Accounts Payable

Outstanding financial obligations that a company owes to its suppliers or creditors for goods and services received on credit

What is Accounts Payable (AP)?

Accounts Payable is an accounting term that represents a company's short-term debt. It is found under Current Liabilities on a Balance Sheet and Operating Activities on the Cash Flow Statement.

It can also be considered an IOU and is typically used when the firm has received a service or product (i.e., parts order, management consultation, etc.) but has not yet paid for it, that pending payment is recorded as an Accounts Payable.

In practicality, Accounts Payable is a specific category on a balance sheet. It keeps track of what a company owes for goods and services that were obtained on credit, meaning they were received but payment hasn't been made yet.

The whole process of handling these payables helps a company manage its activities and enhance its overall cash flow. It starts with acquiring goods or services and concludes when the company settles its debts with the suppliers.

Although AP is said to be a supporting activity, being aware of its implications helps better sustain a business. It is beneficial to pay attention to the payable expenditure and prioritize placing systematic internal controls that prevent error or fraud.

- Accounts Payable represents a company's short-term debts and is listed under Current Liabilities on the Balance Sheet.

- Accounts Payable is not a business expense; it is a liability due within a specific time frame usually one year.

- Account Payable represents a company's short-term debts to suppliers, while Account Receivables represents debts owed to the company by customers.

- Account Payable Turnover Ratio calculates the frequency of payments made by a company to its creditors, indicating liquidity.

Where is AP found?

It can be found in a company's financial position and cash flow statement.

AP appears in the Statement of Financial Position (also known as the Balance Sheet) under 'Current Liabilities.' It represents the total amount due to suppliers for the goods and services purchased on credit by the company.

The balance of payables varies throughout the year; the difference is between the opening and closing balance of the AP (which is recorded in the cash flow statement under "Cash Flow from Operating Activities").

