Credit Rating

An evaluation that assesses the creditworthiness of an individual or a firm.

What Is A Credit Rating?

Credit rating is an assessment of a potential or existing debtholder's credit risk, evaluating the ability to pay the debt and/or interest due on debt.

Your credit score frequently affects the terms and circumstances you are granted, whether applying for a loan, a credit card, or renting an apartment. You may build a solid financial future by making wise financial decisions and being aware of your credit and its ramifications.

So what are credit ratings, and why are they so important for an individual and any organization? Ratings are significant in the financial sector since they help assess the creditworthiness of an individual or a firm.

It presents valuable statistics to lenders, permitting them to assess the risk of extending credit or loans. A person's capability to fulfill commitments and repay debts is summarized through their credit score, which is a snapshot of their financial situation.

Ratings are typically assigned by specialized rating agencies that conduct thorough evaluations based on a range of factors.

These factors include payment history, outstanding debts, credit utilization, length of credit history, and recent credit inquiries. By analyzing these elements, the rating agencies assign a rating that reflects the borrower's overall financial stability and risk profile.

The rating of the credits scale consists of various grades, often represented by letter-based or alphanumeric symbols. The scale typically ranges from AAA (or equivalent) for the highest creditworthiness to D (or equivalent) for the lowest.

Ratings over a specific level are considered investment grade, suggesting a lesser risk of default, whereas ratings below that level are considered speculative or non-investment grade.

A rating has significant implications for borrowers. Those with higher ratings have better chances of obtaining credit or loans at favorable interest rates and terms. It opens doors to financial opportunities and demonstrates responsible financial management.

Conversely, poorer ratings may lead to restricted credit availability or loans with higher interest rates, making it harder to achieve financial objectives.

- A credit rating evaluates the creditworthiness of a borrower, indicating the likelihood that they will be able to repay their debt obligations. It is assigned by credit rating agencies.

- Credit ratings help investors and lenders assess the risk of lending money or investing in a particular entity, such as a corporation or government, influencing interest rates and investment decisions.

- Credit ratings are typically expressed as letter grades (e.g., AAA, AA, A, BBB, etc.), where higher grades indicate lower risk and better creditworthiness. Ratings can be either investment grade or speculative (junk).

- Agencies consider various factors in assigning credit ratings, including the entity’s financial health, debt levels, economic environment, management quality, and historical repayment behavior.

Understanding Credit rating

Credit rating is pivotal in the financial ecosystem as a crucial indicator of a character's or an organization's financial health and creditworthiness.

Understanding why the score is crucial is essential for people, corporations, and lenders alike because it considerably affects access to credit, interest rates, and typical monetary opportunities.

First and foremost, a good credit score opens doors to many financial benefits. It enhances the ability to secure loans, mortgages, and credit cards, often at more favorable interest rates and terms.

NOTE

Higher credit ratings for borrowers signal lower risk to lenders, inspiring confidence and resulting in lower borrowing costs. Credit ratings extend beyond personal finance, encompassing corporations and organizations as well.

Good credit enhances a company's reputation, instills trust, and attracts investors. It facilitates access to financing for expansion, R&D, and strategic initiatives, making it easier to pursue business goals.

For individuals, keeping an excellent credit score is essential for long-term financial stability. It enables access to affordable credit during emergencies, such as medical expenses or unexpected repairs.

Additionally, a positive rating can lead to lower insurance premiums, better rental opportunities, and even improved job prospects, as employers increasingly consider credit history during hiring.

Importance of Credit Rating

Let's focus on a vital topic: the importance of Credit Rating (CR). Refer to the list below to grasp the significance of this key financial indicator.

1. Access to Credit

A high credit score increases the likelihood of loan approvals, credit card applications, and mortgages. Lenders see borrowers with good credit as less risky, making it easier to access credit resources.

2. Interest Rates

Good ratings can lead to lower interest rates on loans and credit cards. Higher credit ratings make borrowers appear less risky of defaulting, allowing them to bargain for better conditions and accumulate large sums of money over time.

