Asset Disposal

The process of the elimination of capital assets from a business’s operations which has to be reported.

What Is Asset Disposal?

Asset disposal refers to the process of removing long-term assets, such as equipment or machinery, from a company's accounting records when they are no longer needed or useful. This can involve selling the asset to recover any remaining value or simply removing it from the company's balance sheet if it has no value left.

Businesses dispose of assets for various reasons, including:

- The asset is fully depreciated and no longer contributes value.

- Maintenance costs exceed the asset's worth.

- The asset is no longer needed due to changes in the business.

- Unforeseen circumstances, such as theft or damage.

When an asset is disposed of, it’s essential to calculate its current book value, which is the original cost minus any accumulated depreciation. This value is necessary for accurately reflecting the asset’s worth at the time of disposal and ensuring the company's financial records are properly updated.

If completed correctly, the disposal of an asset will result in its removal from its books in a process called derecognition in accounting.

- Asset disposal is the elimination of capital assets from a business’s operations, which has to be reported.

- Successful asset discarding requires finding the asset’s net book value, adjusting for the accumulation of the depreciation or appreciation to the time of sale, and logging the gain or loss.

- Disposed asset has either generated a premium, or a discount or lost its entire value for the company, so it’s reflected in the three statements accordingly.

What are the Steps For Asset Disposal?

Asset disposal is generally executed through accounting and recording it properly with its implications reflected on the financial statements. The facilitation of asset disposal is outlined as follows.

Valuation

The value of the asset to be removed requires an assessment of its fair market value or net book value (NBV).

Fair market value is an agreed-upon price between both the seller and buyer to complete their transaction, conforming to the law of supply and demand.

Net book value is calculated as:

NBV = Original Asset Cost - Accumulated Depreciation

Where:

Accumulated Depreciation = Annum Depreciation * Total Number of Years

NVB commonly decreases very predictably and steadily over time.

Depreciation Adjustment

If the discarded asset is either appreciated or depreciated, adjust for the expense or gain accordingly. The remaining depreciation is recognized until the date of forfeiture, ensuring concurrent reporting of the asset’s carrying value.

Most assets lose value over time, so accountants have to ensure that these losses are recorded so they are upholding the standards of Generally Accepted Accounting Principles (GAAP) and not over or underestimating numbers.

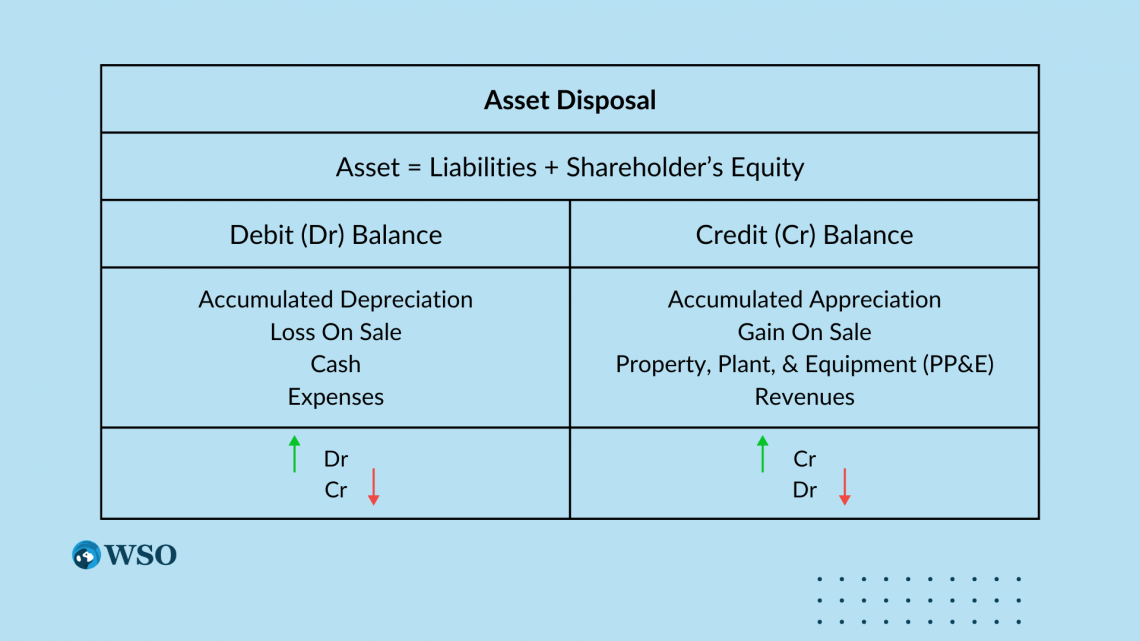

Gain or Loss Recognition

The disposal of an asset yielding a gain will be recognized as a gain from the sale. Conversely, if there is a loss, then it’s recorded as a loss from sales.

