Current Assets

Learn what current assets are, how they work, and why they matter for a company’s liquidity. Explore examples, key ratios, and the differences between current and non-current assets in this in-depth guide.

What are Current Assets?

Current assets are assets expected to be used, sold, or converted into cash within one year or within the operating cycle, whichever is longer.

This distinction exists because current liabilities must be repaid within a short period, and cash from current assets is typically used to settle these obligations.

Current assets include cash, cash equivalents, marketable securities, accounts receivable, inventory, prepaid expenses, and other current assets.

Key Takeaways

- Current assets are very liquid and can quickly generate cash to pay off the outstanding current liabilities.

- These assets include cash, cash equivalents, marketable securities, accounts receivable, inventory, prepaid expenses, and other current assets.

- In contrast to the non-current assets, cash from current assets is expected to be received within one year.

- The current and acid test ratios are used to measure a company's liquidity and assess its ability to pay off current liabilities using current assets.

Types of Current Assets

Now that you understand what current assets are, let's delve deeper into their different components.

The accounts are presented in order of liquidity, the order in which they can be converted into cash. The shorter the conversion time, the earlier an item is on the balance sheet.

Different businesses list their current assets items differently because their nature slightly differs with each company.

Cash

Cash refers to the actual physical or liquid money a company possesses, including funds in bank accounts or on hand. The components of cash flow—operating, investing, and financing—show how cash is generated or used.

Operating cash is the money the firm generates from its operations, while investing activities are the cash spent on investing in property, plant, equipment, and investments, including the cash received from selling investments or assets.

Finally, the cash from financing activities flows in and out when the investors invest in the company or the company raises debt.

Cash is the most liquid asset because you don't have to convert it; it is instantly available.

Cash Equivalents

Cash equivalents are highly liquid investments with an original maturity of 90 days or less, such as Treasury bills or commercial paper.

Two examples of cash equivalents are treasury bills, which the U.S. government issues, and commercial papers, which are loans issued from corporation to corporation with an average maturity of 30 days.

Marketable Securities

Marketable securities are also investments that are very similar to cash equivalents. Still, they are expected to be held for up to one year instead of 90 days.

Examples include trading securities, which are actively traded, and available-for-sale securities, which may be sold before maturity. Held-to-maturity securities are generally classified as non-current assets unless they mature within a year.

Lastly, the securities available for sale are somewhere in the middle. They are expected to be held until they mature and sold if the company decides to do so.

Accounts Receivable

Accounts receivable is an item that shows how much the company is expected to collect in the future.

When a company sells goods or services, it can instantly collect the cash from the customer or sell on credit and wait until the customer pays, on average, within 30 to 90 days.

The expected cash from credit sales is recorded under accounts receivable, and when the payment is received, the accounts receivable balance decreases, and cash increases.

Inventory

Inventory is the goods maintained by the company and expected to be sold to the customers.

When the product is sold, the inventory decreases, representing the sale of an item and the cash generated from the sale. Inventory liquidity refers to the ease with which inventory can be converted into cash through sales.

The average collection period for inventory is very similar to accounts receivable, but usually slightly longer.

Prepaid Expenses

Prepaid expenses occur when a firm pays in advance for a product or service but doesn't immediately receive its benefits.

As time goes by, the firm will start reducing an item and also recognize the expense on an income statement to show that it is paying for the benefits it is receiving.

Other Current Assets

Other current assets are items expected to be converted into cash within one year but are less common or company-specific.

Other current assets include advances paid to employees or suppliers, restricted cash or investments, and assets that are being sold.

How Do Investors Use Current Assets?

Usually, current assets determine the probability that the company can quickly convert its current assets into cash and then pay off its outstanding current liabilities within one year.

When current assets go up, it implies that more funds can be quickly acquired. Conversely, less cash can be acquired if current assets are going down.

Investors calculate liquidity ratios based on current assets and compare them to industry peers to evaluate the company’s short-term financial health and investment potential.

Additionally, a higher level of current assets often indicates that a company has a strong buffer to manage unexpected expenses or financial downturns. This liquidity cushion can be crucial for maintaining operational stability and avoiding the need for costly emergency financing.

Moreover, the composition of current assets is also important. For instance, a company with a high proportion of cash and cash equivalents is generally seen as more liquid than one with a large inventory.

Financial Ratios That Use Current Assets

Three ratios can be used to figure out how likely the firm is to satisfy its short-term obligations.

One is the current ratio. To calculate, we use:

Current ratio = Current Assets / Current Liabilities

Another is the acid test ratio (quick ratio). The formula is:

Acid test ratio (quick ratio) = ((Cash + Cash equivalents + Marketable securities + Accounts receivables) / Current liabilities)

The acid test ratio is similar to the current ratio. The only difference is that it is more conservative by including the items that can be converted into cash more instantly.