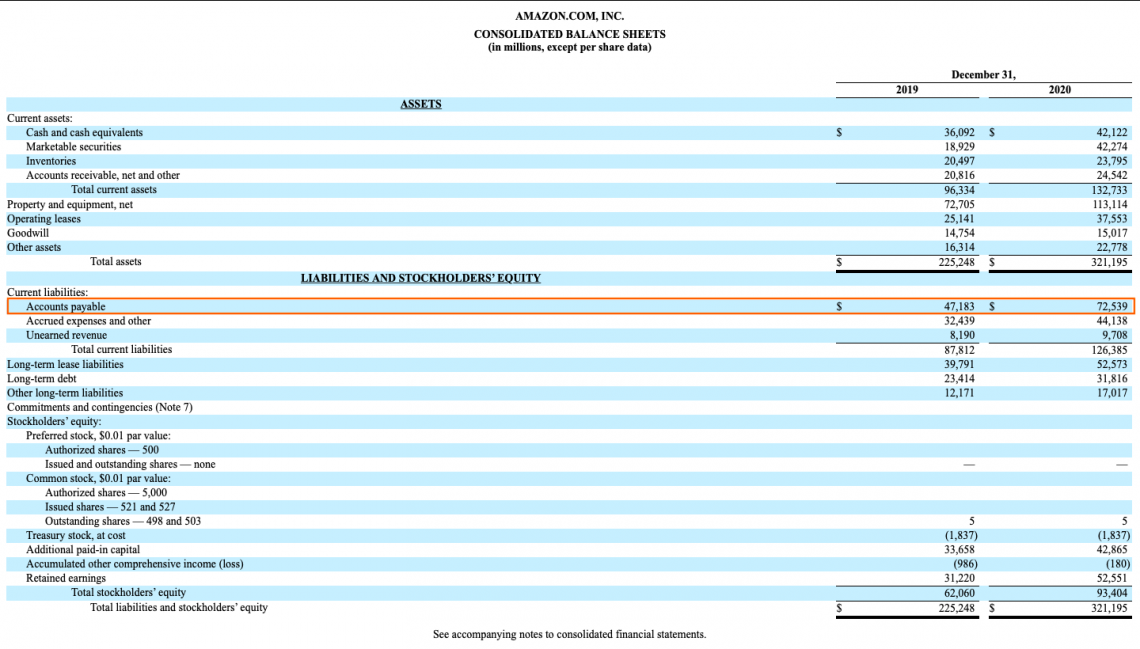

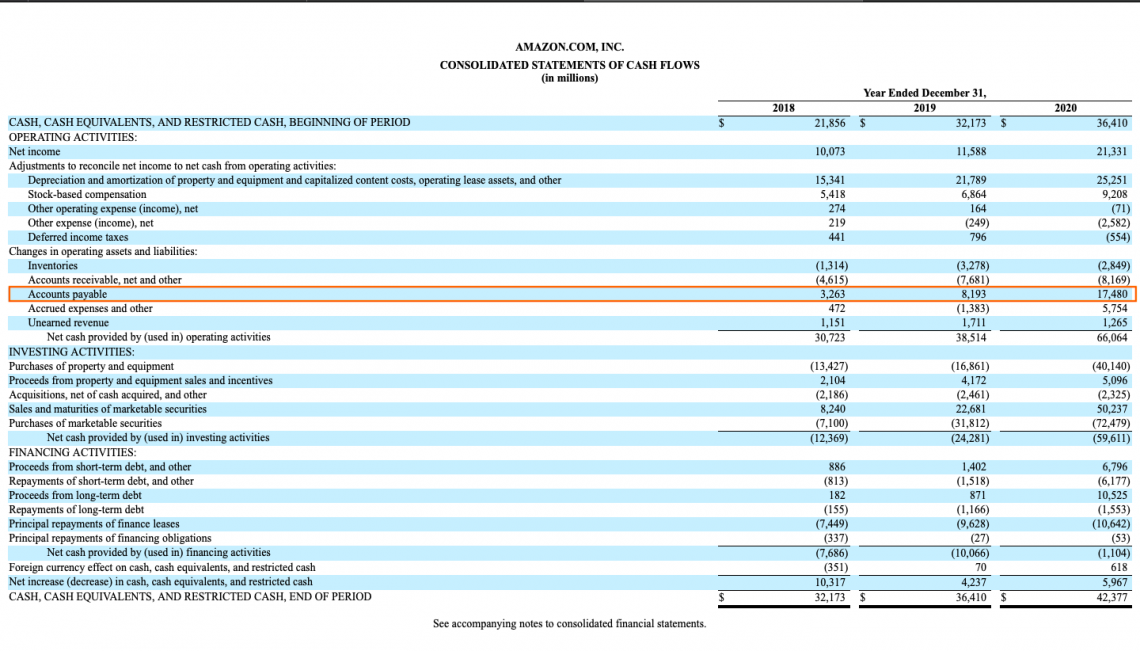

The following visuals are the Consolidated Balance Sheet and Consolidated Cash Flow Statement of AMAZON.COM INC for 2020.

*Highlighted box in orange shows the accounts payable for the year 2020 for Amazon.com Inc.

The entire financial statement documents of Amazon are accessible by clicking here. To learn about Financial Statements and which statement is most important, check out this WSO article.

Accounts Payable (AP) Vs. Trade Payable (TP)

Accounts payable (AP) and Trade payables (TP) are interchangeable accounting terms. This is because they both represent short-term debts that a company owes. There is, however, a slight difference.

AP refer to all short-term obligations (including trade payables). To understand better, let us look at some examples of AP.

1. Transportation and Logistics

A considerable part of operations involves moving goods from one place to another, and often these services are taken on a contract basis. The amount to be paid is specified in the document, and these accounts fall under the umbrella of AP.

2. Leasing and Licensing

Leasing office space or equipment involves monthly or annual payments to the owner of the equipment - the Lessor. Lease rental payable(s) are payments per contract, and it's AP's responsibility to remit the due amount.

