Working Capital Cycle

The time required to convert the net operating capital (the difference between contemporary assets and present-day liabilities) into cash.

What is a Working Capital Cycle?

The Working Capital Cycle is the time required to convert the net operating capital (the difference between contemporary assets and present-day liabilities) into cash. The working capital cycle is crucial to managing a business's finances.

Businesses can optimize their cash flow and ensure smooth operations by effectively managing this cycle.

The operating cycle revolves around three key components:

- Inventory

- Accounts receivable

- Accounts payable

These features play an essential role in determining the cycle span. Inventory represents the goods or raw materials held by a company. Businesses aim to sell their inventory quickly to minimize the time it remains tied up and to generate revenue.

Efficient inventory management helps in reducing the time inventory remains tied up, including:

- Accurate forecasting

- Monitoring demand

- Implementing just-in-time practices

Accounts receivable refers to the money owed to a business by its customers for products or services provided on credit. Collecting revenue from customers promptly is essential to shorten the operating cycle.

Companies can achieve this by establishing clear payment terms, implementing effective credit control measures, and ensuring timely invoicing and follow-up.

On the other hand, accounts payable are the outstanding payments a business owes to its suppliers. Extending the payment period to suppliers strategically can affect the cash conversion period.

Businesses can ensure efficient cash flow management by optimizing these three components of the working capital cycle. Shortening the cycle may improve cash flow, allowing for greater financial agility and flexibility.

It allows businesses to meet operating costs, invest in growth opportunities, and deal with unexpected challenges.

Effective operating cycle management involves continuous monitoring and analysis of financial data, such as cash flow statements, inventory turnover ratios, and days sales outstanding.

Businesses can utilize financial tools and techniques to forecast cash flows, identify potential bottlenecks, and make informed decisions to streamline the cycle.

It is worth noting that the operating cycle can vary across industries and businesses. Factors such as the nature of products or services, market dynamics, and business strategies influence the cycle duration.

Therefore, business leaders must understand industry dynamics and adapt their working capital management strategies accordingly. The working capital cycle represents the time to convert net operating capital into cash.

- The working capital cycle (WCC) measures the time it takes for a business to convert its net working capital (current assets minus current liabilities) into cash.

- It reflects the efficiency with which a company manages its short-term assets and liabilities to generate cash flow.

- WCC = Inventory Period + Accounts Receivable Period - Accounts Payable Period. A shorter cycle indicates a more efficient company, while a longer cycle suggests potential cash flow issues.

- Efficient working capital management can reduce the need for external financing, thereby lowering interest expenses and increasing profitability.

Importance of Working Capital Cycle

The operating cycle plays a crucial role in the financial management of businesses, encompassing various components that impact their liquidity, cash flow, and overall profitability.

It is a vital measure to assess the efficiency and effectiveness of a company's operational and financial activities.

By understanding and managing the working capital cycle, businesses can ensure timely supplier payments, optimize inventory levels, and streamline accounts receivable and payable processes.

This introduction sets the stage for exploring the significance of the operating cycle in facilitating liquidity management, cash flow optimization, risk mitigation, profitability enhancement, and strategic decision-making.

NOTE

Efficiently managing the working capital cycle is paramount to any business's financial well-being and sustainability.

It encompasses the dynamic relationship between a company's current assets and liabilities, directly influencing its liquidity, cash flow, and overall operational efficiency.

By analyzing and optimizing the elements of the operating cycle, organizations can effectively meet their short-term obligations, seize growth opportunities, and mitigate financial risks.

A well-managed cash conversion cycle ensures timely supplier payment, minimizes excess inventory holding costs, maximizes customer collections, and reduces reliance on external financing.

This intricate interplay between cash, inventory, receivables, and payables is instrumental in maintaining a healthy financial position, enhancing profitability, and enabling strategic decision-making.

By recognizing the significance of the cash conversion cycle, organizations can effectively navigate economic changes, capitalize on competitive opportunities, and attain sustainable success within their industries.

Leveraging the Working Capital Cycle for Competitive Advantage

Organizations constantly seek a competitive edge in today's dynamic business landscape. One often overlooked yet powerful avenue for achieving this advantage lies within the working capital cycle.

The working capital cycle encompasses the processes involved in managing a company's cash flow, inventory, and accounts receivable/payable. Businesses can optimize their operational efficiency and enhance financial performance by strategically leveraging these components.

Efficient management of the working capital cycle can lead to numerous benefits. First and foremost, it enables organizations to improve their cash flow position.

NOTE

By minimizing the time between cash outflows and inflows, companies can ensure a healthy liquidity position, allowing them to meet their financial obligations and seize growth opportunities.

Moreover, effective inventory management can reduce carrying costs, mitigate obsolescence risks, and improve customer satisfaction through timely product availability.

Furthermore, a streamlined accounts receivable and payable process can enhance relationships with suppliers and customers.

