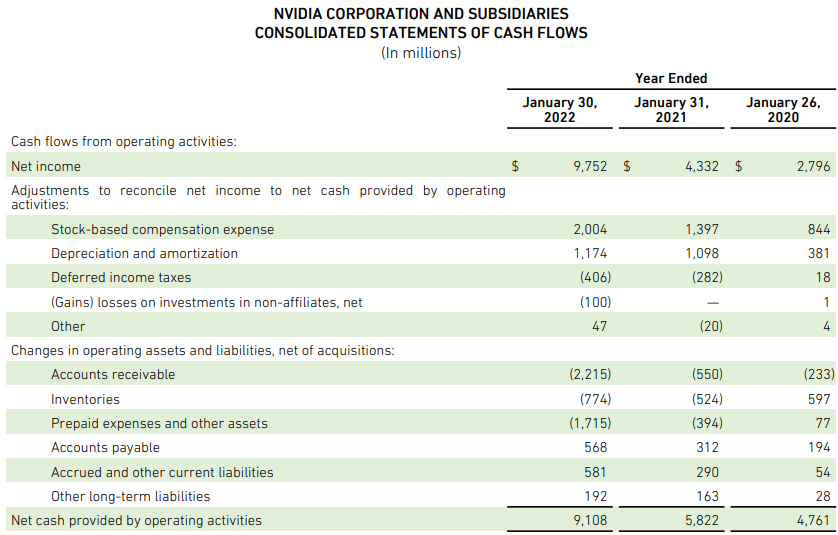

Below is an example of a real CFS pulled from Nvidia Corp's annual 10-K filing. Here, it is plain to see the breakdown of the flows into operating, investing, and financing activities. Let's walk through the CFS step by step.

Net Cash Provided by Operating Activities

This is the first section of the statement, and it is an important benchmark in determining how successful a business's core activities are. A company's net cash flow from operating activities indicates if any additional cash came or left the business.

Since this type of CF directly affects a company's liquidity, business owners and investors look at this section to determine how money moves into and out of a company to get a picture of operational efficiency.

Examining these flows from operating activities helps owners make informed decisions to maintain sufficient cash for operational efficiency and other needs. In other words, it helps them make smart financial decisions.

Positive and growing flow from operating activities indicates that the company’s core business activities are doing well. It provides an additional measure of a company’s profitability potential, in addition to the traditional indicators like net income, EBITDA, ROI, and ROE.

Unlike metrics like EBITDA, ROI, and ROE, net cash flow from operating activities is not an appropriate mode of comparison, even for companies in the same industry, as firms with different businesses will likely have a few somewhat unique drivers of CF.

As such, CF from operations is better suited to examining a firm’s historical performance.

Direct vs. Indirect Presentation

There are two widely recognized methods of presenting CF from operations: direct and indirect.

The direct presentation method lists cash receipts, which are added together to arrive at operating cash flow. The indirect method, which is more popular, begins with net income, and CFs are presented as reconciliations from profit to cash flow.

In the indirect presentation method, the CFS is linked to the income statement by calculating the flows from net income and reconciling Depreciation and Amortization expenses.

1. Net Income

This is the final line on the income statement, and it is the basis from which all cash flows are calculated using the indirect method. Net income is calculated by subtracting COGS and total expenses from total revenue.

2. Reconciliation of Non-Cash Accounts

The declining value of long-term assets appears on the income statement as D&A expenses. But because they are a non-cash expense, they are added back. The same goes for stock-based compensation, deferred taxes, and other non-cash accounts.

3. Operating Assets and Liabilities

After all non-cash accounts have been reconciled, it is time to account for changes in operating assets and liabilities, which is where operating CF comes from. These are accounts that change due to the business’s operating activities.

Based on the example above, it is clear that Nvidia uses the indirect presentation method.

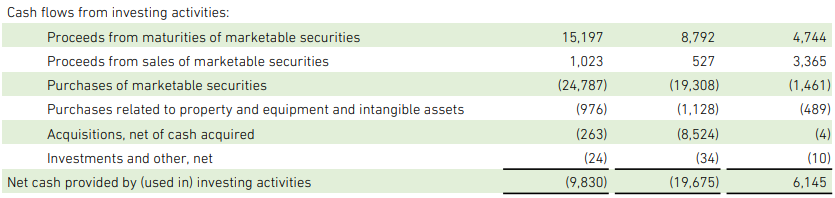

Net Cash Provided by Investing Activities

Like CF from operations links the CFS to the income statement, CF from investing links it to the balance sheet.

