Cash Flow Statement

A financial statement that shows cash transactions during a particular period

What Is A Cash Flow Statement?

A cash flow statement (CFS) is a financial statement that shows cash transactions during a particular period.

Financial statements are official documents that measure a company’s financial health by gauging its liquidity, profitability, and overall soundness. There are three main financial statements:

- Balance Sheet

- Income Statement

- Cash flow Statement

A CFS includes an aggregate of all cash-related activities of a company. For example, it shows a company’s cash activities (inflows/outflows) or where the money was moved around.

For a working professional, business owner, entrepreneur, or investor, knowing how to read and understand a CFS enables them to extract essential data to gauge a company’s financial health. This allows them to overall make more sound decisions.

People and groups interested in the statement of cash flow include:

- Accounting personnel

- Current and potential creditors

- Current and potential investors

-

Cash Flow Statement (CFS) is a financial statement that shows cash transactions during a specific period, providing essential data to gauge a company's financial health.

-

CFS categorizes cash activities into Operating, Investing, and Financing activities, enabling users to assess how efficiently a company allocates cash resources.

-

Cash Flow from Operating Activities represents revenue-generating activities and changes in working capital, while Cash Flow from Investing Activities involves long-term asset acquisition and disposal.

-

Cash Flow from Financing Activities shows how a company raises capital from external sources and returns it to investors, affecting the firm's capital structure.

-

CFS has limitations, such as not accurately representing the firm's true liquidity, ignoring non-cash transactions, and not serving as a substitute for an income statement.

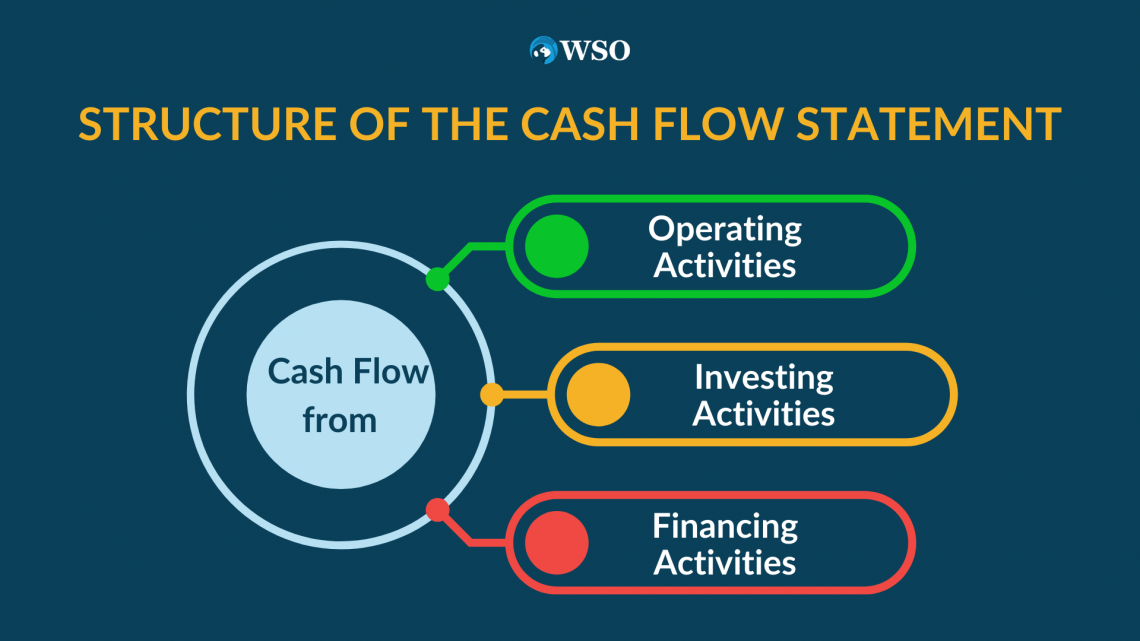

Structure of the Cash Flow Statement

Like every other financial statement, the CFS has a fixed structure.

