Balance Sheet

The balance sheet is a financial statement that documents a company’s assets, liabilities, and shareholder’s equity at a particular point in time.

What Is the Balance Sheet?

The balance sheet is a financial snapshot of a company’s finances at a specific point in time.

It is one of the three main financial statements, along with the income statement, which details financial performance over a period of time, and the cash flow statement, which details sources and uses of cash over a period of time.

It lists what a company owns (its assets), what the company owes (its liabilities), and the capital invested by shareholders (shareholder’s equity). It can be found along with the other two main financial statements in most financial disclosures and in any 10-K or 10-Q.

- The balance sheet is a financial statement that documents a company’s assets, liabilities, and shareholder’s equity at a particular point in time.

- It is one of the three main financial statements and can be found alongside them in any 10-K or 10-Q.

- Its main components are current and non-current assets, current and non-current liabilities, and shareholder’s equity.

- All components must balance according to the fundamental accounting equation: Assets = Liabilities + Shareholder’s Equity.

- It is connected to the income statement via retained earnings and the cash flow statement through the ending cash balance.

Understanding The Balance Sheet

Whereas the income statement tracks a company’s revenues and expenses over a period of time and a cash flow statement records the company’s cash flows over that same period, a balance sheet details the company’s financial position at the end of the period by listing its assets, liabilities, and shareholder equity.

Because of this, to evaluate the company’s financial performance, any balance sheet must be compared to the previous year’s to determine how the company’s assets, liabilities, and shareholder’s equity have changed during the period.

It must always adhere to the fundamental accounting equation, which is as follows:

Assets = Liabilities + Equity

This equation simply describes how all of a company’s assets must be financed either by borrowing money (i.e., accumulating liabilities) or through investments by shareholders (i.e., equity).

Note

The balance sheet is easy to read and understand precisely because it is broken down into these three basic accounting elements. Shareholder’s equity must always be equal to the difference between assets and liabilities.

For example, if a company takes out a $10 million loan that matures in 15 years, $10 million is added to the cash account in the assets section, and $10 million is added to the long-term debt account in the liabilities section. Since both sides of the equation increase by $10 million, the equation still holds.

Additionally, if a company receives $5 million in profits, $5 million is added to the cash balance, and $5 million is added to retained earnings, which is included under shareholder’s equity. The balance sheet still balances since $5 million is added to both sides of the equation.

Investors can use the information on it to calculate various ratios that can be used to assess the company’s financial position, its stability, and the risk involved in that enterprise.

For example, investors can use the debt-to-equity (D/E) ratio to determine a company’s capital structure. In this case, the company’s D/E ratio should be compared to that of its peers to get a sense of whether it is taking on too much or too little debt.

How the Balance Sheet is Structured

The balance sheet is divided into three parts: assets, liabilities, and shareholders’ equity, which are the three components of the fundamental equation of accounting.

Liabilities and shareholder’s equity are often grouped together and sometimes placed on the right side of assets to reflect the fundamental accounting equation.

Assets are divided into current and non-current assets depending on how quickly they can be converted into cash. Similarly, liabilities are divided into current and non-current liabilities depending on how quickly they must be paid back.

Current assets

Current assets are those that can be converted into cash within one year. Because of their speed of conversion, these assets are called liquid and are the first to be sold in case the company needs to pay off debt.

The assets portion lists items in order of descending liquidity. The following is a list of items in the current assets section.

- Cash and cash equivalents are the single most liquid item on the entire statement since it is already cash (or equivalents). Besides hard cash, this account includes short-term certificates of deposit and treasury bills.

- Marketable securities encompass all debt and equity securities that can be readily sold on the market. These include stocks, bonds, and even preferred shares and ETF shares.

- Inventory consists of products for sale to the public.

- Accounts receivable (AR) denotes money that customers owe the company. For example, if a customer buys a product now but defers payment to a later date, the value of the purchase would go into accounts receivable. Some companies adjust the accounts receivable amount to account for customers who are unlikely to pay the company back.

- Prepaid expenses refer to goods and services the company has paid for in advance but has yet to receive or use.

Non-current assets

Non-current assets are those that cannot be converted to cash within a year because it takes longer than a year to get the full value out of these assets.

Non-current assets are capitalized as opposed to expensed, and they lose value over reporting periods through depreciation, amortization, and impairment even though the company does not lose or receive any money from a cash point of view.

