EBITDA

Earnings Before Interest, Tax, Depreciation and Amortization

What is EBITDA?

EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortization) measures a company’s operating performance.

It provides information on a company’s earnings before netting out non cash expenses like depreciation of a firm’s assets and non operating expenses like payments of interest and taxes. For this exact reason, it may not give a reliable estimate of a company’s profitability.

EBITDA, although not supported under GAAP or IFRS, can provide an apples-to-apples comparison between companies within the same industry because it eliminates the effects of depreciation, interest expense, and taxes - which often varies from company to company.

It is often used in replacement of net income when valuing large private companies. It is also used in place of net income when net income for a growing company is negative. It is commonly used in many valuation methods such as:

- Discounted Cash Flow (DCF)

- Asset-based Valuation (ABV)

- Relative Valuation (RV)

- EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) measures a company's operating performance by excluding non-cash and non-operating expenses.

- It is not recognized under GAAP or IFRS, but it provides an apples-to-apples comparison between companies within the same industry.

- EBITDA is commonly used in valuation methods like DCF, ABV, and RV, especially for large private companies and those with negative net income.

- While EBITDA is valuable, it has limitations, such as not accounting for debt financing and depreciation of assets.

- EBITDA should be viewed in conjunction with other financial metrics and compared with peers in the same industry for a complete assessment of a company's financial health.

EBITDA Formulas and Calculation

EBITDA stands for Earnings Before Interest, Taxes, Depreciation and Amortization. It is calculated by taking the company’s net income and then adding back any:

- Interest Expense

- Taxes

- Depreciation

- Amortization

An easy way to remember this is to add back all of the items in the acronym, which are particularly useful when calculating EBIT or EBT. The starting point for EBITDA can be either operating income, which is gross revenue minus operating expenses, or net income, which is the last line item on the income statement.

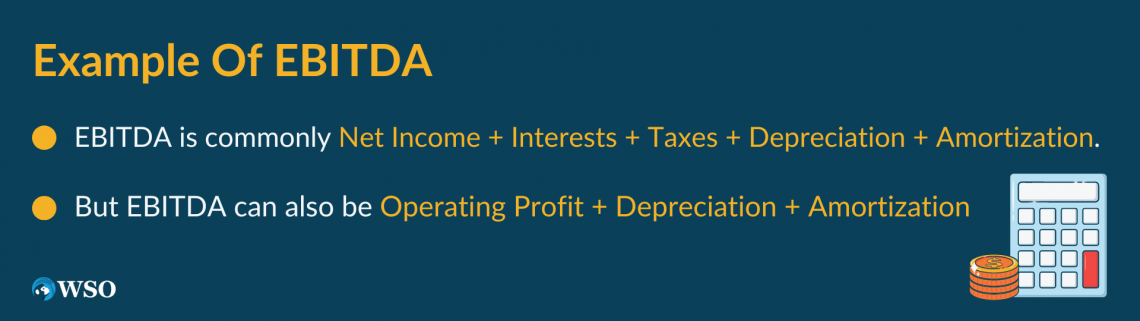

EBITDA formula using net income:

EBITDA = Net Income + Interest Expense + Taxes + Depreciation & Amortization

EBITDA using operating income:

EBITDA = Operating Income + Depreciation & Amortization

The reason for adding interest expense, taxes, depreciation and amortization back to net income is as follows:

In calculating EBITDA, interest is added to net income because all companies have different capital structures (companies are financed differently), which leads to varying interest expense amounts (payment to holders of a company’s debt). Interest expense is also tax deductible.

Taxes are added back because, depending on where a company operates, companies are subject to different tax rates.

Tax rates and taxes paid may not be a fair reflection of how a company is performing relative to its peers because even if two companies are in the same industry, they may generate their revenues in different parts of the world, which means they will be subject to different tax rates.

Depreciation and amortization are added back to net income because the amount of depreciation on a tangible asset, such as a company car, and the amount of amortization on an intangible asset, such as a patent, will vary based on the asset and the assumptions used.