It is presented in a manner so that the inflows and outflows of cash are classified into three standard activities:

- Operating

- Investing

- Financing

All activities regarding cash movement are categorized under these three distinctions, which help users assess how efficiently a firm has allocated cash resources.

Cash Flow Statements contain the following titles for each of the three cash flow categories:

- Cash Flow from Operating Activities

- Cash Flow from Investing Activities

- Cash Flow from Financing Activities

Note

When a CFS is prepared under the GAAP framework (the accounting standard used in the USA. IFRS standard is used in other parts of the world), another activity is added with the heading: ‘Disclosure of Non-Cash Financing Activities.’

This new heading covers all activities that do not impact cash transactions but are shown in the income statement and balance sheet.

Cash from Operating Activities

Operating activities are the main revenue-generating activities of a company.

These activities include transactions and events that impact the day-to-day activities of an enterprise. It is the sum of net income, non-cash expenses, and the changes in the working capital.

Cash-flow from Operating Activities = Net Income + Non-cash expenses + Changes in Working Capital

The cash flow arising from these activities is called “Cash Flow from Operating Activities”.

Some examples are:

- Cash receipts from

- The sale of goods and rendering of services

- Royalties, fees, commissions, and other revenues

- Debtors and bills receivables

- Cash payments

- Involving purchase of goods and services

- Wages, salaries, and other payments to employees

- Income tax payments or refunds (unless they are related to financing and investing activities)

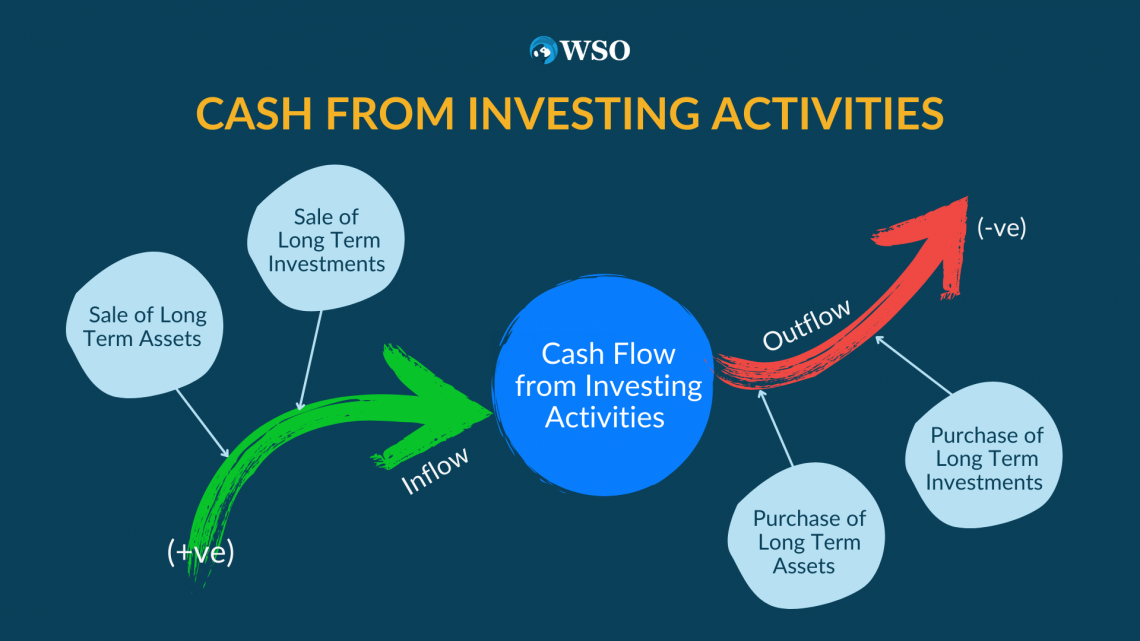

Cash from Investing Activities

Investing activities involve purchasing and selling long-term assets such as lands, buildings, factories, machinery, investments, etc., that are not considered cash equivalents.

