After Tax Operating Income (ATOI)

It is considered a rough estimate of cash flows after tax without the tax benefit of debt.

What Is After Tax Operating Income (ATOI)?

After-tax Operating Income (ATOI) is the company's total income after paying taxes. GAAP does not recognize the ATOI since it excludes the after-tax benefits from accounting changes.

As it's not based on GAAP, what's included and left out of the measure varies between companies and industries. As a result, It's crucial to understand how the company under examination obtained its ATOI.

After-tax operating income is a way to determine how well a business is running because it only looks at costs directly related to running it. For example, it doesn't include interest expense, which is affected by how the company uses debt, dividends, or nonrecurring items.

After-tax operating income shows how much of a company's income will be turned into profit in the long run and how much money a company can make from its operations during a certain time.

ATOI is considered a rough estimate of cash flows after tax without the tax benefit of debt. If a company has no debt, its ATOI will equal its net income after taxes (NIAT).

- After-tax operating income is the company's total revenue after taxes have been deducted.

- After-tax operating income is a method for determining the efficiency of a firm because it only considers costs directly relevant to the operation of the business.

- After-tax operating income is better for investors because it considers taxes and other one-time things that can change operating income.

- Operating and net income both show how much money a company generates. However, they are two very different ways of expressing a company's earnings. Income is the money from normal business operations, whereas net income is the company's total income.

- In contrast to the calculation of net operating profit after taxes (NOPAT), the ATOI does not include interest expenses like the company's decisions to use leverage, which could affect the bottom line.

Understanding After Tax Operating Income (ATOI)

Operating income after taxes is also known as earnings before interest and after taxes (EBIAT). It measures a company's profitability without considering how much money it has (debt to equity).

A business's profit and loss statement shows its operating and non-operating income and expenses over a certain period. Operating income is based on a company's core market, where most of its money comes from.

For example, a manufacturing company's main revenue is created by the company's primary products. Therefore, they will only be left with their operating income after deducting direct and indirect costs.

Operating income is calculated similarly to after-tax operating income. However, it also considers taxes, operational costs, and other significant deductions.

Overall, the term after-tax operating income refers to the operating income of a corporation after tax deductions. However, this statistic does not consider the after-tax benefits of accounting changes.

This measure is calculated similarly to operating income. It is close to the after-tax net operating profit. Nevertheless, the computations may vary significantly.

The Formula of After-Tax Operating Income

After-tax operating income is the corporation’s income generated by its operation. Therefore, it is the company's income after subtracting the direct and indirect expenses.

The after-tax operating income is calculated by subtracting operating expenses and depreciation from the company’s gross revenue. After-tax operating income can be calculated by using the following formulas:

After-tax operating income = (Gross income - Operating expenses - Depreciation) - Taxes

Or

After-tax operating income = Earnings before interest and tax (1 - Tax) + depreciation

Where,

- Gross income: The total income earned by a business before taxes and other outgoing costs is deducted. Earning covers all sources of income and is not only limited to money received in cash but also goods or services received.

- Operating expenses: A company has to pay costs to keep its operations going, such as salaries for employees and supplies for the office. It is referred to as selling, general, and administrative costs (SG&A), which are costs related to running a firm. They also cover costs for marketing, computer equipment, employee benefits, rent, and utilities.

- Depreciation: The expected decline in the value of a fixed asset within a fiscal year. In accrual accounting, calculating depreciation is a way to determine the rate of decline over an asset's useful life. For example, assets lose value over time due to company usage, so companies calculate depreciation expenses to assess their asset-related costs for generating revenues.

- Taxes: Sum of money that individuals/businesses must pay to the government based on various factors, including income level, property worth, etc. The government levies taxes to finance the government and public expenses.

- Pre-tax operating income: Pre-tax Operating income is the first part of the formula (Revenue, operating expenses, and depreciation) and is also known as the pre-tax operating income. It reflects the differences between the company’s operating revenue and direct expense and doesn’t account for taxes.

Pre-tax operating income = Revenue - Operating expenses - Depreciation

Illustrative Example of ATOI

Here is an example:

A TYL company reports the following information:

- Revenues: $10 million.

- Cost of goods sold: $6 million.

- Gross profit: $4 million.

- Operating expenses: $2 million.

- Depreciation: $0.6 million.

- Taxes: $0.4 million.

What is the company’s ATOI?

After-tax operating income = (Gross revenue – Operating expenses – Depreciation) – Taxes

= ($4 million - $2 million - $0.6 million) - $0.4 million

= $1 million

Net Income vs. Operating Income

Operating and net income show how much money a company generates. Still, they are two very different ways of expressing a company's earnings. Operating income is the revenue generated through business operations, while net income represents the final business's income.

