Leverage

It is the use of borrowed money to enhance the returns of any investment

What Is Leverage?

Leverage is a finance concept used by firms that borrow money to maximize profits and increase cash flows and assets. However, this strategy can also involve the company losing money, as borrowing money comes with some risks.

It is when firms use credit to increase their return on cash. They may either get funding from a direct lender or issue fixed-income securities. The firms can invest more capital and get greater returns using credit.

Many individuals have dealt with this concept. When people buy houses, they generally use them too. Only a few people buy a house using cash; most of the time, people take out a loan (a type of credit).

They could afford a more expensive house than they would if they were only using cash. In the future, this will likely increase the returns they can get from selling the house – if they choose to do so.

There are two types in finance:

- Financial

- Operating

Operating involves the measurement of the relationship between the growth of revenues and profits. On the other hand, financial leverage has more to do with a company's debt to increase its assets. Both types can be very lucrative for businesses that implement each strategy, but each has risks, such as insolvency.

These are commonly seen in financial transactions like LBOs. LBOs require a financial sponsor to acquire a company using a significant debt. The more debt a financial sponsor can use, the more potential returns they can make.

Firms must ensure they have strong cash flows before acquiring this debt because they are forced to declare bankruptcy if they cannot pay the interest and principal payments.

- Leverage in finance refers to the use of borrowed funds to increase the potential returns on investments. It can be a powerful strategy for maximizing profits but comes with risks.

- There are two main types of leverage discussed: financial leverage (FL) and operating leverage (OL).

- Leverage can amplify both profits and losses. High financial leverage can lead to significant returns, but it also increases the risk of insolvency if the interest expenses on debt become overwhelming.

What is Financial Leverage (FL)?

A company using more debt financing will have higher FL. With this added cash from taking out different types of debt, firms can increase their returns by making greater investments. These returns must offset the interest expense from the debt to increase net income.

When implementing this strategy, firms increase their market purchasing power. They can complete deals and transactions that are more sizeable than possible by only using equity.

Individual investors can also take advantage of this concept. For example, investors can leverage their investments by using different financial instruments, such as options, margin accounts, and futures – resulting in the investor using credit to fund investment decisions.

Investors may not be comfortable levering their investments directly but may want to indirectly. This would involve investors investing in companies that use it to finance their business operations.

Note

There are many different ratios to calculate leverage. Still, the most common are:

- Debt-to-Assets (Total Debt / Total Assets)

- Debt-to-EBITDA (Total Debt / Total Equity)

- Equity Multiplier (Total Assets / Total Equity)

These ratios are a more standardized way to compare the different capital structures of firms without worrying about the firm's size. However, it's important to remember that different industries may warrant different financing compositions so ratios may be drastically different.

Financial Leverage Example

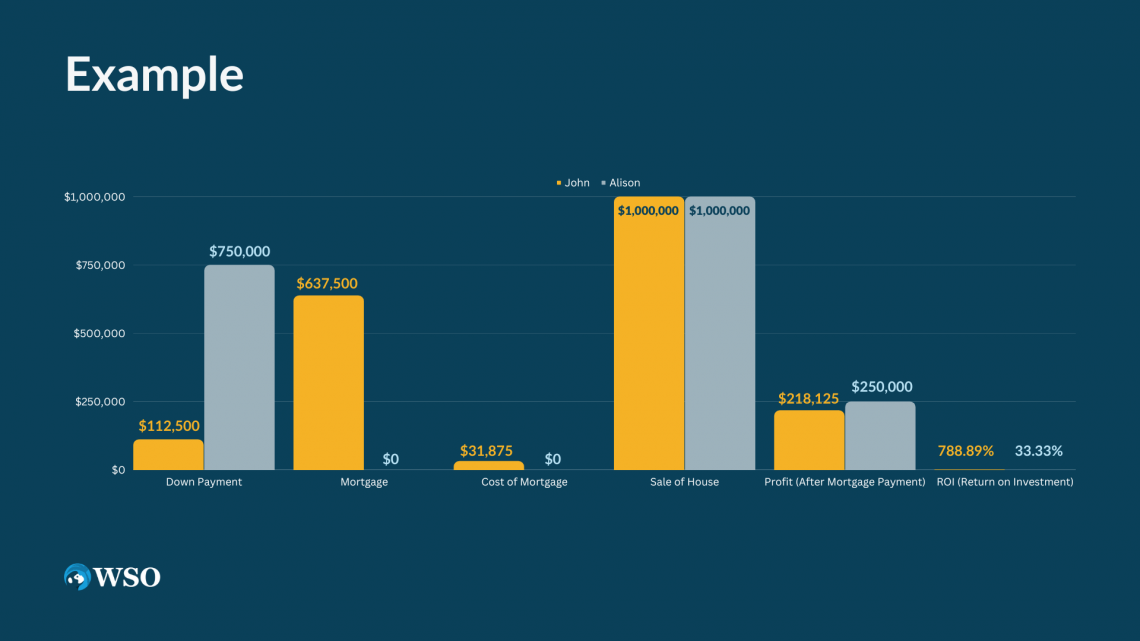

John and Alison are in the market for a house. They are both interested in buying the same house for $750,000. John plans on making a down payment of 15% and taking out a mortgage on the remaining $637,500 (the mortgage payments are 5% annually).