Cash flow from investing activities shows the expenses incurred for assets intended to generate cash flows in the future. It also involves receipts from the sale of these assets when they are no longer of any use to the firm.

Some examples include:

- Cash receipts

- From the sale of fixed assets (including intangibles like copyrights, trademarks, etc.)

- From the sale of shares, warrants, or debt instruments of other enterprises (other than receipts of those instruments that are considered to be cash equivalents)

- From the repayment of advances and loans made to third parties

- From insurance claims made for the property involved in an accident

- From interests on debentures and dividends on shares

- Cash payments

- For acquiring fixed assets

- For acquiring shares, warrants, or debt instruments of other enterprises

- For advances and loans made to third parties

Cash from Financing Activities

Financing activities in the CFS show how a firm raises money from capital markets to pay back its investors.

Cash flow from financing activities = net debt + net equity + net capital leases - dividend payments

These activities affect the capital structure of the firm by:

- Adding or revising loans

- Issuing and/or selling more stock

- Paying cash dividends

Activities include:

- Cash Receipts

- To issue shares or other similar instruments

- For short-term or long-term borrowings (such as issuing debentures, bonds, loans, etc.)

- To increase the balance of bank overdraft or cash credit limits.

- Cash Payments

- For the buyback of equity shares

- For the redemption of preference shares

- For the repayments of short-term and long-term borrowings (including paying back debentures, bonds, loans, etc.)

- For interim dividends and the previous year’s proposed dividend

- For interest on short-term and long-term loans, bank overdrafts, and cash credit

- For preliminary expenses such as registration fee, stamp duty, legal fee, etc.

- For any decreases in the balance of bank overdrafts or cash credit limits

Cash and Cash Equivalents

“Cash” consists of cash in hand (accessible cash) and demand deposits (with banks). Demand deposits are deposits of money that can be withdrawn without any notice (e.g., a current account).

On the other hand, cash equivalents are short-term investments that are easily convertible into cash. As a result, they are highly liquid and carry a minuscule risk of change in their value.

Examples of cash equivalents include:

- Currency

- Treasury bills

- Commercial papers

These are purchased with cash left over after immediate needs.

Normally, an investment will be termed as a cash equivalent only if it has a short maturity period, say 90 days or less from its acquisition. Investments in shares are excluded from cash equivalents unless deemed cash equivalents.

Investment in a company’s preferred shares will count as a cash equivalent only if they are redeemable within 90 days from the date of the purchase. As a result, there may always be a risk that the investment cannot be paid back at the time of its maturity.

Thus, cash and cash equivalents combined include:

- Cash in hand

- Cash at the bank

- Short term Investments or Marketable Securities

- Cheques and Drafts on hand

Treatment of Interest and Dividend on Cash Flow Statement

There are different ways to prepare a CFS under IFRS and GAAP principles.

IFRS stands for “International Financial Reporting Standards” and includes a set of rules that make financial reports consistent and comparable across the world.

GAAP stands for “Generally Acceptable Accounting Principle.” It is used in the United States and includes a set of generally followed rules for preparing financial reports.

A) Interest and Cash Flow

Under GAAP, interest paid and interest received are classified as operating activities.

On the other hand, IFRS allows a firm to choose its policy for classifying interests based on what it considers appropriate.

- Interest paid can be recorded under either operating activities or financing activities.

- Interest received can be recorded under either operating activities or investing activities.

B) Dividend and Cash Flow

Like interest, there are different standards for recording dividends between GAAP and IFRS.

Under GAAP, dividends paid are recorded under ‘financing activities’, whereas dividends received are to be recorded under ‘operating activities.’

Subsequently, under IFRS protocols, companies choose how they would prefer to categorize their dividends.

- Dividends paid are recorded under either operating or financing activities.

- Dividends received are recorded under either operating or investing activities.