Net income is the amount remaining after all expenses have been deducted. It differs significantly from gross income, which removes the cost of products sold from revenues. It is known as the bottom line, as it can be found at the bottom of the company’s income statement.

Net income measures a company's profitability since it allows investors to judge if it earns more than it spends. Net income can be estimated by considering numerous important indicators that investors should be aware of, such as COGS, interest, and tax.

Net income is calculated by subtracting expenses, including taxes, interest, depreciation, and other expenses, from the company’s revenue, as shown in the following formula:

Net income = Revenue - Cost of goods sold - Interest - Tax - Operating and other expenses.

Operating income is a firm's profit after deducting variable and fixed operating expenses, such as the cost of managing day-to-day operations, paying rent and employees, depreciation and amortization, and the cost of goods sold.

Operating income helps investors to examine a company's operating performance by removing interest, taxes, and other expenses from operating income.

It covers selling, general, and administrative expenses (SG&A), expenses incurred by a business to maintain its operations. SG&A includes costs for marketing, computer hardware, staff perks, rent, and utilities.

Operating income is calculated by using the following formula:

Operating Income = Gross Income – (COGS + Operating Expenses + Depreciation and Amortization)

Here is an example:

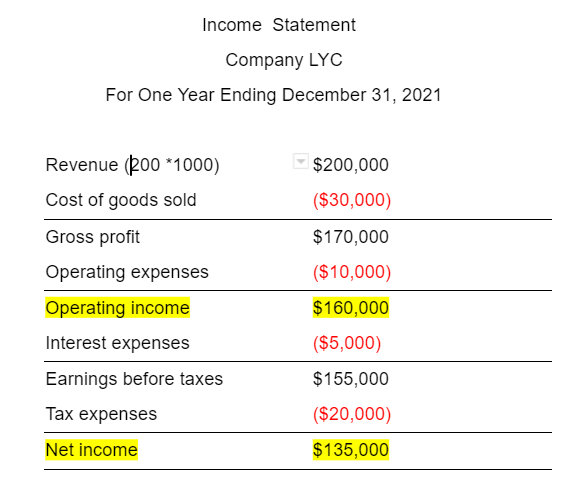

Suppose company LYC reports the following numbers for one year ending December 31, 2021:

- Revenue = 200 units.

$1000 for each unit sold. - Cost of goods sold = $30,000.

- Operating expenses = $10,000

- Tax expenses = $20,000.

- Interest expense = $5,000.

Create an income statement of the company and calculate the company’s operating and net income:

ATOI Vs. NOPAT

Contrary to the net operating profit after tax (NOPAT) calculation, the ATOI does not include interest expenses such as the company's leverage decisions that might affect the company’s bottom line.

ATOI is a hybrid metric that allows analysts to assess firm performance without considering debt. As a result, it provides a more precise assessment of pure operating efficiency.

It assesses the whole operating efficiency of a business, as the calculation considers expenses directly related to the business's activities. It excludes dividend payments and nonrecurring items, as they are not part of the business's usual operations.

On the other hand, Net operating profit after tax (NOPAT) is a company's cash earnings if it has no debt. This financial measure excludes one-time charges and losses, which do not accurately reflect a company's underlying profitability. Therefore, NOPAT is known as operating income and profit.

NOPAT offers analysts a measure of a company's basic operating efficiency without the impact of debt, mergers, and acquisitions. Analysts used this measure to calculate the firm's free cash flow (FCFF), which is equal to net operating profit after taxes minus changes in working capital.

In addition, it is utilized in calculating economic free cash flow to the firm (FCFF), which equals net operating profit after taxes minus capital.

A company’s charges may be related to a merger or acquisition (M&A), which may affect its bottom line for the year but do not necessarily provide an accurate picture of its operations.

Net operating profit after tax can be calculated by using the following formula:

NOPAT = Operating Income × ( 1 − Tax Rate )

Operating income is calculated by taking the differences between net income and operational expenses, including selling, general, and administrative expenses.

Here is an example:

Suppose company TYC reports the following information for one year ending December 31, 2021:

EBIT: $12,000.

Tax rate: 40%.

The net operating profit after tax: $7,200

Calculate the company’s net operating profit after tax:

NOPAT = Operating Income × ( 1 − Tax Rate )

= $12,000 * (1 - 0.40)

= $12,000 * (0.4)

= $4,800

or Want to Sign up with your social account?