For instance, one company may have a building that is being depreciated, while another may only have one company car. The reported depreciation amounts will be very different.

EBITDA In Valuation

EBITDA is commonly used in:

1. Discounted cash flow (DCF) analysis when comparing the relative value of companies because it provides an apples-to-apples comparison between companies by eliminating the effects of interest expenses, taxes, depreciation, and amortization.

To value large privately held companies.

The valuation of companies with negative net income that have a positive EBITDA.

When used in relative value comparisons, a common multiple that is used is enterprise value to EBITDA, commonly known as EV/ EBITDA.

2. Enterprise value (EV) is equal to the market value of a company’s debt and equity minus cash and cash equivalents. Since EV ignores the capital structure of the company, EBITDA happens to be its best value driver, as it also removes the effects of differences in capital structure.

Below is the formula for enterprise value to EBITDA.

Enterprise Value to EBITDA = EV / EBITDA

where,

EV = Market Capitalization + Debt + Minority Interest + Preferred Shares – Cash & Cash Equivalents

and

EBITDA = Net Income + Interest Expense + Taxes + Depreciation & Amortization

Why Use EBITDA?

Oftentimes, companies will have different capital structures and negative net income. This can create issues in valuations and company comparisons.

Discounting negative cash flows will likely lead to a poor valuation for a high growth company. For example, Spotify Technology SA, a music and podcast streaming platform, posted a negative net income of $208.2 million as of December 2019, but a positive EBITDA of $36.94 million in the same period.

EBITDA, especially when used in an enterprise value multiple, provides an apples-to-apples comparison between companies within the same industry because it eliminates the effects of depreciation, interest expense, and taxes.

When used with enterprise value, in EV to EBITDA, and compared across different companies or a benchmark, it can tell an analyst if a company is over-, under-, or fairly valued. Generally a higher EV to EBITDA versus its peers will indicate that a company is overvalued. A low multiple will indicate that a company is undervalued, and may be a potential takeover target for an acquirer.

EBITDA, when combined with other financial metrics, can provide valuable multiples. Two of these multiples are:

- Enterprise Value to EBITDA (EV / EBITDA): Measures how much a firm may need to pay over EBITDA to acquire the target company.

- Debt to EBITDA (Debt / EBITDA): Measures a company’s ability to pay its outstanding debt obligations based on the income that is generated from normal operations.

EBITDA And Leveraged Buyouts (LBO)

A leveraged buyout (LBO) is when a company, usually a private equity (PE) firm, acquires another using a large amount of leverage (debt) to finance the purchase. The company being acquired is usually referred to as the target company, and the company purchasing the target company is called the acquirer.

The target company is usually valued based on EBITDA because it tells the acquirer how much money the target company can generate through its normal operations, regardless of any current assets or liabilities associated with it.

EBITDA can be used in enterprise multiples, such as EV to EBITDA, to tell the acquirer how many multiples over EBITDA the target company will be acquired for.

Let’s imagine a potential target company that is currently revolutionizing kitchen appliances has a negative net income of $100 million. An acquirer believes that under new guidance, the target company could start to turn a profit.

The acquirer calculates EBITDA to be $30 million. This is the amount the target generates from selling kitchen appliances before paying for interest expenses, taxes, and depreciation.

The acquirer now calculates the target’s enterprise value (EV) to be $40 million. Using an enterprise multiple (EV / EBITDA), the acquirer calculates a multiple of 1.33x.

This means that the acquirer will need to pay 1.33 times over EBITDA to acquire the target company. This metric can now be compared across other such companies to analyze if it is under, fairly or over-paying for the transaction.

The Drawbacks Of EBITDA

Although EBITDA provides useful information for valuation and relative comparisons, it does have its limitations.

Some of the limitations are:

- The first is that it does not take into account the cost of debt financing. In other words, EBITDA only looks at earnings or profits before interest and taxes, not after. If a company is highly leveraged, and its interest expense is significant, EBITDA will not capture the effects of these payments.

