Operating Cash Flow

It is a section of the cash flow statement that measures how much the company generates in cash from its core operating activities.

What is Operating Cash Flow (OCF)?

Operating cash flow (OCF) is a section of the cash flow statement that measures how much the company generates in cash from its core operating activities.

Operating activities are businesses' day-to-day activities that generate revenue and incur expenses directly from selling products and services. They include operating, marketing, production, and administrative tasks.

Some examples are, but are not limited to, sales, cost of goods sold, wages, or taxes. For example, salaries paid to employees involved in production and sales are part of operating cash flow, as they are necessary for generating revenue.

Examining operating cash flow is important because it shows the cash generated from a company's core operations, reflecting its ability to generate cash from its primary business activities.

In contrast, the income statement that includes many non-cash expenses often doesn't show the whole picture.

- The Operating Cash Flow (OCF) represents the cash produced by a company’s primary business activities.

- The first method of calculating OCF is the indirect method, which begins with the net income from the income statement and then adjusts for non-cash transactions and changes to working capital to arrive at the net cash from operations.

- The second method is the direct method, which monitors all cash inflows and outflows during a specific period to determine a figure based on cash transactions.

Importance of Operating Cash Flow

As a part of the cash flow statement, the operating cash flow shows the actual cash impact of the business's core operating activities.

Another important financial statement is the income statement. Although the income statement provides information about a company's operating performance, it includes both cash and non-cash items, unlike the OCF, which focuses solely on cash generated from operations.

Still, it includes several non-cash items that often blur the actual business's cash income.

Here, the OCF comes into play, making several adjustments to the income statement to reflect the cash the company generates from its core operations.

For example, imagine a hypothetical firm generating negative $7,000 in net income on the income statement.

The number might imply that the firm isn't doing well. Still, after looking at its operating cash flow, which excludes many non-cash expenses, it suddenly shows that it earned a positive $3000 in actual cash.

How to Calculate Operating Cash Flow

There are two primary methods to get to the operating cash flow: Direct and Indirect.

The indirect method adjusts the net income for accruals, while the direct method reports cash receipts and payments directly from operating activities.

Let’s look at these methods below:

Indirect Method

The indirect method of calculating OCF involves starting with a net income item and adjusting both the income statement and the working capital items to arrive at the actual cash generated for a given period.

There are many different formulas for calculating OCF indirectly. Even though the approaches are different, they all arrive at the same result.

There is an advanced formula for calculating operating cash flow. The formula is:

Cash generated from operating activities = revenue as reported − increase (decrease) in operating trade receivables − investment income (Profit on asset Sales, disclosed separately in Investment Cash Flow) − other income that is non-cash and/or non-sales related

Or

Cash paid to operating suppliers = costs of sales − stock variation = purchase of goods + all other expenses − increase (decrease) in operating trade payables − non-cash expense items such as depreciation, provisioning, impairments, bad debts, etc. − financing expenses (disclosed separately in Finance Cash Flow)

There is also a more simplistic and generalized formula for the OCF; it is:

Cash flow from operating activities = net income + depreciation, depletion, & amortization + adjustments to net income + changes in accounts receivables + changes in liabilities + changes in inventories + changes in other operating activities

Example

In the indirect method of calculating OCF, non-cash expenses are added back to net income first, followed by adjustments for changes in working capital.

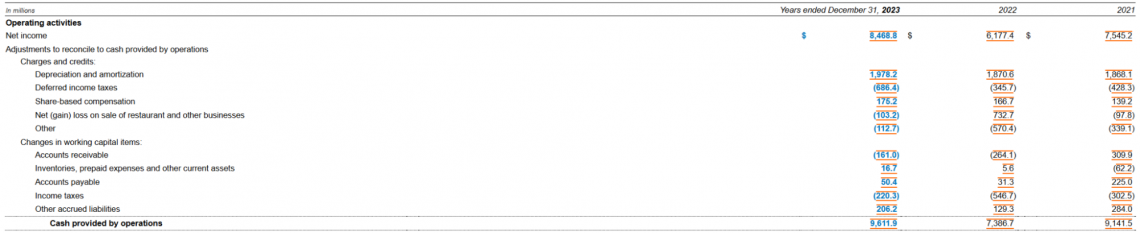

Let’s take a look at the financial statement below:

The OCF starts with a net income of $8.469bn and adjusts for multiple non-cash items. The items include:

- Depreciation and amortization

- Deferred income taxes

- Share-based compensation

- Net (gain) loss on the sale of restaurants and other businesses

- Other non-cash expenses

After adjusting for the non-cash expenses, the statement adjusts for the working capital, including increases and decreases in current assets and liabilities. Adjusting for them helps connect them to associated cash changes.