Any losses are treated like an expense and would be debited to increase the value. Gains would be credited to reflect money received from the disposal.

Recording Disposal

For bookkeeping, professional records onto a journal entry, also known as a T-account.

This is how a journal entry functions:

When drafting the T-account, it might be easier to visualize yourself as the Shareholder’s Equity on the credit side and process how each line item would affect you personally.

If you were, metaphorically speaking, the shareholder’s equity, line items like revenues would have increased your equity. Thus, revenues would be credited to the credit side of the balance.

Likewise, expenses would have a negative effect on your equity, so you are going to debit it under the debit balance.

Cash flows can be simplified by understanding their relationship with revenue and the corresponding debit and credit entries.

When revenue increases, the equivalent value is reflected in the cash account, ensuring both sides of the accounting equation balance. This approach helps manage and track financial transactions effectively.

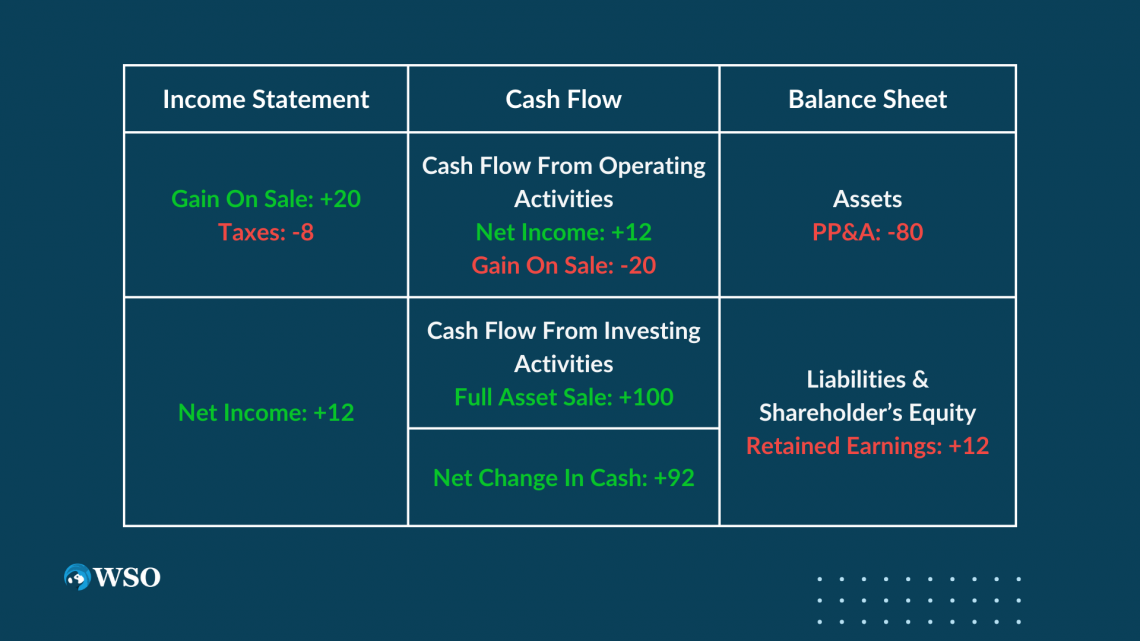

Three Financial Statement Impacts

The balance sheet must be revised to reflect the removal of the assets. The income statement reflects any gains or losses recognized and the impact it has on the net income.

For example, if a business sold an asset for $100 that had a net book value of $80, assuming a tax rate of 40%, it would affect the three statements as follows:

Assets equal Liabilities & Shareholder’s equity so the balance sheet balances.

Note

Why does Gain On Sale or the sale of an asset reduce the Cash Flow from Operation Activities? Remember, in the Cash Flow Statements, you both:

- Add non-cash expenses

- Subtract non-cash gains

Many younger students remember adding back non-cash expenses part but forget the flip side of the coin which is the subtracting of non-cash gains.

The adjustment removes non-cash gains.

On a conceptual level, the gain from the sale of an asset isn’t cash being generated by the company’s core operating activities. The cash gain of an asset had nothing to do with goods and services being sold to their customers.

Compliance/Disclosures And Auditing/Internal Controls

Professions will have to abide by the rules and regulations underwritten by the Financial Accounting Standards Board (FASB) with their issued and well-known GAAP guidelines.