3. Financial Opportunities

Strong ratings open doors to various financial opportunities, such as favorable business loans, investment options, and partnerships. A positive credit history helps businesses attract investors and secure funding for expansion and innovation.

NOTE

For individuals, good credit can lead to better rental options, lower insurance premiums, and increased job prospects.

4. Utility Services

Utility companies often consider credit scores when determining deposit requirements for services such as electricity, water, and phone connections. A good credit score may reduce or eliminate the need for large deposits, making it easier to set up essential services.

5. Insurance Premiums

Insurance providers often factor credit scores into their pricing models. A better credit score can result in cheaper insurance rates since people with strong credit are more responsible and less prone to submit claims.

This will result in vast financial savings on various insurance policies and automobile, home, and life insurance.

6. Housing Opportunities

Landlords and property management companies frequently assess ratings when considering rental applications.

NOTE

A strong credit score increases the likelihood of being approved for desirable rental properties and may even allow negotiation of lower rental rates.

7. Employment Considerations

Some employers, particularly those in finance, security, or positions involving financial responsibility, may review credit reports as part of their hiring process. Good credit reflects financial responsibility and may enhance employment prospects in these industries.

8. Peace of Mind

Maintaining good credit provides peace of mind. It ensures financial stability and the ability to navigate unexpected situations effectively.

With a strong credit history, individuals and businesses have a safety net for emergencies. They can confidently pursue their financial goals without the added burden of limited credit options or high-interest rates.

How Credit Rating Works

Understanding how the rating works is essential for borrowers seeking credit, negotiating favorable terms, and making informed financial decisions. In the US, credit scores for people generally vary from 300 to 850, with higher scores denoting more creditworthiness.

They consider various factors, including payment history, debt levels, credit utilization, length of credit history, types of credit utilized, and recent credit inquiries. These factors collectively shape the rating assigned to an individual or entity.

On the other hand, credit scores for companies often use a different scale. The rating companies like Standard & Poor's, moody's, and Fitch offer one frequently used scale.

Generally, they use alphanumeric symbols for rating purposes, including AAA, AA, A, BBB, BB, B, CCC, CC, C, and eventually D.

NOTE

The ratings are often displayed on a scale, with AAA being the highest and C being the lowest. Ratings over BBB are considered investment grade, suggesting a reduced risk, whereas ratings below BBB are considered speculative.

Understanding the workings of credit score agencies, the factors they consider, and the rating scale allows borrowers to actively manage their credit profiles, improve creditworthiness, and access favorable credit terms.

By navigating the credit landscape effectively, individuals and businesses can unlock opportunities and build a solid financial foundation.

Now we will go through the three main elements of how rating works. The following are the three elements for a better understanding:

- CR agencies

- Factors considered in CR

- CR scale

Credit Rating Agencies

As independent establishments that evaluate the creditworthiness of people, companies, and governments, credit score groups play a vital function within the financial landscape.

These agencies evaluate the risk of lending money to borrowers and provide objective credit ratings that help lenders, investors, and financial institutions make informed decisions.

These agencies employ rigorous methodologies and analytical models to evaluate various factors contributing to creditworthiness.

They assemble data from various sources, including financial statements, public documents, and different pertinent records, to provide an intensive evaluation of an entity's financial health.

Credit score corporations use each quantitative and qualitative fact to inform their ratings. They look at quantitative elements like industry forecasts, regulatory environment, and financial conditions, as well as qualitative ones like payment records, debt levels, and financial ratios.

The groups use their expertise, experience, and proprietary models to assign credit rankings, replicating the perceived degree of danger to a borrower.

These companies have established credibility and are widely recognized within the financial industry. However, it's critical to know that distinctive regional and specialized credit score agencies exist.

NOTE

The rating agencies offer an essential service by offering impartial and independent creditworthiness assessments.

Investors, lenders, and borrowers may verify threats and make intelligent lending decisions, make an investment, and manage credit, thanks to the information furnished by their evaluations.