The last ratio is the cash ratio, which can be calculated by using:

Cash Ratio = (Cash + Cash Equivalents) / Current Liabilities

The ratio measures the extreme form of liquidity. It shows the company's ability to pay off outstanding current liabilities without any need for conversion into cash.

Example of Current Assets

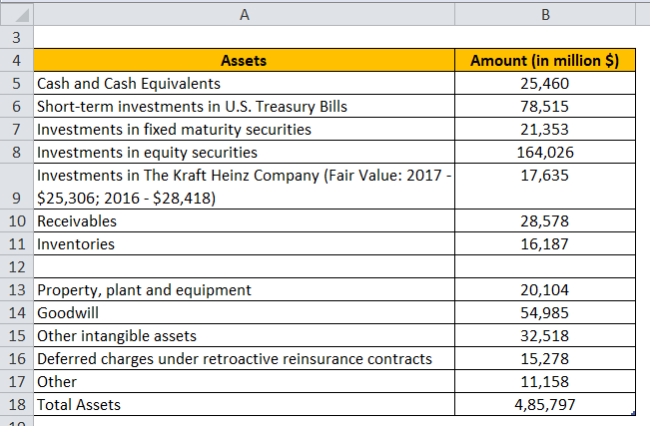

Now, let's look at an example of current assets in an actual company.

First, looking at the picture, we see that all current assets are at the top of the assets section.

One line separates them from the long-term assets grouped at the bottom.

Current assets typically include the most liquid assets—cash and cash equivalents—followed by marketable securities such as short-term investments in treasury bills, fixed-maturity securities, and, in some cases, equity securities.

The last two items included in the current assets are the accounts receivables, followed by inventories.

Now, let's see how the current assets can be used when calculating the ratios

Total Current Assets are:

- Adding up all items: $351,754 million

- Cash and Cash Equivalents: $25,460

- Short-term investments in the U.S. Treasury Bills: $78,515

- Investments in fixed maturity securities: $21,353

- Investments in equity securities: $164,026

- Investments in The Kraft Heinz Company: $17,635

- Receivables: $28,578

- Inventories: $16,187

Now, when Current Liabilities = $200,000 million

- Current Ratio: 1.76

- Current Assets / Current Liabilities

- Acid Test Ratio: 1.68

- (Cash + Short Term Investments + Receivables) / Current Liabilities

The ratios being well above 1 imply that the firm’s chance of paying off current liabilities using the current assets is high.

When Current Liabilities = $600,000 million

- Current Ratio: 0.59

- Current Assets / Current Liabilities

- Acid Test Ratio: 0.56

- (Cash + Short Term Investments + Receivables) / Current Liabilities

The ratios being less than 1 imply that the firm has a smaller chance of paying off the outstanding current liabilities using the current assets.

Current Assets vs. Non-Current Assets

Current assets can be converted into cash within one year and are typically used to pay off outstanding short-term liabilities due within that period.

On the other hand, non-current assets are those expected to provide benefits to the company over more than one year. For example, buildings, equipment, or land will all benefit a company for many years, potentially dozens of years.

Let’s understand the difference in the table below:

| Operator | Current Assets | Non-Current Assets |

|---|---|---|

| Liquidity | Can be converted into cash within one year | The cash is expected to be collected in more than a year |

| Use | Can be used in operations and pay off current outstanding liabilities due to high liquidity | Are expected to be used by and benefit the company in the long term (e.g. buildings, equipment, and land) |

| Valuation | Valued at the market price or cost | Valued at cost less depreciation |

Conclusion

Current assets play a crucial role in a company's financial health by providing the liquidity necessary to meet short-term obligations.

These assets, from cash and accounts receivable to inventory and prepaid expenses, are expected to be converted into cash within one year, making them vital for maintaining operations and meeting current liabilities.

Understanding the components of current assets and how they are measured is essential for investors, as it helps assess the company's ability to convert these assets into cash when needed.

Investors and analysts can evaluate a company's short-term financial stability and capacity to manage immediate obligations by utilizing liquidity ratios such as the current, acid test, and cash ratios. These ratios are valuable tools for determining a company's risk and ability to navigate financial challenges.

In contrast to non-current assets, which provide long-term value, current assets focus on the short-term financial picture and are critical for a business's day-to-day operations.

A well-managed portfolio of current assets ensures that a company can remain agile and resilient in an ever-changing market environment. Therefore, monitoring and optimizing current assets is a key practice for businesses and investors aiming for long-term success and financial stability.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?