Any additional disclosure requirements by other Federal organizations or your employer are mandatory usually entailing the providing of adequate information in the financial statements and highlighting any significant risks. This safeguards reporting accuracy and compliance with regulations and disclosures.

The trustworthiness with auditing and compliance on financial reporting helps stakeholders understand asset discarding on company performance.

The Two Main Asset Disposal Depreciations

The asset value is determined based on numerous factors including but not limited to: market demand, condition, age, functionality, and industry vertical.

The two ways to methods of evaluation are:

- Straight Line Method

- Double Declining Method

Straight Line Method

Straight Line is considered the simple method since it’s easier to calculate.

The formula is as shown below:

Annual Asset Depreciation = (Asset Cost - Salvage Value) / # Years of Useful Life

Where:

- Asset cost: How much was the asset purchased for?

- Salvage value: How much is the asset worth at the time of discard?

- Useful life: How long is the asset to be in use for the company?

Double Declining Method

The double declining method, commonly referred to as the accelerated method, frontloads depreciation expenses starting high and incrementally reducing over the asset’s life.

The formula has you dividing the years of useful life by 2, so the original depreciation expense will be double the straight-line method.

The formula is represented below:

The first year’s accumulated depreciation is $0.

Since not all assets are treated the same, the double declining method is very useful for assets that diminish in value extraordinarily quickly in the early years.

Note

The double declining method is the equivalent of 2*Straight Line Deprectiation*Book Value. Straight line depreciation is more commonly utilized professionally and is the GAAP standard.

Asset Disposal Journal Entry Example

For the sake of simplicity, let's assume that ABC Corporation has a delivery van worth $20,000 on the balance sheet. This situation will be applied to the rest of the examples shown below.

The journal entries described earlier in “Recording Diposal” are also explained further in detail.

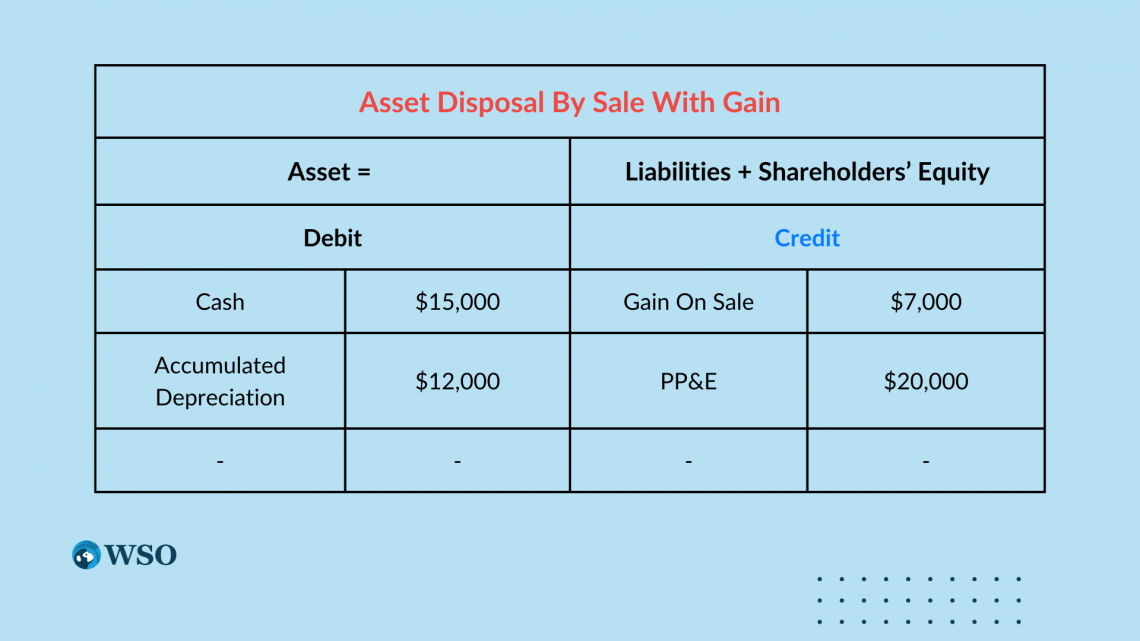

Asset Disposal with a Gain

ABC Corp sells the van that is no longer necessary for the business. The truck being purchased 3 years ago for $20,000 has an accumulated depreciation of $12,000.

The company sold it for $15,000 cash.

Let’s walk through what an Asset Disposal with a gain would look like.

The NBV is $8,000 since the Asset Cost of $20,000 - accumulated depreciation of 12,000.