Disclosure of Non-Cash Activities on cash flow statement

Non-cash activities do not involve cash transactions but are recorded in the income statement.

These activities impact an asset’s value on the balance sheet. Non-cash activities include:

- Depreciation

- Amortization

- Unrealized gain

- Unrealized loss

- Deferred income tax

- Stock-based compensation

Let’s look at an example of depreciation.

Depreciation, in simple terms, can be defined as the loss in value of an asset over its course of life due to usage, wear and tear, etc. It involves the allocation of an asset’s cost over its useful life.

Examples of depreciable assets include buildings, plants, machinery, vehicles, etc. The land is the only exception, as land value appreciates over time.

Depreciation Cost = (Purchase Price - Scrap Value) / Estimated Life

And while depreciation is for fixed assets, amortization, on the other hand, is the loss in value of intangible assets over time. Examples of assets that can be amortized include patents, trademarks, copyrights, etc.

Note

Disclosure of non-cash activities is included when preparing a CFS under GAAP.

Preparing Cash Flow Statement

There are two ways of calculating CFS:

- Direct Method

- Indirect Method

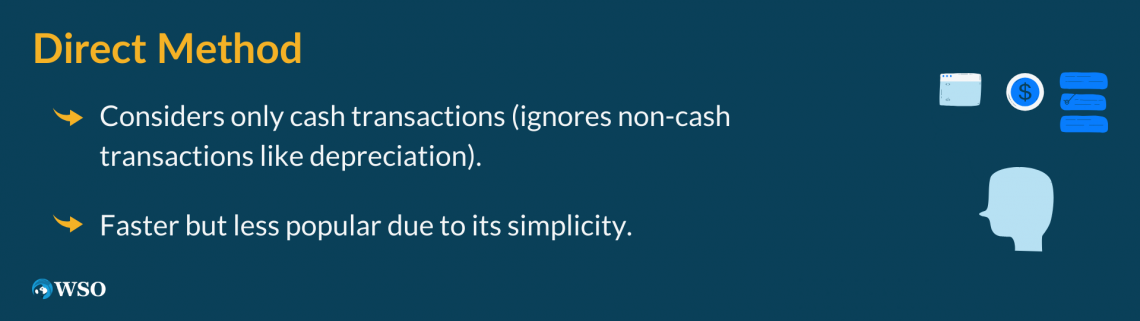

1. Direct Method

Only cash transactions (like cash payments and receipts) are calculated in the cash flow statement in the direct cash flow method. This method ignores all assumptions and does not consider the impact of non-cash transactions (e.g., depreciation).

Preparing a CFS when using the direct cash flow method takes less time as it ignores all assumptions and does not rely on adjustments. However, for this very reason, it is not popular in the accounting industry and is used less by organizations and businesses alike.

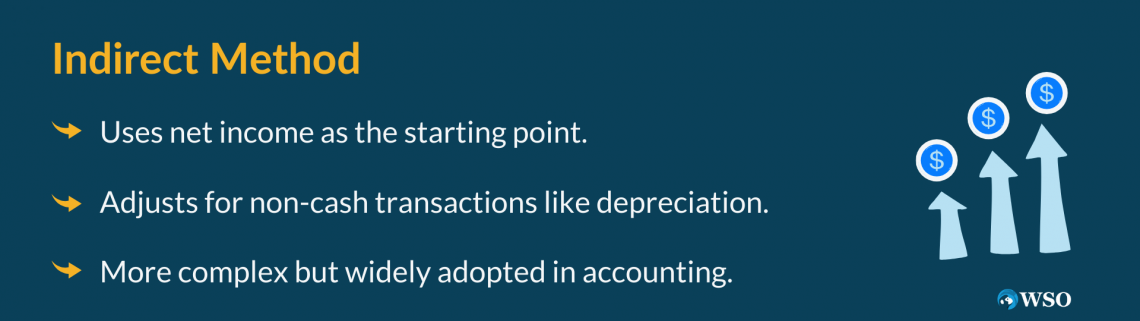

2. Indirect Method

The indirect method of cash flow is complex compared to the direct method as it uses net income as the base, recognizes the necessary adjustments needed, and considers the impact of non-cash transactions.