Even' rent payments' for renting office space are considered payable, which is why annual rent payments come under the AP umbrella.

Licensing trademarks or patents involves paying annual charges for their use – it is taken care of by the AP department.

3. Raw Material Purchase and Vendor Payments

A considerable part of the payables includes purchasing raw materials on credit. Every organization engaged in manufacturing requires frequent credit purchasing. Such purchases fall under trading activities. Such vendor payments are called trade payables.

Trade Payables (TP) are short-term payments to a supplier or vendor for inventory-related goods.

For example:

- Purchasing raw materials on credit. Like a sugar manufacturing company or a clothing factory purchasing luxury textiles on credit.

- Delivery service provided by the supplier to transport raw materials to the factory on credit is also a trade payable.

From the above examples, we can see that the trade payables are for activities that pertain to materials or supplies used as inventory in the business. While on the other hand, APs are for indirect expenses.

Materials, inventory, or supplies purchased on credit impact the trading account and thus translate how the organization arrives at its 'gross profit' calculation.

Indirect expenses go on the profit and loss statement (also called the income statement) and are deducted from the gross profit to yield net profit.

The payment process will be the same for trade and accounts payable(s). Timely payments, as well as good vendor relations, helps a company improve its profitability.

In conclusion, it is safe to say that all trade payables are accounts payable, but not all accounts payable are trade payables. Trade payables specifically pertain to 'inventory,' the keyword which differentiates the two terms and their distinctions.

