Chart of Accounts

A collection of all the accounts that the company maintains to keep track of all the financial transactions

What is the Chart of Accounts?

A chart of Accounts is the collection of all the accounts that the company maintains to keep track of all the financial transactions. It is a complete listing of all the accounts a company uses to classify and record its financial transactions.

It presents a scientific and structured technique for bookkeeping, ensuring that monetary statements are correct, reliable, and comprehensive.

Here are some reasons why they are important:

1. Accurate financial reporting

Organizing and classifying all financial transactions helps businesses ensure accurate financial reporting. This enables accountants and other financial professionals to prepare financial statements and reports easily.

2. Easy tracking of financial transactions

Businesses can easily track and monitor their financial transactions. This simplifies seeing any anomalies or faults and swiftly implements corrective measures.

3. Better decision-making

A well-planned COA can offer insightful information about a company's financial health, assisting management in making decisions regarding investments, costs, and other financial issues.

4. Consistency and standardization

It helps ensure consistency and standardization in financial reporting across the organization. This makes it easier to compare financial data over time and across different departments.

5. Accounting guidelines

Businesses must keep them as it allows you to abide by several accounting regulations, including the Generally Accepted Accounting Principles (GAAP).

Businesses also need to ensure that their financial reporting complies with rules and best practices in the sector by adhering to these standards.

- A Chart of Accounts (COA) is a structured system in accounting that is used to classify and organise financial transactions in order to ensure accurate financial reporting and decision-making.

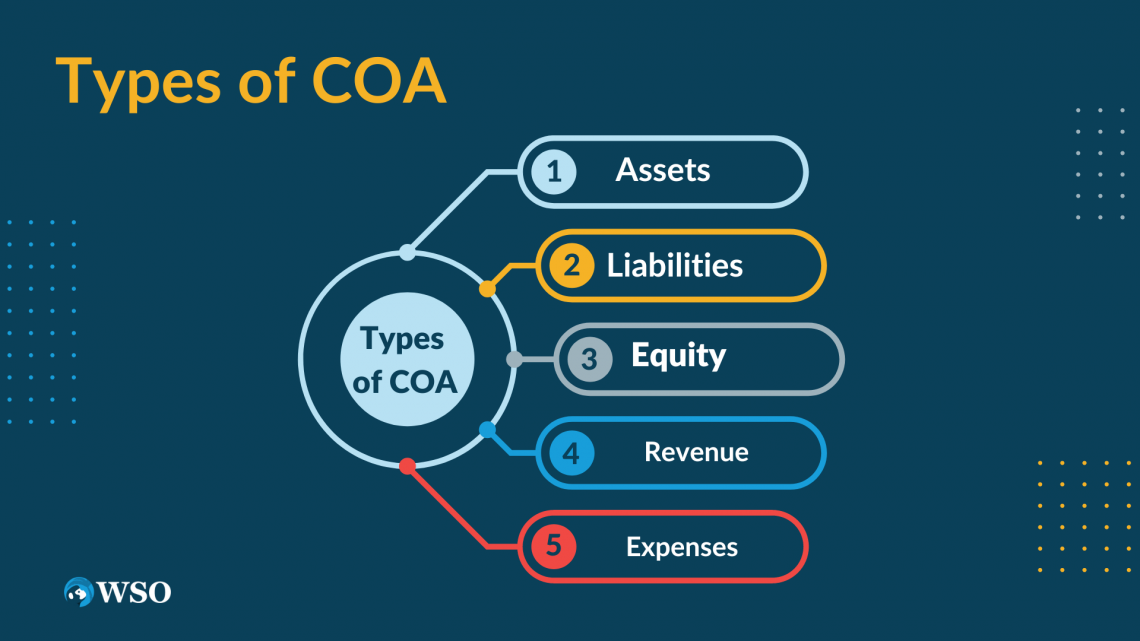

- The COA is normally divided into five major categories: assets, liabilities, equity, revenue, and expenses, with subcategories for more thorough classification.

- Assets are resources that a firm owns or controls, whereas liabilities are commitments to third parties. After removing liabilities, equity represents the company's residual worth.

- Revenue and expense categories aid in the tracking of income sources and daily operating expenditures, enabling for accurate financial statement production and performance review.

Types of Chart Of Accounts

It typically includes a series of categories and subcategories that help organize the company's financial data. These classes can also include assets, liabilities, equity, revenue, and expenses.