- Another drawback is it doesn’t take into account depreciation or amortization of a company’s assets. For instance, if a car rental company whose main source of revenue is from car rentals isn’t depreciating its cars then EBITDA may not be a reliable metric because depreciation expenses would likely be substantial. Relying on EBITDA, in this instance, could distort the company’s valuation.

- EBITDA is also not recognized by GAAP or IFRS, the two largest accounting bodies, thus making it a non-GAAP measure. An analyst must pay special attention and not base their decision solely on the value of EBITDA since EBITDA may make a company look less expensive and more attractive than it really is.

In summary, while EBITDA can be a good way to measure the financial health of a company, there are some drawbacks to be aware of.

EBITDA Vs. EBIT Vs. EBT

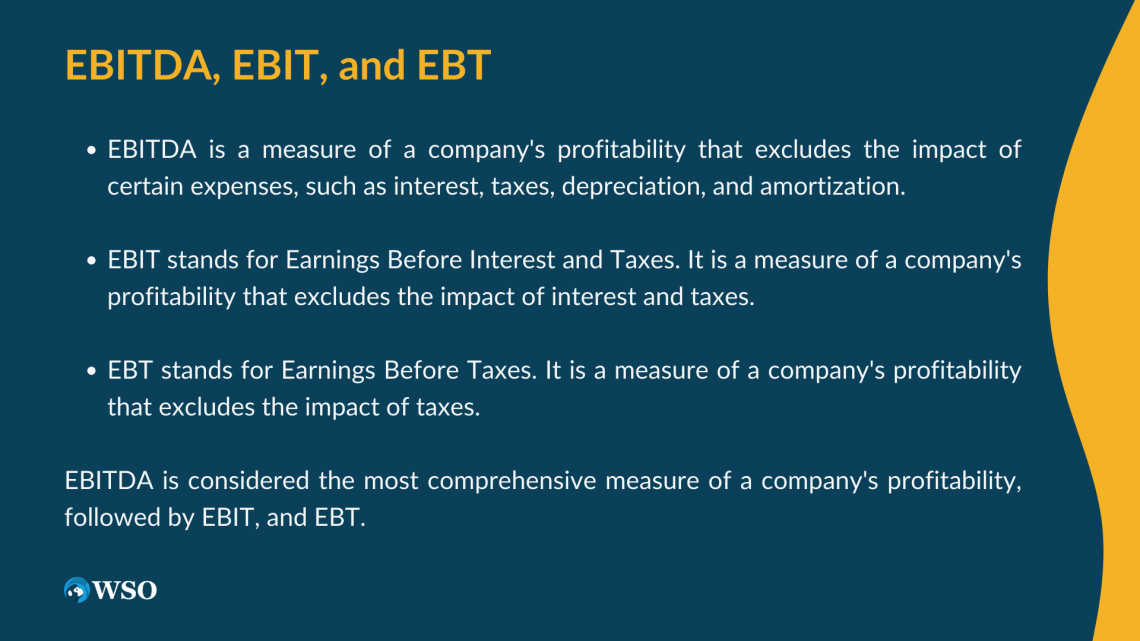

EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. EBIT and EBT are both components of EBITDA, but they focus on measuring different aspects of a company’s operating income.

EBIT stands for Earnings Before Interest and Taxes. EBIT is commonly known as a company’s operating income because it focuses on measuring a company’s ability to generate income prior to accounting for taxes and interest expenses.

It is essentially a company’s operating income after accounting for the effects of depreciation and amortization. By netting out depreciation from EBITDA to arrive at EBIT, it accounts for a company’s depreciation expenses, which is one of the drawbacks of using EBITDA.

Below is the formula for EBIT:

EBIT = Net Income + Interest Expense + Taxes

If we refer back to our example using a rental car company, EBIT would be a better metric to use since it accounts for the depreciation of the fleet of cars, which would likely be substantial.

EBT stands for Earning Before Taxes. It focuses on a company’s profitability after accounting for interest expense, depreciation, and amortization.

By accounting for the effects of interest expense and depreciation, an analyst can see how these expenses affect a company’s operating income, which addresses two of the limitations of using EBITDA.