In this method, depreciation (a non-cash transaction) is generally added back into the net income.

Example for the Cash flow Statement (CFS)

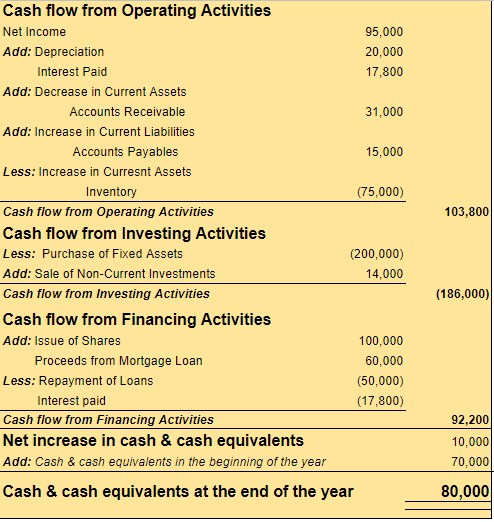

Given below is the CFS of ABC Ltd. company for the year ended on December 2021:

ABC Ltd.

Cash Flow Statement

For the year ended on December 2021

(All figures in USD)

As you can see, the first part of the statement calculates the Cash Flow from Operating Activities.

With net income as the base, we add non-cash transactions (depreciation) + non-operating activity transactions (interest paid) + changes in working capital.

(Cash Flow from Operating Activities = Net Income + Non-Cash Transactions + Non-Operating Activity Transactions + Changes in Working Capital)

The sum of these values gives us Cash flow from Operating Activities. (which equals $103,800 here).

Note that interest paid is not an operational activity. Therefore, we add the non-operating transactions back to the net income to calculate the true cash flow from operating activities.

The second part of the statement calculates the Cash Flow from Investing Activities. We add the cash received from the sale of non-investments and deduct the cash paid to purchase the fixed asset.

(Cash Flow from Investing Activities = Sale of Non-Current Investments - Purchase of Fixed Assets)

The sum gives us Cash flow from Investing Activities which is $(186,000), which means a negative balance showing cash outflow.

The third part calculates the Cash Flow from Financing Activities. The funds received through the issuance of shares and mortgage loans are added, while the cash paid for the redemption of debentures and dividend payments are deducted.

(Cash Flow from Financing Activities = Issues of Shares + Proceeds from Mortage Loan - Repayment of Loans - Interest Paid)

The sum gives us the total Cash flow from Financing Activities, equaling $92,200.

In the end, we add the three calculated cashflows to get the net increase in cash and cash equivalents.

When added to the previous year's cash and cash equivalent balance, this amount should match the current year’s cash and cash equivalent balance.

