Discounted Cash Flow (DCF)

Primary valuation methods used by finance professionals to derive a company's fair value

What is Discounted Cash Flow (DCF)?

Discounted cash flow, commonly known as DCF, is a valuation method used to assess the worth of securities, mergers and acquisitions (M&A) deals, and other assets. It has been around since as early as the 1700s.

Discounted cash flow was significantly developed and popularized by American economist John Burr Williams in his book, The Theory of Investment Value, published in 1938. Williams' work laid the foundation for modern DCF analysis, emphasizing the importance of cash flows and their present value in investment valuation.

However, DCF did not gain popularity until the 1980s when U.S. courts began using it. Today, professionals in many financial fields like investment banking, corporate finance, private equity, and more use DCF.

- Discounted cash flow is a valuation method used by financial professionals to assess potential investments.

- DCF uses the present value of future cash flows to calculate the intrinsic value of an investment. The major components are the time value of money, future cash flows, discount rate, and terminal value.

- The steps are calculating the future free cash flows, selecting a discount rate (typically WACC), estimating terminal value, and summing the present value of cash flows.

- DCF's greatest advantage is its ability to determine a company's intrinsic value. However, the amount of assumption and its sensitivity to parameter changes can significantly affect the accuracy.

- Since DCF is the industry standard, professionals often pair it with other valuation methods to ensure accuracy. Other methods include comparable company analysis and comparable transaction analysis.

Understanding Discounted Cash Flow

Discounted cash flow is a valuation method used to determine whether an investment should be made using the expected future cash flows. DCF discounts a company's cash flows to the current day using a discount rate. This is based on the idea of the time value of money.

The key components to understand DCF are cash flows, discount rate, time value of money, and the terminal value:

- Cash Flow: The money that goes in and out of a business. This comprises both cash spent and cash received. DCF uses the predicted future cash flows when making a valuation.

- Discount Rate: The rate at which companies discount their future cash flows to the present value. Often, the weighted average cost of capital (WACC) is used as the discount rate. WACC is the average amount of money companies spend to finance their operations.

- Time Value of Money: The idea that the same amount of money is worth more in the present than in the future. This is because of the ability to invest in the present, creating value in the future. In addition, money loses purchasing power in the future because of inflation.

- Terminal Value: A business’s present value at any point in the future. An expected constant growth rate is used.

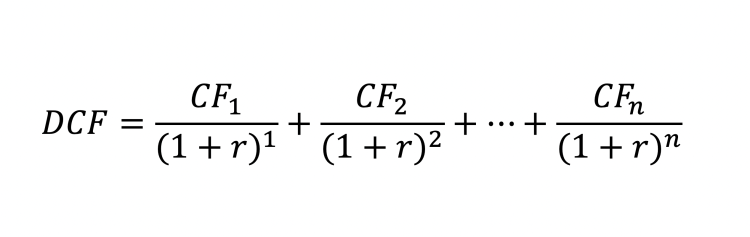

DCF Formula

These components are necessary under the formula for discounted cash flow. Discount Cash Flows formula is:

DCF = CF1/(1 + r)1 + CF2/(1 + r)2 + … + CFn/(1 + r)n

Where

- CF1: Predicted Cash Flow in Year 1

- CF2: Predicted Cash Flow in Year 2

- r: Discount Rate

- CFn: Predicted Cash flow for additional years.

This allows financial professionals to estimate the intrinsic value of an investment or company. When the present value of the future cash flows is more than the cost of the investment, it may be worth it.

How is DCF calculated?

Knowing the key components of DCF and its formula is essential to calculating discounted cash flow. There are five major steps:

- Forecasting cash flows

- Selecting the discount rate

- Calculating terminal value

- Summing present values

- Calculate Stock Price if applicable

Forecast cash flows

The first step is forecasting future cash flows. It is best to estimate 5 to 10 years into the future. To do this, one must consider all the future cash inflows and outflows.

Inflows usually come from investing, revenue, and other financing. Outflows are any time money leaves the business; think expenses, taxes, dividends, and debt repayments. To forecast cash flows, subtract outflows from inflows.

It is important to consider the type of company and its future goals and consult various department members.

Calculating the Discount Rate

When calculating the discount rate, WACC is the most commonly used method. Other discount methods used are the cost of debt, risk-free rate, cost of equity, and hurdle rate.

Since WACC is the most popular, it is essential to have a firm grasp of its formula.

WACC can be calculated by using the formula:

WACC = E/ (D + E) * (re) + D/ (D + E) * (rd) * (1 - t)

Where

- E = Market Value of Equity, calculated by multiplying the total number of shares outstanding by the current stock price

- D = Market Value of Debt, the amount at which all of a company's debt can be bought or sold

- re = Cost of Equity, the amount of return investors require to compensate for the risk of buying a stock

- rd = Cost of Debt, the interest rate or yield that debt investors require loaning their money to a company

- t = Corporate Tax Rate that varies from state to state; as of 2023, North Carolina had the lowest at 2.5%, whereas New Jersey had the highest at 11.5%. The federal rate is 21%.