On the other hand, Alison wants to avoid taking out a mortgage. She is willing to pay the entire $750,000 in cash for the house. Will John or Alison realize a higher return on their investment if they were to sell the house in a year from the point of their acquisition for $1,000,000?

| John | Alison | ||

|---|---|---|---|

| Down Payment | $112,500 | $750,000 | |

| Mortgage | $637,500 | $0 | |

| Cost of Mortgage | $31,875 | $0 | |

| Sale of House | $1,000,000 | $1,000.000 | |

| Profit (After Mortgage Payment) | $218,125 | $250,000 | |

| ROI (Return on Investment) | 788.89% | 33.33% | |

In this example, we see Alison made a higher profit than John. Still, John was able to make a way higher return on investment. This is where a lot of people get tripped up.

John could have a greater ROI because he didn’t invest much money in the house. Most of the money that he paid for the house was in debt. So, with a sale of $1 million ($1 million in cash), John made almost eight times the amount of money he put in.

On the other hand, Alison put in $750,000 in cash on her investment. So the cash she got from the sale was only 1.3 times the amount she put into the house.

This is the key difference: John had high leverage, while Alison had none. As a result, John could use a lot of cheap debt to increase his return, while Alison didn’t have any debt, resulting in a much smaller return.

High Financial Leverage risks

Although a company can profit greatly from using credit to fund its investments, it can also suffer through different expenses associated with using credit. Interest expenses can start to add up and overwhelm the borrower (the company).

There are just as many cons for all the pros of using this approach. Here is a list of risks a company faces when it wants to incur debt to try and make a healthy return:

1. Stock Price Volatility

A company's profits may also be unstable when the stock price is unstable. The changes in the stock price will result in the accounting of employee-owned stock options needing to be easier. As a result, these firms will pay higher interest to shareholders.

2. Defaulting/Bankruptcy

When the barriers to entry in an industry are low, the revenues and profits of that market will be more volatile than in a high barrier-of-entry industry.

This volatility could hurt a company if it makes a firm unable to meet its debt obligations and pay its expenses. In addition, firms that cannot pay their lenders may file a bankruptcy case and collect collateral if the debt is secured.

3. Lenders' skepticism of issuing more debt

Lenders conduct due diligence to ensure firms meet their debt obligations when lending debt to firms. Lenders may be less likely to provide additional funds if a company has a high debt-to-equity ratio.

This is because the lender wants to avoid providing funds to a firm likely to default and not pay the lender back. If lenders provide funds to these types of firms, it will result in high-interest rates to protect against default risk.

Note

Leverage may have been a big influencing factor in the 2008 Global Financial Crisis. Some experts believe that firms and lenders got too greedy and didn’t want to settle for moderate returns. Instead, they had extremely levered positions, resulting in the market suffering when their levered investments didn’t realize.

What is Operating Leverage (OL)?

When a company has fixed operating costs and high revenues and profits, the company will have a high OL. Unfortunately, this means the company will have to expense many fixed monthly expenses regardless of its profitability.

Firms with low OL won’t have as many fixed operating costs. Instead, they will have high costs correlated to the sales they make.

It can also be used to determine a firm’s break-even point. This can lead to the firm pricing their products appropriately to cover all their expenses and still make a profit.

Fixed costs can be both beneficial and detrimental to businesses. On the one hand, a company will always know the costs they have each month, as the costs don’t change.

On the other hand, the company may experience economies of scale as it can spread fixed costs across many products.

The cons are, as mentioned above, the costs are there regardless of how the business does financially. The business could not sell any products and would still experience the same costs if it had record monthly sales.

Note

Companies need to have good cash flow so they don’t run into this problem and end up operating at a loss due to fixed expenses.