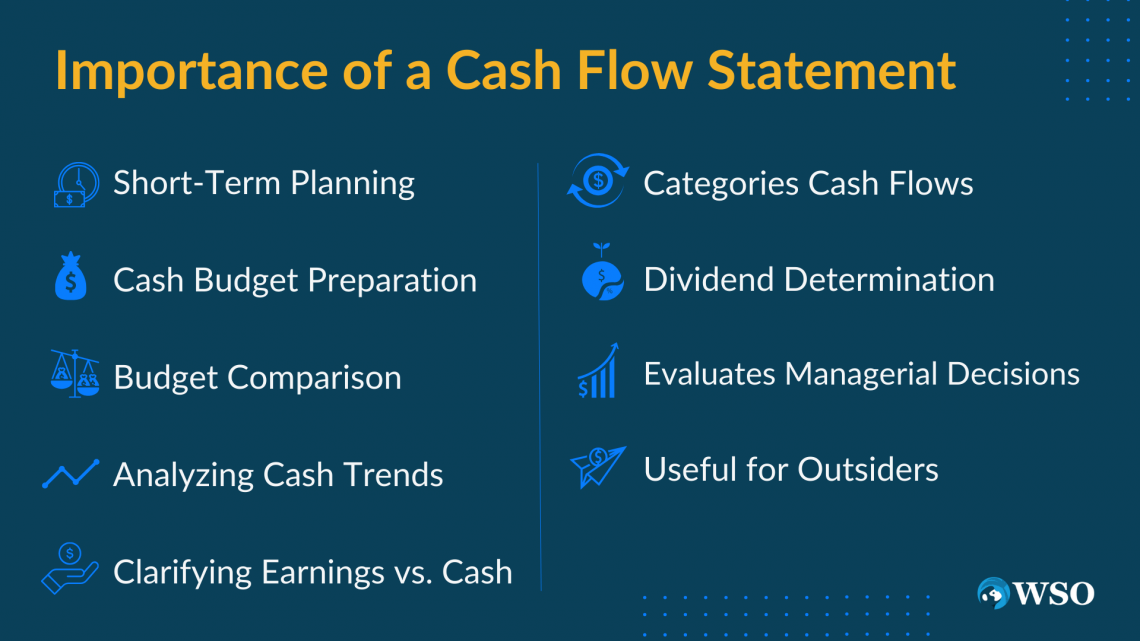

Importance of a Cash Flow Statement

A cash flow statement is essential for the following reasons:

1. Useful for short-term planning

It provides information for planning the short-term financial needs of a firm.

Since it provides information regarding the sources and utilization of cash during a period, it becomes easier for the management to assess if a company has a healthy cash flow.

For example, the management checks if the company has adequate cash to:

- Meet its day-to-day expenses

- Pay the creditors on time

- Pay the long-term loans and interests

- If it has enough cash to pay for the purchases of fixed assets

2. Useful in preparing the cash budget

A cash budget can be prepared with the help of a projected CFS (a statement prepared for the future period). A cash budget helps inform the management of cash surplus or deficit periods.

For example, in the months in which cash receipts exceed payments and months in which cash payments exceed the receipts, the projected CFS helps fill those deficits with the surplus of funds and vice versa.

3. Comparison with the cash budget

A cash budget is prepared at the beginning of the year. In contrast, a CFS is prepared at the end of the financial period (usually one year).

A comparison of the two gives insights into how a firm’s financial resources have been generated and utilized according to the budget. First, the differences between the two can be analyzed. Then, measures can be taken to correct them.

4. Studying trends of cash receipts and payments

A statement of cash flow reveals the speed at which cash is being generated from the trade receivables, inventory, and other current assets and the speed at which current liabilities are being paid.

It enables the management to assess the true position of the cash in the future.

5. Elucidate cash deviations from earnings

A profit-making company can have a lot of cash, or, when it suffers a loss, it may still have plenty of cash. A cash flow statement explains the reasons for it.

6. Classifies cash flow from various activities

The CFS aims to highlight cash flows from operating separately, investing, and financing activities. The amount of cash that has been generated or allocated in such activities is explained by CFS.

7. Aids in determining dividends

The management uses a CFS to determine the cash generated from operating activities that can be used for dividend payments.

8. Tests managerial decisions

Sources of long-term funds should be used to purchase fixed assets. These sources include:

- Issue of shares

- Debentures

- Bonds

- Taking long-term loans

The CFS shows whether the management has used these funds efficiently and whether these funds can be reimbursed using the cash generated from operating activities. Therefore, it is generally preferred to follow this policy.

9. Useful to outsiders

A CFS helps investors, debenture holders, bankers, lenders, suppliers of credit, etc., to analyze the financial position of an enterprise so that they can make more sound decisions.