However, since the company sold it for $15,000 which is higher than the NBV, so the company has sold it for a premium.

To authenticate the journal entry, make sure Assets = Liabilities + Shareholder’s Equity. In this scenario $15,000 + $12,000 = $7,000 + $20,000, so the journal entry is correct.

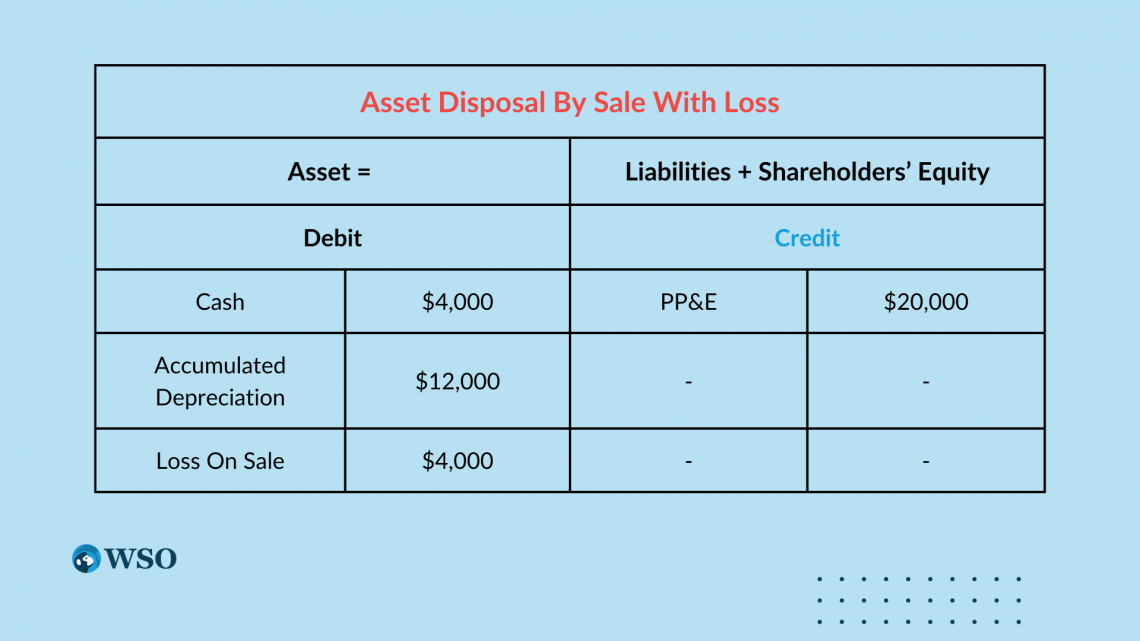

Asset Disposal with a Loss

ABC Corp sells the van that is no longer necessary for the business. The truck being purchased 3 years ago for $20,000 has an accumulated depreciation of $12,000.

The company sold it for $4,000 cash.

Let’s walk through what an Asset Disposal with a loss would look like.

The NBV is $8,000 since the Asset Cost of $20,000 - accumulated depreciation of 12,000.

However, since the company sold it for $4,000 which is lower than the NBV, the company incurred a loss on the sale.

To authenticate the journal entry, make sure Assets = Liabilities + Shareholder’s Equity. In this scenario $4,000 + $12,000 + $4,000 = $20,000, so the journal entry is correct.