Operating Leverage Example

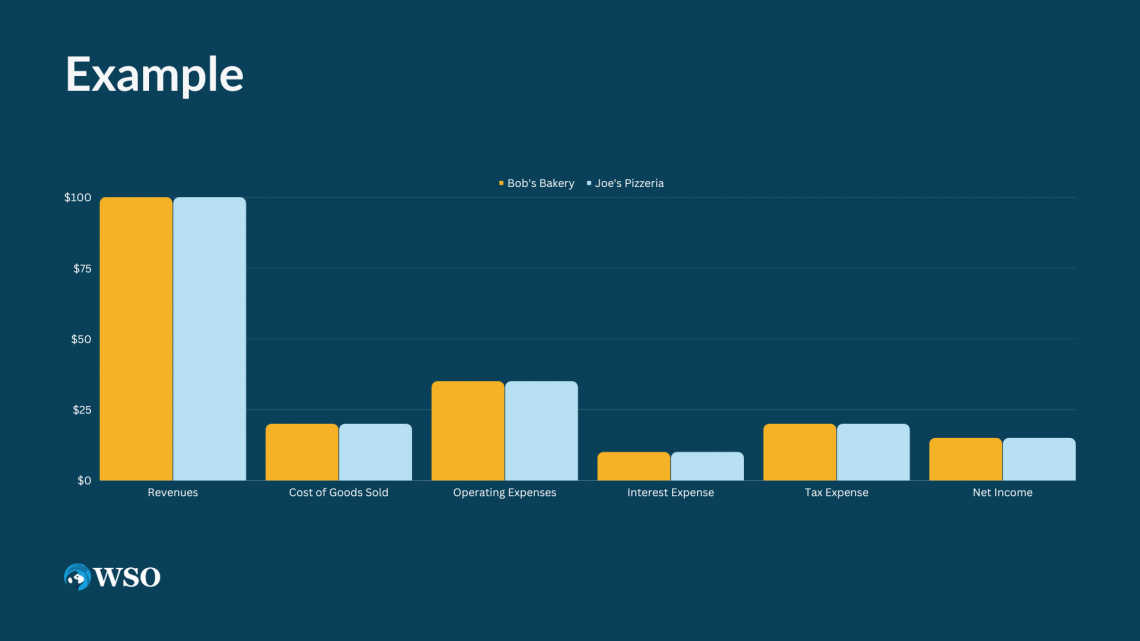

Imagine there are two companies: Joe’s Pizzeria and Bob’s Bakery.

The income statement of the two companies is the same. The only difference between the two companies is the type of expenses they face.

Joe’s Pizzeria faces lots of variable expenses (35% of revenue), while Bob’s Barkey faces fixed expenses of $35.

| Bob’s Bakery | Joe’s Pizzeria | ||

|---|---|---|---|

| Revenues | $100 | Revenues | $100 |

| Cost of Goods Sold | $20 | Cost of Goods Sold | $20 |

| Operating Expenses | $35 | Operating Expenses | $35 |

| Interest Expense | $10 | Interest Expense | $10 |

| Tax Expense | $20 | Tax Expense | $20 |

| Net Income | $15 | Net Income | $15 |

While the income statements are the same now, they won’t be the same given the revenue changes.

If the revenue increases by $20, Bob’s Bakery will have a higher net income because of its higher OL. Bob’s operating expenses will stay the same since they’re fixed costs, while Joe’s will increase since they are directly correlated to revenue growth.

| Bob’s Bakery | Joe’s Pizzeria | ||

|---|---|---|---|

| Revenues | $120 | Revenues | $120 |

| Cost of Goods Sold | $20 | Cost of Goods Sold | $20 |

| Operating Expenses | $35 | Operating Expenses | $42 |

| Interest Expense | $10 | Interest Expense | $10 |

| Tax Expense | $20 | Tax Expense | $20 |

| Net Income | $35 | Net Income | $28 |

On the other hand, if the revenues decrease by $20, Joe’s Pizzeria will now have a higher net income. Since Joe’s operating expenses are tied to revenue growth and revenue is decreasing, Joe’s operating expenses are also decreasing. Bob’s are staying the same, resulting in a lower net income.

| Bob’s Bakery | Joe’s Pizzeria | ||

|---|---|---|---|

| Revenues | $80 | Revenues | $80 |

| Cost of Goods Sold | $20 | Cost of Goods Sold | $20 |

| Operating Expenses | $35 | Operating Expenses | $28 |

| Interest Expense | $10 | Interest Expense | $10 |

| Tax Expense | $20 | Tax Expense | $20 |

| Net Income | ($5) | Net Income | $2 |

While in this scenario, Bob’s Bakery is coming in at a loss; Joe’s is still making a profit. This example shows that while having expenses as fixed costs can be very lucrative for a business, they can also hurt the business, given the right scenario.

Leverage FAQs

Highly financial levering refers to when a firm borrows a lot of debt to complete different business functions of the company (i.e., different transactions such as acquisitions).

Firms can make a lot more profit when they use cheap debt and a limited source of their cash. This is prevalent in deals like LBOs, where financial sponsors buy companies with large debts to make high returns.

Financial deals with firms taking out debt and using it to create levered transactions to maximize cash returns. At the same time, operating has to do with the operating cost of a business – whether or not the operating expenses are fixed or variable.

Some risks can be associated with the business if they have less debt or fixed operating costs. Conversely, if businesses have a lot of debt and experience cash flow problems, firms may default on their credit and go bankrupt.

Firms may also be unable to take out more loans if their debt-to-equity ratio is too high, which could be a problem in the future if they need cash.

Also, if there is an economic downturn or the firm’s cash flows are cyclical, they may have problems paying their operating expenses if they’re fixed costs. If they make significantly less money than expected, they are still obligated to pay these costs at the same price.

or Want to Sign up with your social account?