The following is a list of items in the non-current assets portion:

- Property, plant, and equipment (PP&E) refers to land, buildings, machinery, equipment, and other such assets.

- Intangible assets denote assets that may not be physical but are still important to the company. The main examples of intangible assets are intellectual property (copyright) and goodwill.

- Long-term investments include all financial investments that cannot be converted into cash within the current financial year.

Current liabilities

Just like assets, liabilities are divided into current and non-current liabilities. Current liabilities are those that must be paid within the next twelve months. Current liabilities are listed in order of when they must be paid.

The following is a list of items that commonly appear on the current liabilities portion.

- Accounts payable (AP) is money the company owes for a service that has already been provided (e.g., the company has still not paid last year’s electricity bill).

- Short-term debt and the current portion of long-term debt include loans with a maturity of less than a year and loans with a maturity longer than that, which expire this year.

- Wages payable are wages that the company still hasn’t paid its employees.

- Dividends payable denote dividends whose payment has been authorized but hasn’t been made.

- Interest payable is interest on debt that hasn’t yet been paid.

Non-current liabilities

Non-current liabilities are financial obligations due in more than twelve months. These are usually large amounts of money borrowed to finance the company’s operations.

The following are the three main items in the non-current liabilities section.

- Long-term debt denotes all debt that reaches maturity in more than one year.

- Deferred tax liability refers to taxes that have been incurred but whose payment has been delayed to the next year.

- Various obligations that don’t fit into other categories are grouped under "other long-term liabilities."

Shareholder’s Equity

Shareholder’s equity represents the residual interest in the company’s assets after liabilities have been deducted. It is the final portion of the balance sheet and is sometimes also placed to the right of assets under liabilities.

The following are the components of the shareholder’s equity section.

- Retained earnings are equal to net income (as found on the income statement) less any dividends paid to the company’s shareholders. This money can be used for several purposes, such as paying out further dividends, reinvesting in the company, paying back debt, etc.

- Treasury stock denotes the shares that a company has bought back from the public. By doing this, the company is able to consolidate ownership and prevent a hostile takeover, as well as boost stock prices and increase financial metrics.

- If a company issues preferred stock, this will also be found on the shareholder’s equity portion of the statement. Preferred stock is senior to common stock in its claim to the business’s assets, meaning that holders of preferred stock will be paid before owners of common stock in case of the company’s liquidation.

How To Prepare A Balance Sheet

There are a few fundamental steps to preparing a balance sheet, but the most important thing to keep in mind is that its main objective is to detail all of a company’s assets and liabilities at a specific point in time.

The following is a summary of the main steps:

- Determine the reporting date: To prepare a balance sheet, you first need to know when you want to report your company’s financial position.

- Record assets: After determining the date for the statement, you need to identify and record all of the assets your company held on that date.

- Record liabilities: Similarly, you must also find and list out all of your company’s liabilities as of that same day.

- Determine shareholder’s equity: After listing out all assets and liabilities, you must record how much of the company is attributable to its shareholders. This calculation and the specific line items under the shareholder’s equity section will depend on how many different kinds of stock and other warrants or options the company offers.

- Apply the fundamental accounting equation: After recording assets, liabilities, and shareholder’s equity, any accountant must add liabilities and shareholder’s equity together and confirm that this equals assets. If not, the fundamental equation of accounting does not hold, and there have been mistakes or omissions.

- Format: The purpose of a balance sheet is to showcase the company’s financial position to investors and creditors. Therefore, it is important to neatly format it to easily read and interpret it

How To Read A Balance Sheet

The balance sheet provides insight into liquidity, solvency, and the allocation and utilization of long-term and short-term resources.

Being able to interpret it is crucial to investors, as it is fundamental in determining the amount of risk involved in a company.

By comparing a company’s balance sheet to those of peers, investors can determine whether it is over-leveraged and might default on its loans and declare bankruptcy.

Investors can also use the items on the balance sheet to calculate several ratios that quantify a company's financial health. These include leverage ratios, which provide insight into how much debt a company has taken on:

Debt-to-equity (D/E) ratio = total debt/shareholder’s equity

Debt-to-assets (D/A) ratio = total debt / total assets

Debt-to-capital (D/C, or capitalization) ratio = total debt / (total debt + shareholder’s equity)

Asset-to-equity ratio = total assets/shareholder’s equity

As well as liquidity ratios, which determine how capable a company is of meeting its short-term debt obligations:

Current ratio = current assets / current liabilities

Quick ratio = (cash + accounts receivable + marketable securities) / current liabilities

Cash ratio = (cash + marketable securities) / current liabilities

Note

It is important to understand that a balance sheet does not say anything about the performance throughout the fiscal period but only gives the investor a snapshot of the company’s position at a specific point in time.