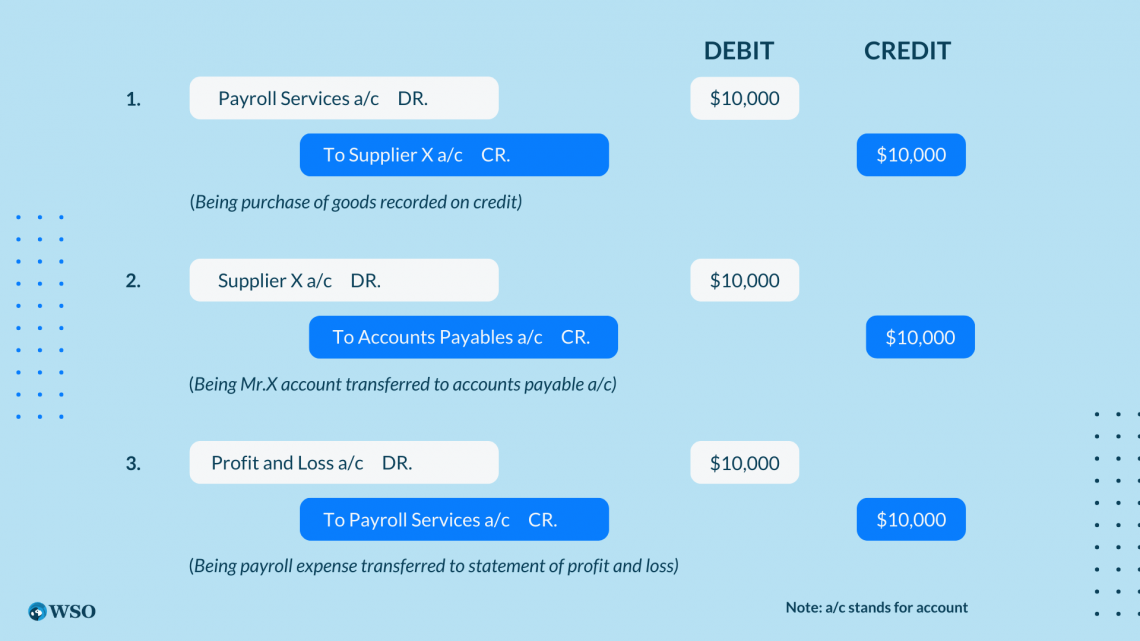

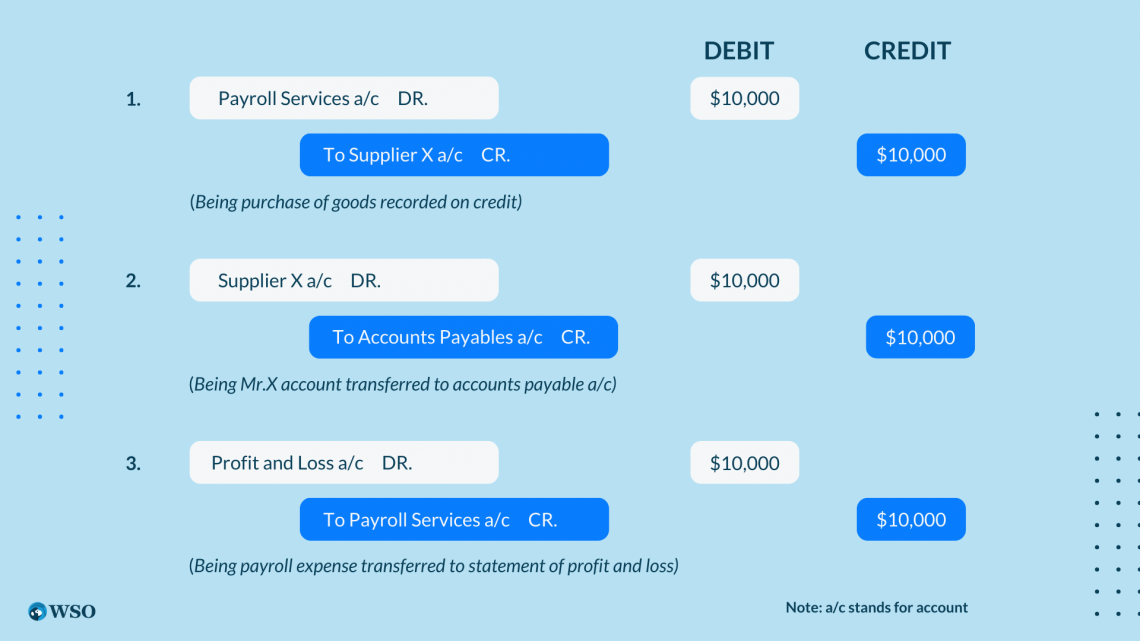

Example for Accounts Payable

Supplier X supplies payroll services to Company ABC for $10,000 on a credit basis, payable within six months. The $10,000 represents a 6-month AP liability (or short-term debt) owed by Company ABC to Supplier X.

Journal Entry will be as follows:

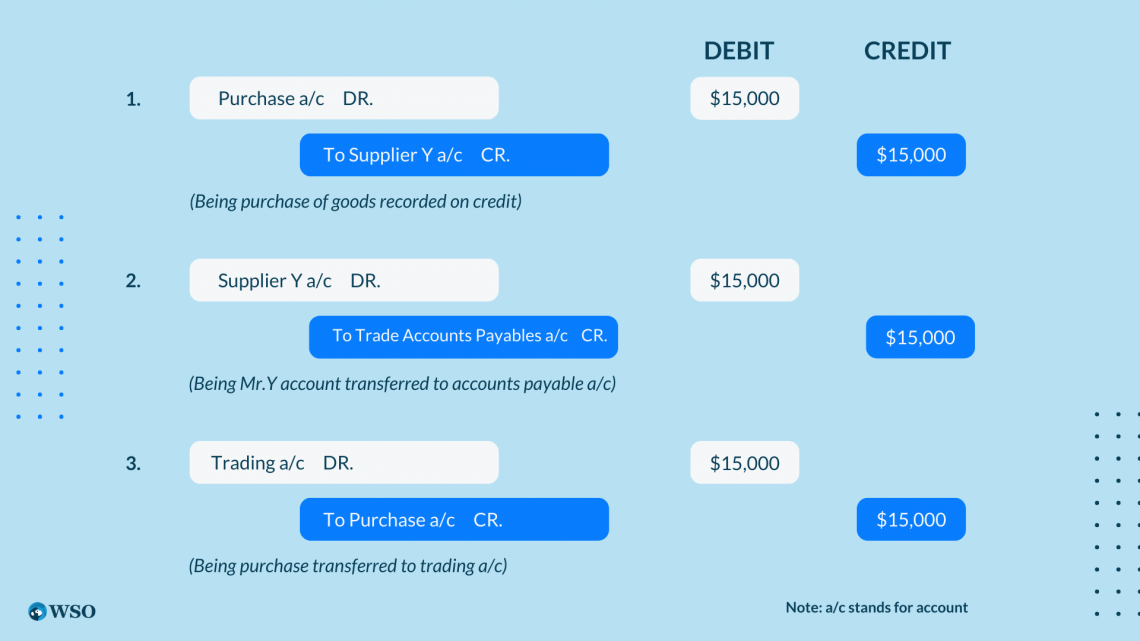

Example for Trade Payables

Supplier Y supplies goods to Company PQR for $15,000 on a credit basis, payable within six months. The $15,000 represents the trading account payable to Mr. Y and will be a short-term liability for the company.

Journal Entry for the above example:

Is AP a Business Expense?

AP's are liabilities due within a given time frame and are personal accounts by nature. Therefore, balances remaining at the end of an accounting period for personal accounts appear on the balance sheet.

Business expenses, on the other hand, are charged against profit. They are deducted from the total revenue to yield net profit. Business expenses are classified as nominal accounts.

Nominal accounts are accounts associated with the income statement. It records incomes, gains, expenses, and losses for an accounting period. To better understand the types of accounts - real, nominal, and personal with their definitions and differences, refer to this article here.

Thus, we can conclude that AP is not a business expense. Instead, it is merely a personal account created when journaling entries and closes when the balance amount is paid.

Let us quickly look at the journal entry below from the first example of this article:

Supplier X supplies payroll services to Company ABC for $10,000 on a credit basis, payable within six months. The $10,000 represents a 6-month AP liability (or short-term debt) owed by Company ABC to Supplier X.

The payroll service is a business expense for an organization that will be charged against profit and loss, whereas the 'Supplier X' account is an AP, which will be repaid within the stipulated time. Payroll service is a debit account, while AP is a credit account in the trial balance.

Thus the conclusion, AP is not a business expense.

What is the difference between Accounts Payable (AP) and Accounts Receivable (AR)?

Accounts Payable and Accounts Receivable are accounting terms representing two sides of the same coin. As a result, they both play a distinct role in maintaining a healthy cash flow for the company.

Again, AP refers to a company's short-term debts to its suppliers or vendors. The company here says, 'I owe you to the supplier. Moreover, they are current liabilities for the company and represent future cash outflows.

The Accounts Payable Turnover Ratio (APTR) calculates the AP turnover:

Now let us lightly discuss the Accounts Receivable Turnover Ratio (APTR).

Accounts Receivable Turnover Ratio (ARTR) calculates the company's frequency in collecting its debt from customers. It calculates the turnover by dividing 'Net credit sales' by 'Average accounts receivable.'

Accounts Receivable (AR) refers to the debt that a customer owes to a company. They are current assets and represent future cash inflows to the company. To better understand ARTR, refer to this in-depth WSO article here.

Accounts Payable Turnover Ratio (APTR)

APTR calculates the rate at which the company pays off its supplier. APTR is also known as the Creditors Turnover Ratio (CTR).

APTR determines the frequency of payments made by a company to its creditors over an accounting period. And since it determines the frequency of payments (or cash outflow), it is considered a Liquidity Ratio.