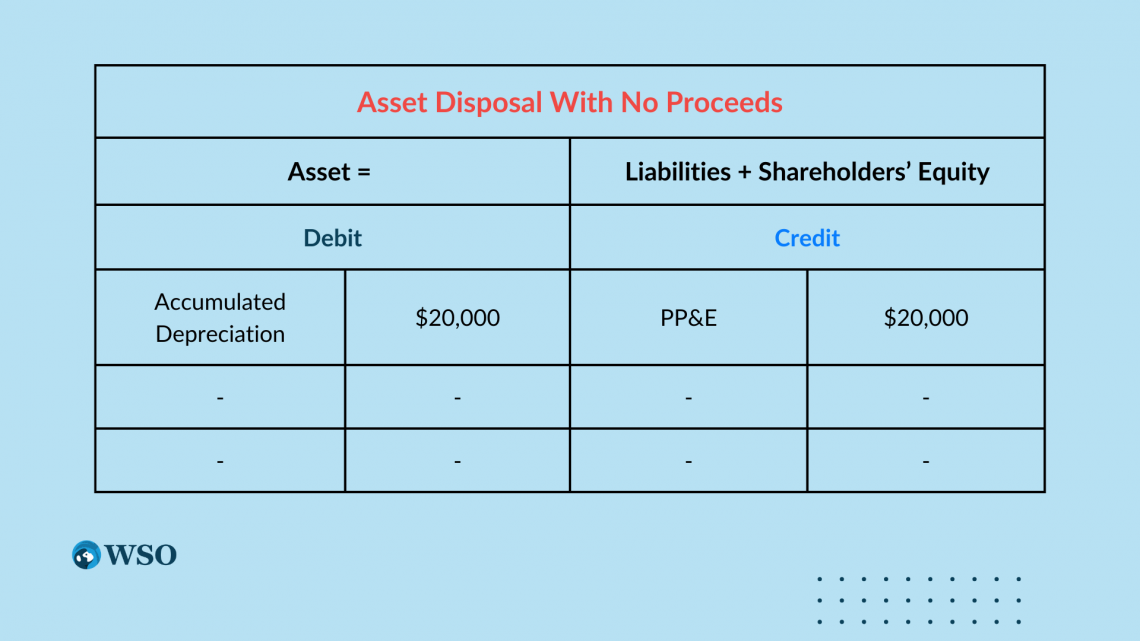

Asset Disposal with No Proceeds

ABC Corp sells the van that is no longer necessary for the business. The truck being purchased 3 years ago for $20,000 has an accumulated depreciation of $20,000.

Let’s walk through what an Asset Disposal with no proceeds at 100% depreciation would look like.

The NBV is $0 since the Asset Cost of $20,000 - accumulated depreciation of 20,000.

The company cannot sell the asset, because it’s already fully depreciated.

To confirm your journal entry, ensure Assets = Liabilities + Shareholder’s Equity. In this scenario $20,000 = $20,000, so the journal entry is correct.

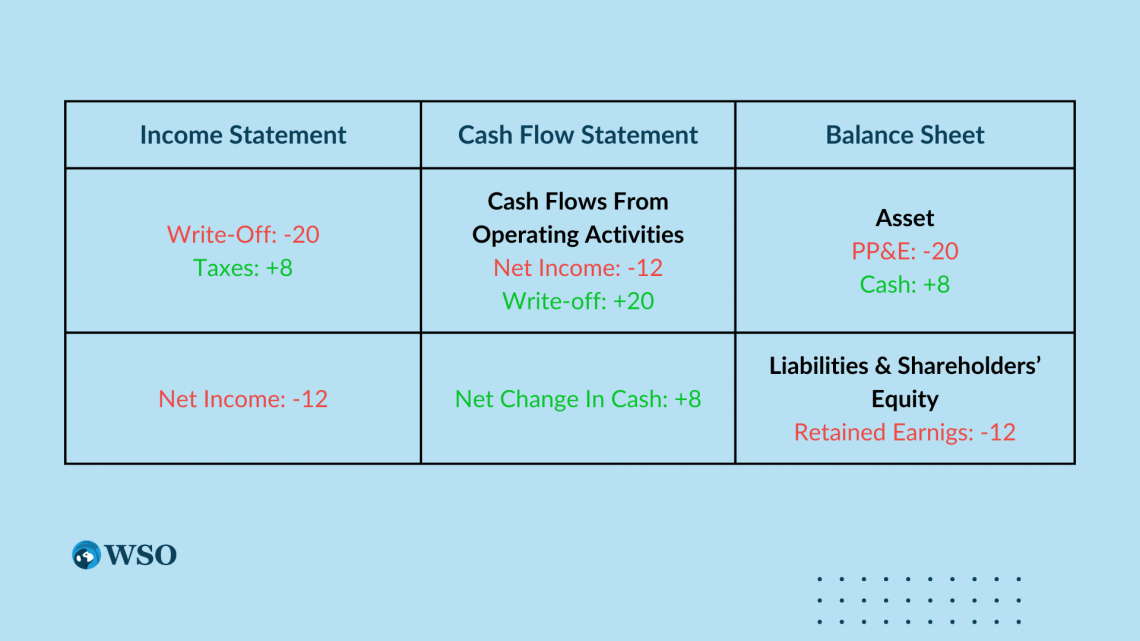

We’re going a little deeper for this specific example because a fully depreciated asset would be considered a write-off to zero and not a simple gain or loss like in the previous two examples.

Here’s what a write-off to zero would look like on the three statements rather than an asset gain/loss.

Assume a 40% tax rate. Values are recorded in thousands.

Asset Disposal FAQs

In tax law, write-downs are tax-deductible, so 40% of the write-off will be added back to net income.

The write-down is a non-cash expense. Physically, there is no cash entering or leaving the company.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?