Whatever the company’s position at the end of the fiscal year, the balance sheet does not provide any information about whether this is an improvement over last year or a deterioration. Therefore, any balance sheet is best interpreted compared to previous years.

Similarly, ratios such as the D/E ratio or the current ratio are most useful when compared to those of other companies. Since different sectors require more debt financing than others, choosing a peer group of comparable companies is fundamental.

It is also vital to remember the fundamental equation of accounting. The balance sheet should always balance, as per the fundamental accounting equation: assets equal liabilities plus shareholder’s equity. If this is not the case, there may be errors in the data reported or miscalculations.

Balance Sheet And Other Financial Statements

While the three main financial statements all examine the company’s performance from different perspectives, they all refer to the same company. Therefore, there is some crossover between the statements, and they all flow into one another.

The balance sheet is connected to the income statement via retained earnings, which appears under shareholder’s equity and is equal to net income (from the income statement), less any dividends paid to the company’s shareholders.

The cash flow statement is linked to the balance sheet primarily through the cash and cash equivalents item and changes in working capital.

This item represents cash at the end of the period and is equal to the last period’s ending cash balance plus all the cash flows detailed in the cash flow statement.

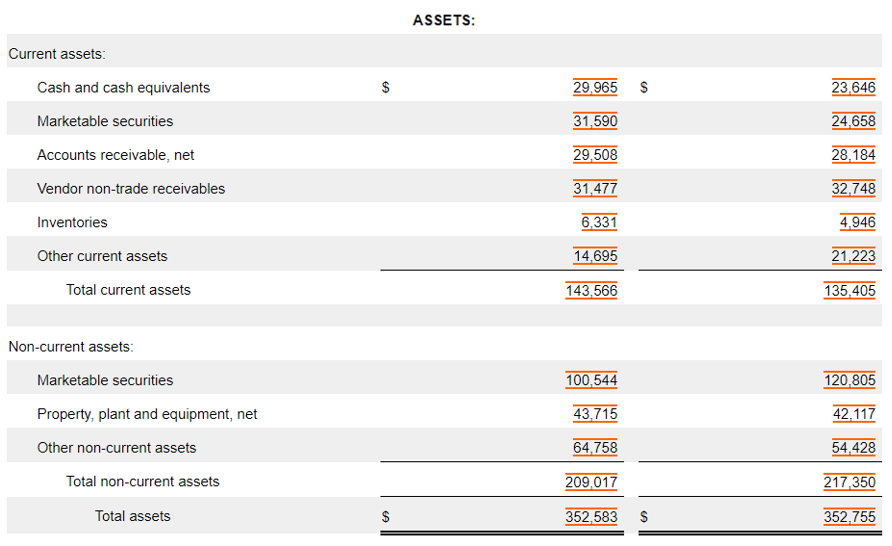

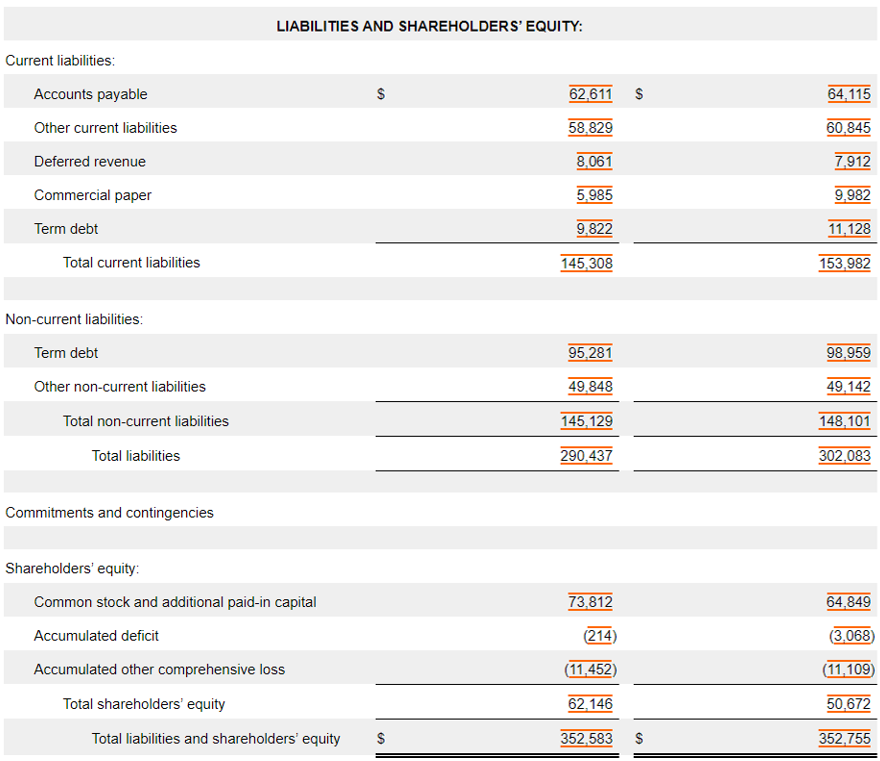

Balance Sheet Example

Below is a balance sheet taken from Apple’s 10-K for the fiscal year ending September 30th, 2023, which has been adapted for the purposes of this article.

The company’s current and non-current liabilities are listed, followed by its current and non-current assets, along with shareholder’s equity.

According to the fundamental accounting equation, total assets are equal to total liabilities plus shareholder’s equity.

Income Statement vs. Balance Sheet

The income statement, also called the profit and loss (P&L) statement, is another one of the three main financial statements. The income statement tracks a company’s revenues and expenses and other gains and losses during a given period.

While the balance sheet provides a snapshot of a company’s position at a given point in time, the income statement details how a company’s finances have changed throughout the period. Therefore, both statements should always be analyzed in conjunction.

For example, the balance sheet discloses how much debt a company has taken on. Only the income statement can tell if the company is growing enough to justify that amount of leverage.