1. Assets

Assets are resources a company owns or controls, expected to provide future economic benefits. Those benefits can come in the form of expanded sales, decreased expenses, or multiplied cost of the asset over the years.

Here are some examples of asset accounts that might be included:

- Cash

- Accounts Receivable

- Inventory

- Property, Plant, and Equipment

- Investments

- Prepaid Expense

Each of these asset accounts has a normal debit balance, which means that any growth within the account is recorded as a debit, and a lower is recorded as a credit.

For example, if a commercial enterprise spends $1,000 on new stock, the transaction can be recorded as a credit to the cash account and a debit to the inventory account.

2. Liabilities

Liabilities are obligations that a company owes to external parties, such as suppliers, lenders, or customers. These obligations can arise from transactions such as loans, accounts payable, or taxes owed.

The liabilities category in a COA is usually divided into subcategories, each representing a specific type of liability. The subcategories may include:

- Current Liabilities

- Long-term Liabilities

- Contingent Liabilities

Note

When liability is incurred, it is recorded in the appropriate account within the chart of accounts using the double-entry accounting system.

The liability account is credited, representing the increase in the company's obligation, while the corresponding account is debited, representing the decrease in assets or increase in expenses.

3. Revenue

Revenue is a critical account in the COA for any company that generates income. In the double-entry accounting system, revenue is recorded as a credit entry, indicating that it increases the company's equity.

Note

The revenue account is typically classified as an income statement account and is located within the "revenue" category of the chart of accounts.

This category may also include subcategories:

- sales revenue

- service revenue

- rental revenue

- Depending on the nature of the business' operations, interest revenue.

Since the revenue account is a nominal account, it is closed at the conclusion of each accounting period to ascertain the business's net income or loss.

When a sale is made, the revenue account is credited, and the amount credited represents the revenue made by the business. For instance, the revenue account will receive a $1,000 credit if a corporation sells things worth $1,000.

4. Expenses

They stand for the expenses an organization incurs in carrying out its daily activities, including wages, rent, utilities, and supplies. Expenses must be properly classified and recorded for accurate financial reporting and decision-making.

Depending on the cost's nature, expenses are generally categorized into different categories. These categories may also include:

- Cost of goods sold (COGS)

- Operating Expenses

- Non-Operating Expenses

Note

By properly classifying and recording expenses, businesses can analyze their spending and identify areas where costs can be reduced or eliminated.

The COA for expenses provides a structured approach to accounting for these costs, making tracking and managing them easier. It also helps businesses prepare accurate financial statements for making informed business decisions.

This maintains the balance of the accounting equation (Assets = Liabilities + Equity) and ensures that the financial statements accurately reflect the company's financial position.

5. Equity

Equity is a fundamental category in the chart of accounts within the double-entry accounting system. Equity refers to the residual interest in a company's assets after deducting liabilities. It represents the company's value that belongs to the owners or shareholders.

Equity accounts are important in determining the financial health of an enterprise. They are used to prepare financial statements together with the balance sheet and the statement of changes in equity.

Within the equity category, several subcategories provide more detail on specific transactions. Some common equity accounts include:

- Capital Stock

- Retained Earnings

- Treasury Stock

- Dividends

When recording transactions in the equity category, the double-entry accounting system requires that every transaction affecting equity must have a corresponding debit and credit entry.

For instance, if an employer issues additional shares of stock for $100,000, the capital stock account may be credited with $100,000, and the cash account might be debited with $100,000.

Categories on the Chart of Accounts

They are a key component of financial accounting used to organize and classify financial transactions into different categories. These categories are then used to prepare financial statements such as the balance sheet and income statement.

1. COA covered within the Balance Sheet

A balance sheet is a picture of a company's financial situation at a specific time. It consists of two main sections: assets and liabilities. The COA is used to classify all the transactions related to these sections.

Assets and liabilities are split into current and noncurrent categories, respectively. The COA provides specific account codes used to record transactions related to each category.

For example, code 101 is used to record cash transactions, while code 201 is used to record accounts payable transactions.

2. COA being incorporated in the Income Statement

A financial statement that displays a company's revenues and outlays over time is the income statement. The COA is used to classify all the transactions related to the income statement.

The income statement consists of two main sections: revenues and expenses. The revenues are categorized into different sources of income, such as sales revenue, rental income, or interest income.

The expenses are classified into different categories, such as salaries and wages, rent expenses, or office supplies.