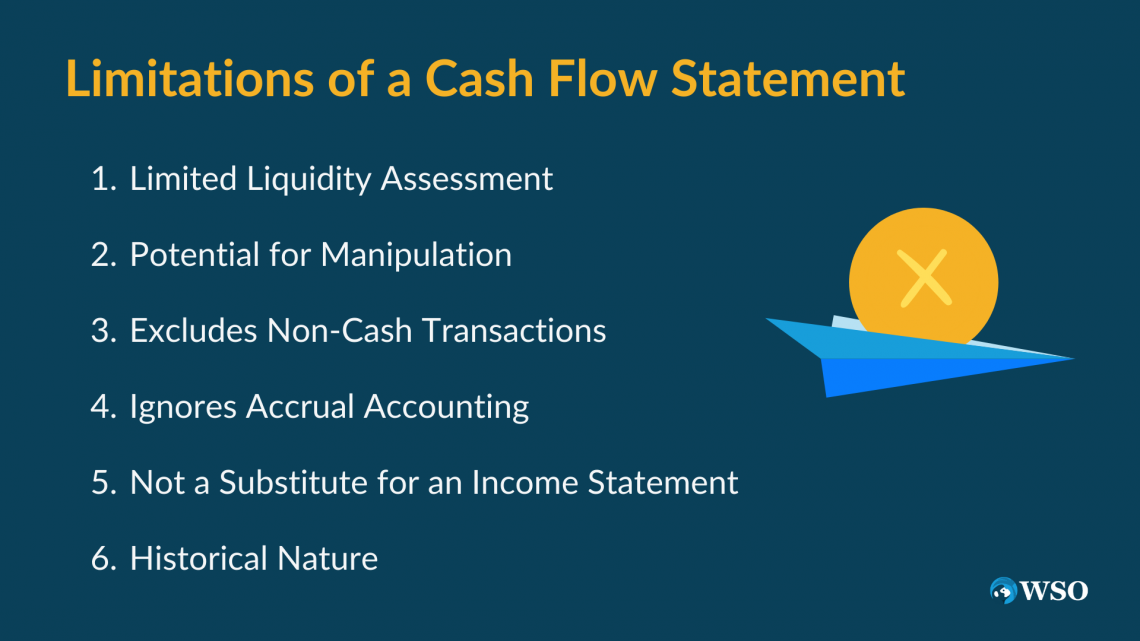

Limitations of a cash flow statement

Recognizing these limitations is crucial for any stakeholder, be it an investor, creditor, or manager, to interpret the data more judiciously and make informed decisions.

1. Not suitable for judging the liquidity

CFS does not represent the true liquidity of a firm as liquidity is comprised of both cash and assets that can be converted into cash easily. Examples include marketable instruments, bonds, etc. Excluding these assets prevent accuracy in reporting a firm’s liabilities.

2. Possibility of window dressing

The possibility of window-dressing (manipulation of the figures in the financial statements to make the firm look attractive to the investors) is higher in the case of a firm’s cash position than a firm's working capital position.

The cash balance can be easily maneuvered by postponing purchases and other payments by rapidly collecting cash from debtors before the balance sheet date.

3. Ignores non-cash transactions

CFS ignores non-cash transactions such as:

- Purchases of fixed assets through the issuance of shares or debentures

- Conversion of debentures into shares

- Issuance of bonus shares.

Thus, the true position of an enterprise cannot be valued solely through a cash flow statement.

4. Ignores the accrual concept of accounting

CFS is prepared on a cash basis, meaning it ignores one of the basic concepts of accounting, namely the accrual concept.

The accrual concept in accounting allows an organization to record the revenue of a good or service when the transaction occurs as opposed to when the good/service is received.

5. Not a Substitute for an income statement

A cash flow statement does not take into account the non-cash items. Therefore, net cash flow does not mean the net income of a business. Instead, the net income of the business includes income from cash and non-cash transactions.

6. Historical in Nature

A statement of cash flow is prepared based on the years passed. Therefore, information revealed by it will be more useful if a projected CFS accompanies it.

Researched and authored by Aqsa Wasif | LinkedIn

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?