Optimizing the collection of receivables and negotiating favorable payment terms with vendors can bolster cash inflows and reduce the need for external financing.

This, in turn, increases a company's financial stability and flexibility, enabling it to respond swiftly to market fluctuations and capitalize on emerging opportunities.

Primary Competitive Advantages Of Leveraging The Working Capital Cycle

The primary competitive advantages include the following:

Liquidity Management

The cash conversion cycle helps businesses maintain sufficient liquidity to cover operational expenses and meet short-term obligations.

Efficient working capital management ensures the company has enough cash and resources to pay suppliers, employees, and other creditors promptly.

By monitoring and optimizing the cash conversion cycle, businesses can prevent cash shortages and reduce reliance on expensive short-term financing options.

Cash Flow Optimization

A well-managed working capital cycle improves cash flow by minimizing the time lag between cash outflows and inflows. Effective inventory management ensures that businesses refrain from tying up excessive funds in excess stock and can convert inventory into cash quickly.

Streamlining accounts receivable and payable processes enables businesses to collect customer payments faster while negotiating favorable payment terms with suppliers.

Risk Mitigation

The operating cycle helps businesses identify potential risks and vulnerabilities in their cash flow. By monitoring the components of the operating cycle, such as:

- Inventory turnover ratio

- Accounts receivable turnover ratio

- Accounts payable turnover ratio

NOTE

Businesses can detect inefficiencies, address bottlenecks, and reduce operational risks.

Managing the operating cycle effectively reduces the risk of cash flow disruptions, late payments, and potential financial distress.

Profitability Enhancement

A well-managed working capital cycle contributes to overall profitability. Efficient inventory management reduces carrying costs, such as storage, insurance, and obsolescence, positively impacting the bottom line.

By optimizing accounts receivable and payable processes, businesses can improve cash inflows and negotiate favorable credit terms, which reduces financing costs and enhances profitability.

Strategic Decision Making

The operating cycle provides valuable insights for strategic decision-making. By analyzing trends in working capital components over time, businesses can identify patterns, plan for seasonal fluctuations, and make informed decisions regarding production, pricing, and financing.

Understanding the operating cycle helps businesses allocate resources effectively and identify areas for process improvement.

NOTE

The operating cycle helps businesses optimize inventory management, reduce stockouts, and improve customer satisfaction by ensuring timely product availability.

Calculating Working Capital Cycle

Calculating the operating cycle remains crucial for evaluating a company's cash flow efficiency and ability to manage short-term liabilities.

This analysis offers valuable insights into a company's liquidity, operational efficiency, and financial health.

By following key steps, businesses can determine their operating cycle, gain a deeper understanding of working capital management, and make informed decisions to optimize financial performance.

Calculating the operating cycle involves assessing a company's cash flow efficiency and short-term liabilities.

This analysis provides valuable insights into liquidity, operational efficiency, and financial health.

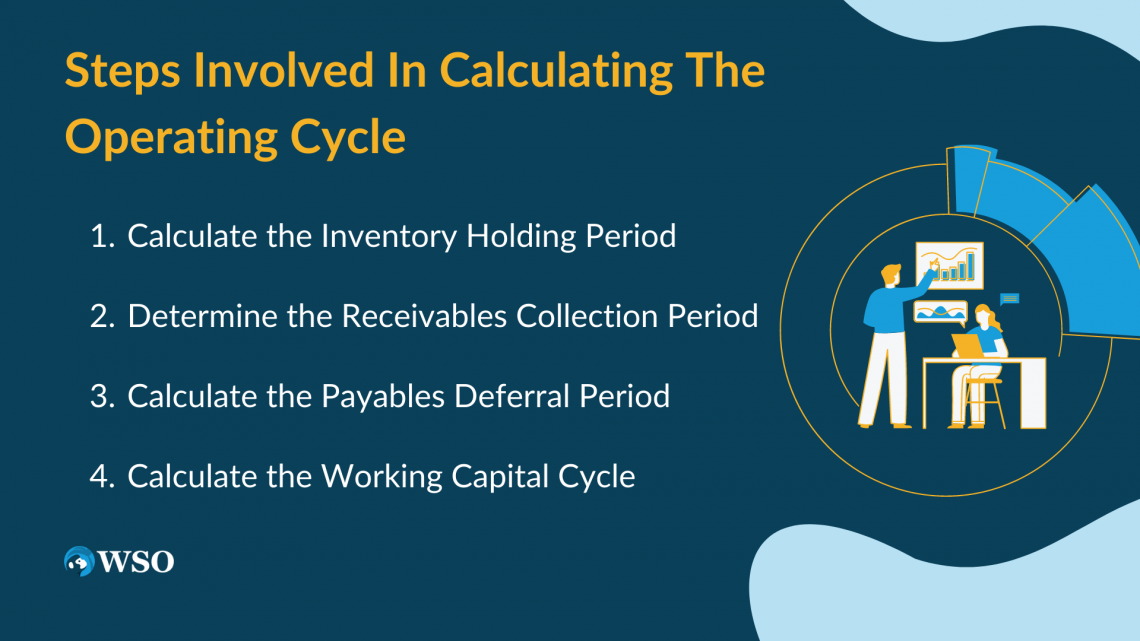

Steps Involved In Calculating The Operating Cycle

Here are the key steps involved in calculating the operating cycle:

- Calculate the Inventory Holding Period: This step involves determining the average number of days it takes for the company to convert its inventory into sales. By dividing the average inventory value by the cost of goods sold (COGS) daily, businesses can ascertain how long it typically takes to sell inventory.

- Determine the Receivables Collection Period: This step involves calculating the company's average days to collect customer payments. Dividing the average accounts receivable value by the sales per day helps assess the efficiency of the company's credit and collection policies.

- Calculate the Payables Deferral Period: This step involves determining the average number of days it takes for the company to pay its suppliers. Dividing the average accounts payable value by the cost of goods sold (COGS) per day helps evaluate the company's payment terms and ability to manage payables effectively.

- Calculate the Working Capital Cycle: To obtain the operating cycle, subtract the payables deferral period from the sum of the inventory holding period and the receivables collection period. The resulting figure represents the number of days it takes for the company to convert resources into cash.

NOTE

Analyzing the cash conversion cycle provides valuable insights into a company's overall financial efficiency, cash flow management, and the effectiveness of working capital management strategies.

A shorter cash conversion cycle indicates the company can quickly convert resources into cash, which is generally favorable. Conversely, a longer cycle suggests the company may face liquidity challenges or operational inefficiencies.

The cash conversion cycle is a fundamental metric offering valuable insights into a company's liquidity and operational efficiency. Analyzing this cycle allows businesses to assess their ability to manage resources and convert them into cash effectively.

A shorter cash conversion cycle signifies that the company can swiftly transform resources, such as inventory and accounts receivable, into cash.

This is generally positive, indicating the company can meet short-term obligations and maintain a healthy cash flow position. On the other hand, a longer cash conversion cycle raises concerns about a company's liquidity and operational effectiveness

It suggests the company takes more time to convert resources into cash, potentially indicating challenges in managing inventory, collecting receivables, or delaying supplier payments.

By closely monitoring and analyzing the cash conversion cycle, businesses can identify areas for improvement and implement strategies to enhance liquidity and operational efficiency.

This may involve streamlining inventory management, optimizing accounts receivable collection processes, negotiating favorable payment terms with suppliers, or implementing working capital financing solutions.

A well-managed cash conversion cycle ultimately contributes to a company's financial stability, growth, and overall success in the marketplace.

Working Capital Cycle Sample Calculation

Let's illustrate a hypothetical example of the cash conversion cycle calculation.

Assume we have a company called ABC Electronics that sells electronic gadgets. We'll calculate the cash conversion cycle for ABC Electronics based on the following information:

Inventory Holding Period

Assuming the following figures.

Average Inventory Value: $50,000

Cost of Goods Sold (COGS) per Day: $1,000

The calculation is as follows:

Inventory Holding Period = Average Inventory Value / COGS per Day

Inventory Holding Period = $50,000 / $1,000 = 50 days

This means it takes ABC Electronics approximately 50 days to sell its inventory.

Receivables Collection Period

Average Accounts Receivable Value: $30,000

Sales per Day: $2,000

The calculation is as follows:

Receivables Collection Period = Average Accounts Receivable Value / Sales per Day

Receivables Collection Period = $30,000 / $2,000 = 15 days

This means ABC Electronics takes approximately 15 days to collect customer payments.

Payables Deferral Period

Average Accounts Payable Value: $20,000

Cost of Goods Sold (COGS) per Day: $1,000

The calculation is as follows:

Payables Deferral Period = Average Accounts Payable Value / COGS per Day

Payables Deferral Period = $20,000 / $1,000 = 20 days

This means ABC Electronics takes around 20 days to pay its suppliers.

Working Capital Cycle

Working Capital Cycle = Inventory Holding Period + Receivables Collection Period - Payables Deferral Period

Cash Conversion Cycle = Inventory Holding Period + Receivables Collection Period - Payables Deferral Period

Working Capital Cycle = 50 days + 15 days - 20 days = 45 days

ABC Electronics has a cash conversion cycle of 45 days. This means the company takes approximately 45 days to convert its resources (inventory and accounts receivable) into cash.

By analyzing this working capital cycle, ABC Electronics can assess its cash flow efficiency and identify areas for improvement.

For instance, if the business enterprise can reduce its stock retaining duration or grow its receivables series duration, it will be capable of shortening the operating capital cycle and enhancing its cash flow function.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?