For more on accounting ratios, read this in-depth WSO article explaining liquidity ratios, their uses, when to use them, all other ratios, and more!

Where,

Example on APTR

Question: The total purchases made by the company XYZ were $1,000,000, of which

78% were on credit. The returns for the year were $10,000.

Opening Bal. of AP = $230,000

Closing Bal. of AP = $450,000

Calculate the AP turnover ratio.

Answer:

Hence, payments are made 2.26 times a year.

Working Notes:

Thus, we can see that the company's APTR is 2.26 times (or 161 days) the average time it takes to pay off its supplier.

The higher a company's APTR, the more favorable it is to their:

- Investors

- Bankers

- Suppliers

- Creditors

It demonstrates that a company pays back its debts frequently without delays.

To better understand AP Turnover Ratio and its implications, read here.

How is the AP Process Recorded?

AP Processes differ slightly for every organization based on the volume of transactions within a company. But they all seek to streamline their processes to improve cash flow and working capital management.

It starts with the 'Procurement to Pay cycle,' or the 'P2P cycle', where the department with the requirement for any item, inventory, service, etc. from an outside vendor defines its needs and specification in the 'Purchase Requisition' document.

A purchase requisition document is an internal document generated by an employee in the organization whenever there is any requirement for goods or services.

The purchasing department then sets out to identify a suitable vendor. It can negotiate the price and quantity, or if there is already a contract, the department can go ahead with the specified terms.

At this stage, the purchasing department creates a 'Purchase order' or PO for the required item to be sent to the supplier for procurement. The supplier, in turn, sends the confirmation receipt for the order placed according to the available inventory level.

When the organization receives the goods, the warehouse records the delivery in the 'Receiving Report.' It is important to note the discrepancies in quantity and quality here. The delivery confirmation is sent back to the vendor.

With the information available with the supplier in the delivery confirmation report, the supplier can either reject or accept the discrepancies and provide credit for the same.

The final invoice is then sent to the purchasing department, which transfers it to the AP department for payment.

The AP team captures the invoice data and codes invoices with the correct amount and cost center in the accounting system. It then approves invoices by matching them with the purchase order and receiving the report.

Finally, the invoice is ready for payment on the due date.

The entire AP workflow process includes three documents that are to be matched for details as we move forward:

- Purchase Order (PO)

- Receiving report (also called goods receipt)

- Vendor's invoice

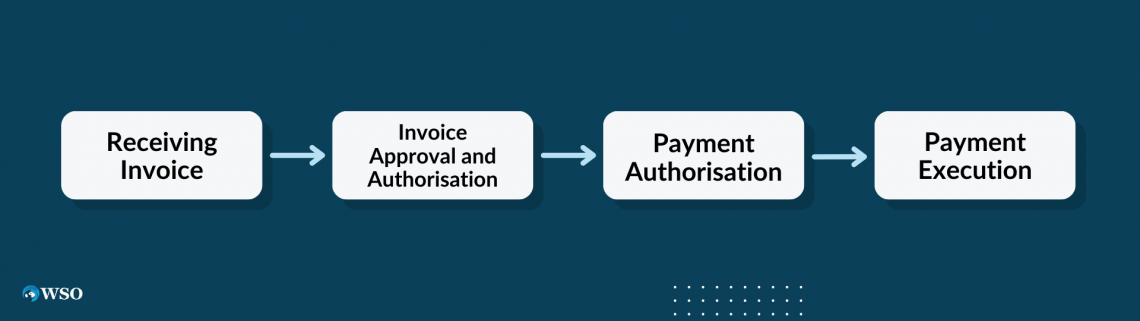

The next steps depict the actual payable process:

Step 1: Receiving the Invoice

Once the goods are received, the supplier sends the invoice to the organization, particularly the purchasing department, to collect its payments. Then the invoice is routed to the AP department. AP receives the invoice and proceeds to move to the next step for approval.