It provides specific account codes used to record transactions related to each category. For example, code 400 is used to record rent expenses, while code 500 is used to record salaries and wages expenses.

Chart Of Accounts Example

It offers a methodical technique to classify and arrange financial data, making it simpler for businesses to produce financial reports and evaluate their financial performance. First, let's look at a real-world illustration to further comprehend the significance of a COA.

Suppose a small retail business called ABC Company has a COA that includes the following categories:

- Assets: This category includes ABC Company's assets, such as cash, inventory, and property.

- Liabilities: This category includes ABC Company's liabilities, such as loans, accounts payable, and taxes owed.

- Equity : This category includes ABC Company's equity accounts, such as common stock and retained earnings.

- Revenue : This category includes all of ABC Company's revenue accounts, such as sales revenue and rental income.

- Expenses : This category includes all of ABC Company's expense accounts, such as rent, utilities, and salaries.

- Using this COA, ABC Company can record all of its financial transactions in a systematic and organized manner.

For example, if ABC Company sells merchandise to a customer, it would record the transaction in the sales revenue account under the revenue category.

Note

When it comes time to generate financial reports, such as a balance sheet or income statement, ABC Company can easily use the chart of accounts to compile the necessary information.

If ABC Company pays rent for its retail space, it will record the transaction in the rent expense account under the expense category.

For example, the balance sheet would include all of ABC Company's assets, liabilities, and equity accounts, which are organized based on the categories in the COA.

The income statement would include all of ABC Company's revenue and expense accounts, also organized based on the categories in the COA.

In conclusion, a COA is essential for businesses to organize and categorize financial information.

Special Considerations

When creating COA, it is important to ensure it is organized, accurate and reflects the organization's specific needs. In addition, it should include all necessary accounts and be easily understandable to users.

Additionally, they should be flexible enough to accommodate future changes and updates as the organization grows and evolves. Businesses must consider several special considerations when creating and maintaining their chart of accounts.

1. Industry-specific accounts

Different industries have unique financial reporting requirements, and businesses must ensure that their COA reflects those requirements. For example, in contrast to service-based businesses, manufacturers may need to monitor inventory levels and the cost of goods sold.

Therefore, businesses should tailor them to their specific industry and financial reporting needs.

2. Tax Compliance

Businesses must ensure they comply with tax laws and regulations. This means that businesses must categorize and record transactions in a way that accurately reflects their tax obligations.

For instance, companies need to keep track of tax-deductible expenses, such as personal spending and business travel costs.

3. Accounting software compatibility

Most businesses use accounting software to manage financial transactions and generate financial reports. Therefore, businesses must ensure their COA is compatible with their accounting software.

Note

All employees should use the same account names, numbers, and categories when recording financial transactions. This consistency ensures that financial reports are accurate and reliable.

This means the account names, numbers, and categories must be consistent with the accounting software's requirements.

4. Scalability

As businesses grow and evolve, their financial reporting needs may change. Therefore, businesses must ensure that their COA can accommodate future growth and changes.

This means the COA should be adaptable enough to add new accounts and modify current accounts as necessary.

5. Consistency

Finally, businesses must ensure that their chart of accounts is consistent across all departments and locations.

Conclusion

COA is a critical component of any business's financial management system. It provides a framework for accurate financial reporting, easy tracking of financial transactions, improved decision-making, consistency and standardization, and compliance with accounting standards.

The charts of accounts provide a systematic and organized way to classify financial transactions and prepare financial statements such as the balance sheet and income statement.

It is a systematic way of organizing financial information and provides a framework for financial reporting and analysis.

It is an essential tool for any business or organization to control its budget efficiently. It permits them to hold track of their financial transactions, discover trends and patterns, and make knowledgeable decisions based on the statistics.

A well-designed chart of accounts must be comprehensive, correct, and smooth to use. In addition, it has to offer a clear picture of the monetary fitness of the organization and permit management to make knowledgeable choices primarily based on the data.

By implementing a chart of accounts, businesses can speed up their accounting processes and reduce the likelihood of errors and inaccuracies.

Businesses must carefully consider several factors when creating and maintaining their accounts chart.

Keeping these special considerations in mind, businesses can ensure that their accounts chart is accurate, compliant, and scalable, which is critical for generating reliable financial reports and making informed business decisions.

By using a chart of accounts, companies can easily generate financial reports and analyze their financial performance, which is critical for making informed business decisions.

or Want to Sign up with your social account?