Calculating the Terminal Value

Remember, this is used to estimate FCF after five or ten years. There are two methods by which terminal value may be calculated:

1. Perpetuity Growth

An assumption is that cash flows will grow infinitely at a constant rate after the forecast period. The growth rate is typically between 2 to 4%, which is the economy's growth.

The Formula to calculate the terminal value using perpetuity growth is:

TV = FCFn (1 + G)/ (WACC - G)

Where

- TV = Terminal Value

- FCFn = future cash flow at year

- G = perpetuity growth

- WACC = weighted average cost of capital

2. Exit Multiple Method

Values businesses based on similar businesses that have recently sold. The formula for exit multiple can be calculated by:

EV/ EBIT

Where

- EV = enterprise value

- EBIT = Earnings before interest taxes

To calculate the terminal value using exit multiple, use this formula:

TV = Final year EBITDA x Exit Multiple

Summing present values

This step is based on the idea of present value, which is the current worth of future money. To discount cash flows to year zero, use this formula.

PV = FCF1/ (1 + WACC)1 + FCF2/ (1 + WACC)2 + …. + FCFn/ (1 + WACC)n + Terminal Value/ (1 + WACC)x

The sum of the present value of future cash flows is the enterprise value of the company based on DCF.

Calculate Price per Share

This step is only used when evaluating stock price. To calculate the price per share, follow the formula below.

Step 1: Calculate equity value

EV - Long-Term debt = Equity Value

EV = Enterprise value by DCF

Step 2: Calculate share price

Equity Value / Shares outstanding = Price Per Share

DCF Example Calculation

Let’s take an example to understand the process better. Suppose we have XYZ Corp. Now, let’s do the DCF analysis.

Step 1: Project Cash Flows of XYZ Corp

| Year | Projected Cash flow |

|---|---|

| 1 | 1,000,000 |

| 2 | 1,250,000 |

| 3 | 1,750,000 |

| 4 | 2,100,000 |

| 5 | 2,500,000 |

Step 2: Calculate the discount rate using the WACC of XYZ Corp

- Market Value of Equity = $10 million

- Market Value of Debt = $5 million

- Cost of Equity = 10%

- Cost of Debt = 6%

- Corporate Tax Rate = 25%

WACC= (($10M/ ($10M + $5M)) * 10%) + (($5M/ (10M + 5M))* 6%) * (1 - 0.25)

WACC = 0.067 + 0.015

WACC = 0.082 or 8.2%

Step 3: Calculate the Terminal Value

Using the Perpetuity method:

- FCF5 = 2,500,000

- G = 3% (typically between 2 & 4%)

- WACC = 8.2%

TV = 2,500,000 (1 + 0.03)/ (8.2% - 3%)

TV = 2,575,000/ 5.2%

TV = $49,519,230

Step 4: Calculate the enterprise value by summing the discounted cash flows to year zero using WACC

| Year | 1 | 2 | 3 | 4 | 5 | Terminal |

|---|---|---|---|---|---|---|

| FCF | 1,000,000 | 1,250,000 | 1,750,000 | 2,100,000 | 2,500,000 | 49,519,230 |

| Pv | 925,925.93 | 1,059,405 | 1,377,410 | 1,571,601 | 1,735,526 | 33,391,626 |

Sum of Present Values = 40,061,493

Enterprise Value of the company based on DCF = 40,061,493

Step 5: Calculate Stock Price

For the model, let's assume the long-term debt is 15 million, and there are 10 million shares outstanding.

First, calculate equity value:

40,061,493 - 15,000,000 = 25,061,493

25,061,493/ 10,000,000 = $2.51

XYZ has a share price of $2.51

If the market price exceeds $2.51, XYZ is considered overvalued, and if it falls below, XYZ is deemed undervalued.

To learn more about valuing a stock through DCF, watch this video:

How does DCF compare to other Valuation Methods?

DCF is the industry standard among investment bankers and investment analysts for valuating companies, mergers, and other assets. It is important to understand that discounted cash flow is not the only method financial professionals use.

| Valuation Method | Description | Key Metrics | Main Application |

|---|---|---|---|

| Discounted Cashflow | Estimates the value of an investment based on expected future cashflow discounted to the present value. | Free Cash Flows Discount Rate Terminal Values |

Valuing companies, M&A deals, and other assets |

| Comparable Company Analysis (CCA) | Values a company by comparing it to other businesses in the same industry of a similar size. | EV/S P/E P/B P/S |

Determining if a company is overvalued or undervalued compared to its peers. |

| Comparable Transaction Analysis (CTA) | Compares the current company to a company in the same industry with a similar business model, primarily used for M&A valuation. | EV/EBITDA | Evaluating how much a company should pay for another company in a merger or acquisition. |

Discounted cash flow vs. comparable company

Analysts who use the comparable company analysis to value a company will find publicly traded companies and their existing price-to-earnings (or any other relevant multiple) ratios and compare them to the target.