Step 2: Invoice Approval and Authorisation

The second step towards the AP Process involves approving the invoice issued via the supplier by conducting a three-way match between the three documents - Purchase Order (or PO), the 'Receiving report, and the supplier's invoice.

Before the invoice is entered into the system, it should reflect what the company has ordered and received the good/service, along with the units and price. Details listed below are vouched and verified, and captured into the system:

- Order ID

- Name of the supplier

- Quantity of goods ordered

- Prices of the items

- Date of the delivery

- Date of payment

If discrepancies arise with the quantity or price, the AP department sends the invoice back to the purchasing department to rectify it.

Step 3: Payment Authorization

After verifying all the details and resolving conflicts, the payable amount to the supplier is finalized. Then, payment authorization takes place by a higher authority in the AP department.

They finalize the mode of payment and the date, considering all the factors and where the company has taken maximum benefit for the credit period.

The invoice is marked 'Approved for Payment' in the system and sent for final processing, which is the next step, i.e., executing the payment.

Step 4: Payment Execution

Executing the payment is the last process and involves marking the invoice as paid in the accounting system.

Once everything is authorized and approved, remittance is sent to the vendor through cheque or cash on the stipulated date. If any interest or penalty is applicable, it is added to the total payable amount. Finally, the following accounting entry takes place to mark the account closure:

What about vendor invoices without purchase orders or receiving reports?

Not all invoices received by the vendor have delivery of goods or purchase orders. Therefore a three-way match is not always possible. For example, lease rentals are to be paid annually or monthly, or certain contract payments have their scheduled payments.

The AP department has to scrutinize the invoices and schedule payments according to when they are due.

How to Optimize AP Process?

-

With the advent of technology, AP is now automated for faster processing, reducing human error and saving time and cost involved in manual processing.

- Organizing and prioritizing the invoices as per the order date and credit period.

- Streamlining the work can help reduce manual labor and bring efficiency to the operations by eliminating bottlenecks.

- Keeping track of KPIs (Key Performance Indicators) to monitor AP. KPIs include:

- Cost per invoice process

- Days payable outstanding

- Payment accuracy rate

- Late interest, fees rates, or invoice rates

- Early discount capture rate

- Keeping supplier information up to date.

- Putting internal controls in place to avoid misrepresentation due to error or fraud.

AP Department

It is also the independent department in an organization or a company that works actively to handle debt operations.

Back in the early days, AP was considered a back-end operation. But as the market grew more fierce and technologically advanced, Chief Financial Officers (CFOs) realized how crucial payable systems are to improve a company's cash flow.

All businesses, big or small, are now gradually opting for separate payable departments to handle the transactions more efficiently and effectively. The department also takes care of the administrative, clerical, and accounting work involved in the AP process.

What is the role of the AP Department?

The Account Payable Department handles the verification of invoices and is also responsible for the execution of payments to invoices. It also oversees the settlement of late fees and penalties associated with overdue payments or breaches of contracts.

A well-managed AP department can help companies save substantial amounts of time and money by optimizing the liabilities payable process.

The AP department is also responsible for:

- Searching for appropriate vendors or suppliers who could provide quality material at the best prices.

- Partnering with vendors to secure long-term discounts for bulk purchases.

- Generating reports every week or month to monitor the department's activities.

- Inclusion of internal controls to look for deficiency in the AP Process.

What happens if the AP or AP department is not efficient?

- Accounts can remain overdue, resulting in late payments. This will accumulate interest on the unpaid amount affecting the cash flow for the credit period. Therefore, an organization should always pay their bills on time, but never before they are due for payment.

- Payment term violations can lead to penalties for the company.

- Inconsistent payments to the vendors could lead to a strained relationship, forcing vendors to provide inferior services.

- Inconsistency in maintaining inventory impacts the operations of the company, mainly manufacturing.

- Gaps in internal controls in the AP Process can lead to fraud.

or Want to Sign up with your social account?