Below is the formula for EBT:

EBT = Net Income + Taxes

EBT would be useful if an analyst is looking at a company with a highly leveraged capital structure and has a lot of fixed assets or intangible assets, such as patents, that require a significant amount of depreciation or amortization expenses.

It would allow the analyst to view the company's operating income prior to accounting for taxes, which will vary depending on where the company does business.

What Is A Good EBITDA?

EBITDA provides information on a company’s earnings prior to netting out depreciation of a firm’s assets and payments of interest and taxes. A higher EBITDA is preferred over a lower one, but if a company is highly leveraged, then EBIT or EBT might be a better measure of a company’s profitability.

EBITDA, like other financial metrics, should be viewed in tandem with other financial metrics and ratios to get a complete view of the financial health of a company.

It is also important to compare the EBITDA of the company being valued to the EBITDAs of the company’s peers in the same industry.

For instance, the EBITDA of a financial technology company will likely be drastically different when compared to the EBITDA of a car manufacturer.

For example, the EBITDA for Block, Inc., for the fiscal year ending in December 2020, was $323 million, while the EBITDA for Ford Motor Company was $2.9 billion for the same period. A significant portion of the difference arose from the difference in depreciation and amortization.

Block’s depreciation and amortization was $154.5 million, and Ford’s was $7.45 billion.

Example Of EBITDA

Let’s assume a new high-growth online car manufacturer has a net income of $5 million in the current period.

An analyst would like to calculate EBITDA for this company and simultaneously calculate its EV to EBITDA ratio. It currently has an enterprise value (EV) of $20 million.

In order to calculate the company’s EBITDA, the analyst would need to add back interest expense, taxes paid, and any depreciation and amortization to net income. All amounts below are in US Dollars (USD).

| Particulars | Amount (USD) |

|---|---|

| Net Income | 5,000,000 |

| Interest Expense | 1,000,000 |

| Taxes Paid | 400,000 |

| Depreciation & Amortization | 300,000 |

| EBITDA | 6,700,000 |

If you recall, EBITDA is equal to:

EBITDA = Net Income + Interest + Taxes Paid + Depreciation & Amortization

So in this case, the formula would be:

6,700,000 = 5,000,000 + 1,000,000 + 400,000 + 300,000

Now to calculate EV to EBITDA, we will divide the company’s EV of $20 million by EBITDA of $6.7 million, which we calculated above. The formula for EV to EBITDA is below:

Enterprise Value to EBITDA = EV / EBITDA

EV to EBITDA for the online car manufacturer is equal to:

2.99x = 20 million / 6.7 million

An EV to EBITDA of 2.99x means that an acquirer would need to pay 2.99 times over EBITDA to purchase the online car manufacturer.

When evaluating the attractiveness of a company, it is important to consider other multiples and metrics of the target company and compare these multiples with companies in the same industry.

Let’s also calculate the company’s EV to EBIT and EV to EBT to see what impact depreciation and taxes have on EBITDA.

EBIT for the company is equal to $6.4 million. The calculation is below.

EBIT = Net Income + Interest Expenses + Taxes Paid

6,400,000 = 5,000,000 + 1,000,000 + 400,000

EV to EBIT for the online car manufacturer is equal to:

3.13x = 20 million / 6.4 million

Since depreciation and amortization is removed from the EBIT calculation, the denominator in EV to EBIT becomes smaller. The company has an EV to EBIT of 3.13x, which means an acquirer would need to pay 3.13 times over EBIT to acquire the online car manufacturer.

EBT for the company is equal to $5.4 million. The calculation is below.

EBIT = Net Income + Taxes Paid

5,400,000 = 5,000,000 + 400,000

EV to EBT for the online car manufacturer is equal to:

3.7x = 20 million / 5.4

Since EBT nets out interest expense and depreciation and amortization, the denominator for EV to EBT decreases, bringing the multiple to 3.7x.

As variables, such as interest expense and depreciation, are removed from EBITDA, we can see the impact they make on our multiples.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?