Therefore, the DCF and comparable company analysis are very different valuation methods.

While the DCF takes a fundamental approach by finding an intrinsic value of the company, the comparable company analysis takes a technical approach by finding a relative bargain.

One benefit of the DCF over the comparable company analysis is that it does not rely on finding a similar company to conduct the research.

You'd be surprised how difficult it would be to find a comparison with similar assets or revenue streams when the target industry is very niche.

To learn more about the comparable company analysis, click here.

Discounted cash flow vs. precedent transactions

The precedent transactions analysis is considered a subset of the comparables company analysis. Precedent transactions are done by looking at the prices paid by investors to acquire similar companies.

This is different from looking at the market price because it focuses on specific transactions and their specifics, including the type of company, its size, and the type of buyer.

While a DCF can be calculated on every transaction, precedent transactions are much more relevant to analysts working on an M&A deal.

The approach in a precedent transaction is also more technical than fundamental, where you'd be trying to look at similar transactions and relate their value to the target.

To learn more about precedent transactions, click here.

How To Answer The "Walk Me Through A DCF" Question?

In an interview, it is essential to keep your technical overview high. Therefore, start with a high-level overview and be ready to provide more detail upon request.

- Project out cash flows for 5 - 10 years depending on the stability of the company.

- Discount these cash flows to account for the time value of money.

- Determine the terminal value of the company - assuming that the company does not stop operating after the projection window.

- Discount the terminal value to account for the time value of money.

- Sum the discounted values to find an enterprise value.

- Subtract Net Debt and divide by diluted shares outstanding to find an intrinsic share price.

Discounted Cash Flow Advantages and Disadvantages

Like all financial valuation methods, there are both advantages and disadvantages.

The advantages are:

- Very detailed: DCF requires an in-depth analysis of each factor that affects future free cash flow; this leads to a strong understanding of a company's financials and operations

- Determines intrinsic value: This shows if an investment is undervalued or overvalued.

- Easily modeled on Excel: It makes evaluating a company easy and efficient.

- Evaluate M&A and other assets: aids decision-making for M&A deals.

- Does not need comparable companies: Does not rely on CCA for valuation, which helps with unique companies.

- Helps calculate IRR: Enables the calculation of IRR, a crucial calculation for profitability.

- Sensitivity Analysis: shows how different variables affect valuation, which is critical in checking for risk

On the other hand, the disadvantages are:

- Uses many assumptions: DCF uses a large amount when evaluating growth rates, discount rates, and cash flow, leaving room for error.

- Sensitive to changes: highly sensitive to changes in parameters, leaving it vulnerable to changes surrounding interest rates, economic conditions, and industry trends

- Estimating Terminal value: this valuation can be very subjective, leading to inaccuracies in valuation

- Complexity: Difficult to calculate because of the large amount of factors that go into it, especially difficult for companies with a large amount of

- Ignores other companies: Relies only on the intrinsic value of a company and can overlook industry trends

Conclusion

Overall, Discounted Cash flow is a method financial professionals use to evaluate a potential investment. DCF can be used for evaluating securities, M&A deals, companies, patents, and more. It is used in Private Equity, investment banking, and corporate finance sectors.

DCF is based on money's time value, allowing those using it to calculate the present value of future cash flows. This gives an intrinsic value to the investment in question. If the intrinsic value is less than the current price, it is overvalued; if it's more than the current price, it is undervalued.

Although DCF is widely adopted as the industry standard, it possesses both strengths and weaknesses. DCF's strengths lie in its ability to consider a company's operational and financial performance. DCF can be easily applied to Excel, which speeds up the process of calculating the intrinsic value.

However, DCF still contains flaws within the model. The biggest one is the number of assumptions used to calculate it. Estimates are used when forecasting cash flow and choosing the appropriate discount rate. This can lead to inaccuracies in the valuation.

When making valuations, often, no one method is used by itself. Professionals often use other methods, such as comparable cost and transaction analyses.

Analysts must carefully evaluate the advantages and disadvantages of DCF while considering other valuation methodologies to facilitate informed decision-making.

Discounted Cash Flow FAQs

Discounted Cash Flow is a valuation method that uses the sum of the present value of future cash flows to estimate an investment.

Discounted Cash flow has five steps: first, estimate future cash flows, then calculate the discount rate, next calculate the terminal value, after which sum the discounted cash flows, and finally, if it is a stock being evaluated, calculate the share price.

Financial professionals evaluating investments such as securities, companies, patents, real estate, and more use discounted cash flow.

Some advantages of DCF include the fact that it is very detailed, determines the intrinsic value, can be modeled in Excel, is used for M&A, does not need CCA, helps calculate IRR, and can be used for sensitivity analysis.

Disadvantages to DCF include lots of assumptions, sensitivity to changes, terminal value estimation, complexity, and it ignores other companies.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?