The items include:

- Accounts receivable

- Inventories

- Prepaid expenses

- Other current assets

- Accounts payable

- Income taxes

- Other accrued liabilities

The example shows how relying only on the income statement can sometimes deceive a person analyzing the financial statements. After the adjustments, the OCF increased to $9,612bn, meaning there were around $1.2bn in non-cash expenses and changes in working capital.

The horizontal analysis shows a substantial $2.3bn increase in operating cash flow from 2022 to 2023, which means more cash gains than losses in that time frame.

Direct Method

In the direct method, the net Cash Flow from Operations (CFO) is computed using the company's accounting records data.

The following format can be used for this purpose:

| Dec 31, 2016 | Dec 31, 2015 | |

|---|---|---|

| Operating cash flow | – | – |

| Cash received from customers and suppliers | 25,900 | 23,478 |

| Cash paid to suppliers | -15,658 | -17,534 |

| Dividend received | 1,200 | 178 |

| Net interest | -5,426 | -4,789 |

| Taxes paid | -1963 | -750 |

| Net cash from operating activities | 4,053 | 583 |

Pros and Cons of Direct and Indirect Methods

Each approach has several pros and cons.

In the direct method, only the cash inflows and outflows during a specific period are shown, and the accruals are not counted.

The direct method is valued for providing clear insights into a company's cash inflows and outflows, which can help understand its past performance and ability to meet current liabilities.

Furthermore, it offers valuable insights for forecasting a company's financial requirements.

In the indirect method, the accruals are adjusted to net income to show the actual changes to cash.

One method's advantage is that it highlights why net income and operating cash flows differ. It uses a predictive approach, starting with future income forecasts and adjusting for balance sheet changes due to timing differences between accrual and cash accounting.

Additionally, adjusting net income to operating cash flows is simpler and cheaper than reporting gross receipts and payments using the direct method.

Operating Cash Flow Vs. Free Cash Flow

Let’s take a look at the table below to understand how both differ from each other:

| Operating Cash Flow | Free Cash Flow | |

|---|---|---|

| Definition | Cash generated from core business operations | Cash available after capital expenditures (CapEx) and operating expenses. |

| Calculation | net income + depreciation, depletion, & amortization + adjustments to net income + changes in accounts receivables + changes in liabilities + changes in inventories + changes in other operating activities | operating cash flow - capital expenditures |

| Purpose | Measures the cash generated by a company’s regular business activities. | Represents the cash available for distribution to shareholders, debt repayment, or reinvestment in the business. |

Operating Cash Flow (OCF) FAQs

One limitation of operating cash flow is that it does not account for capital expenditures (CapEx), which are significant cash outflows related to investing activities.

Also, companies can manipulate the cash flow number by being dishonest about accounts payable, selling (securitizing) accounts receivable, and including cash not related to the company's core operations.

Also, while the calculation of operating cash flow should follow standard accounting principles, variations in reporting practices can occur among different firms.

The analyst can use the Operating Cash Flow Ratio, which measures how well a company can pay off its current liabilities with its cash flow from the core business operations.

The formula to calculate is:

Operating Cash Flow Ratio = Cash Flow From Operations / Current Liabilities

Yes, one measure is Free Cash Flow (FCF). It measures how much cash is left for all the investors after all the operating expenses are subtracted.

One primary advantage of FCF is that it includes the CAPEX, while OCF doesn't.

To calculate, the formula is:

FCF = Cash Flow From Operations - CAPEX

FCF = Net Income + Non-Cash Expenses – Increase in Non-Cash Net Working Capital – Capital Expenditures

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?