Similarly, the balance sheet can outline a company’s assets, but only the income statement can show whether the company effectively employs those assets to make a profit.

| Statement | Income Statement | Balance Sheet |

|---|---|---|

| Timeframe | Tracks change over a period of time. | Records position at a specific point in time. |

| Content | Outlines profits and losses. | Outlines assets, liabilities, and shareholder equity. |

| Use | To gauge the performance, profitability, and growth of a company. | To determine whether a company has enough assets to cover its financial obligations. |

| Items | Revenue - Cost of Goods Sold (COGS) = Gross Income - Selling, General, and Administrative Expenses (SG&A) = Operating Income (EBIT) + Non-Operating Income - Non-Operating Expenses - Interest Expense = Earnings Before Tax (EBT) - Tax Expense = Net Income |

Assets:

Liabilities:

Shareholder’s Equity |

| Fundamental Formula | Net Income = Revenue + Non-Operating Income - COGS - SG&A - Interest Expense - Tax Expense | Assets = Liabilities + Shareholder’s Equity |

Balance Sheet FAQs

The balance sheet is a financial statement that records a company’s assets, liabilities, and shareholder’s equity at a specific time. It is one of the three main financial statements, including the income and cash flow statements.

There are three main components: current and non-current assets (what the company owns), current and non-current liability (what the company owes), and shareholder’s equity (what is attributable to the company’s shareholders).

The total value of assets must equal the sum of the total values of liabilities and shareholder's equity, as per the fundamental accounting equation.

The balance sheet is connected to the income statement via retained earnings, which appears under shareholder’s equity and is equal to net income (from the income statement), less any dividends paid to the company’s shareholders.

It is linked to the cash flow statement through the cash and cash equivalents item. This item, which represents cash at the end of the period, is equal to the last period’s cash balance plus all the cash flows detailed in the cash flow statement.

Interpreting the balance sheet is crucial to investors, as it is fundamental to determining the amount of risk involved in a company.

By reading the liabilities section, investors can determine how much debt the company has taken on and compare it to peers. They can also determine whether the company is over-leveraged and whether it might default on its loans and declare bankruptcy.

It is also a detailed list of everything the company owns and owes and might give investors a good reason to invest in a company (or to divest from it) if it is apparent that the balance between the company’s assets and liabilities will (or will not) lead to its growth.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?