This section involves long-term uses of cash. Accordingly, any changes to a company’s cash position involving non-current assets, investments, or equipment would be included in this section.

1. Financial Assets

We know that “marketable securities” (equity in another company) have nothing to do with Nvidia’s core business operations. Therefore, those items cannot be operating assets and must be investment accounts.

2. Capital Expenditures

The next line item under cash flow from investing activities is “purchases related to [PP&E] and intangible assets,” which is CapEx.

3. Acquisitions

The following line item, categorized as “Acquisitions, net of cash acquired” includes all cash Nvidia made in acquiring other companies, categorized as a non-current asset account.

Because this section deals with long-term uses of cash, many of the flows listed tend to be negative. Nvidia’s CFS lists net cash provided by investing activities as negative in 2021 and 2022. In the long run, however, these investments tend to pay off.

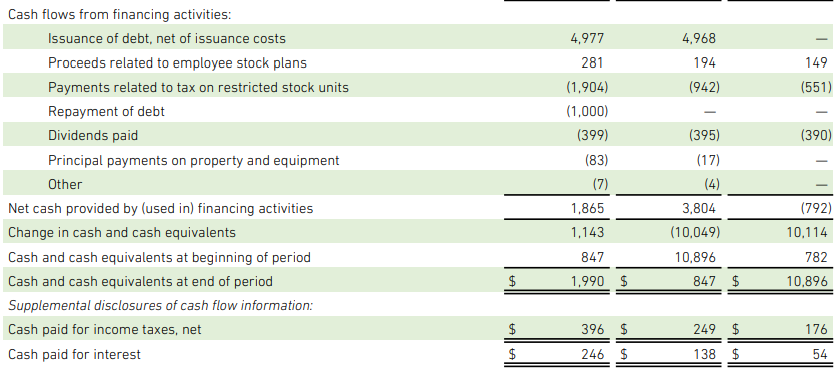

Net Cash Provided by Financing Activities

This section lists all cash flows that are used to fund a company. In addition, these activities include all transactions that alter a company’s capital structure.

-

All line items under this section an of Nvidia’s capital structure.

-

Dividend payments reduce the “dividends payable” account on a firm’s balance sheet, which decreases the firm’s liabilities and lowers the firm’s debt-to-equity ratio.

This section of the CFS will look very different for companies with different business models.

For example, Amazon tends to rely more on debt than other companies would be comfortable with. But a high debt ratio works for Amazon; because they are in the volume business, they turn over their receivables very quickly and can cover their large debt.

Examining a business’s capital structure is extremely important for investors because a firm’s blend of debt and equity financing could significantly impact its valuation. Check out this link for more information on how capital structure affects business valuation.

To round out the CFS, the values of all sections are added to find the change in cash and cash equivalents (∆CCE) for the period.

∆CCE is then added to CCE at the beginning of the period to find the total amount of CCE at the end of the period.

If you’re interested in a career in finance and accounting, check out our course on Financial Statement modeling.

Statement of Cash Flows FAQs

It is the amount of money that comes into and leaves a company.

A company’s cash balance is the amount of cash it has on hand. The cash balance is an indicator of a firm’s ability to pay off its short-term debts.

Cash equivalents are highly liquid assets. In other words, they can quickly be converted into cash. Treasury bills, money market holdings, and commercial paper are examples of cash equivalents.

While receivables and liquid securities (stocks, bonds, derivatives) are very liquid and are sometimes considered “near-cash” when calculating ratios, they are not cash equivalents.

Profit indicates the amount of money left over after expenses have been paid, but they do not represent CF because profits can be recorded before the money flows into the company.

CF, on the other hand, measures the exact amount of cash that enters or leaves the company.

For example, if a law firm were to provide legal services, their accounts receivable would increase. When RED accounts are closed at the end of the period, that amount would be recorded as profit.

However, payment would not be reflected on the CFS until the money comes in.

FCF is the amount of cash a firm has left over after paying operating expenses and CapEx. FCF can be calculated using operating CF or total sales revenue:

FCF = Operating Cash Flow - CapEx

or

FCF = Revenue - (Operating Costs + Taxes) - Required Investments in Operating Capital

Investors can use FCF to determine whether a company has enough leftover cash to pay dividends.

or Want to Sign up with your social account?