The scores these groups assign significantly affect borrowing charges, investment opportunities, and the general functioning of financial markets.

Factors Considered in Credit Rating

CR agencies consider various factors to determine ratings. While the exact methodologies may vary between agencies, common factors include the following.

1. Payment history

The track record of timely payments is crucial in evaluating creditworthiness. Consistently making timely payments improves credit, while late or missed payments can have adverse effects.

2. Debt levels

The amount of outstanding debt is taken into account. High debt levels relative to income or credit limits may negatively impact ratings.

3. Credit utilization

The percentage of available credit being utilized is an important factor. Keeping credit utilization low, ideally below 30%, demonstrates responsible credit management.

4. Length of credit history

The length of time an individual or entity has been using credit is considered.

NOTE

A longer credit history provides more data points for assessment and can contribute positively to credit scores.

5. Types of credit utilized

A diverse credit mix, including credit cards, loans, and mortgages, demonstrates responsible credit management. Using a variety of credit types responsibly can improve the ratings.

6. Recent credit inquiries

The number of recent credit applications or inquiries can impact credit. Multiple inquiries within a short period may raise concerns about financial stability.

Credit Rating Scale

Individuals and businesses have distinct rating scales. Credit evaluates borrowers' creditworthiness and predicts the possibility of debt default.

While ratings serve the same goal for people and businesses, the scales and methodology utilized to establish these ratings may differ.

The difference in scales between individual and corporate credit ratings is due mainly to the various criteria and risk assessments involved in determining people's vs. organizations' creditworthiness.

| Credit Rating | Individuals (United States) | Companies |

|---|---|---|

| Excellent | 800-850 | AAA |

| Very Good | 740 - 799 | AA |

| Good | 670 - 739 | A |

| Fair | 580 - 669 | BBB |

| Poor | 300 - 579 | BB and below |

Benefits of a Good Credit Rating

Numerous advantages that come with maintaining high credit can have a favorable effect on several facets of personal and financial life. Good credit makes chances possible, promotes financial flexibility, and offers assurance.

When people and companies know the advantages of having excellent credit, they are better equipped to manage their credit profiles and make wise financial decisions actively.

NOTE

A good credit score enhances access to credit resources, enabling individuals and businesses to secure loans, credit cards, and mortgages more easily. It also paves the way for favorable interest rates and terms, saving borrowers significant money over time.

Moreover, a positive rating opens up a world of financial opportunities, from favorable business loans and investment options to partnerships and collaborations.

Beyond financial opportunities, a good rating may lead to lower insurance premiums, better rental options, and increased job prospects.

Insurance providers often factor credit scores into their pricing models, while landlords and property management companies consider ratings when assessing rental applications.

Some employers also review credit reports for positions involving financial responsibility, making a good rating an asset in the job market.

Ultimately, maintaining good credit provides peace of mind and financial stability. It serves as a safety net during unexpected situations and ensures the ability to navigate emergencies and pursue financial goals confidently.

By recognizing the benefits of good credit, individuals and businesses can proactively manage their creditworthiness and unlock a world of financial possibilities.

Advantages of a Good Credit Score

Some of the most common advantages are:

1. Lower borrowing costs

Your good credit can provide mortgages and credit at cheaper interest rates. Lenders who have certain ratings see borrowers as less hazardous, allowing them to negotiate better conditions and pay less in borrowing fees.

Whether it be a mortgage, vehicle loan, or private loan, this results in significant financial savings throughout the loan.

2. Easier loan approvals

A good credit score simplifies the loan approval process. Lenders are more inclined to approve applications from individuals with strong credit because they demonstrate a history of responsible financial behavior.

NOTE

With a good rating, borrowers can avoid the frustration and potential rejection of loan applications, making accessing the funds needed for various purposes easier.

3. Better insurance rates

Insurance providers often consider credit scores when determining insurance premiums. Low insurance premiums result from people with high credit being seen as more responsible and less prone to make claims.

NOTE

Maintaining an excellent credit score can also result in widespread financial savings on insurance rates, whether for home coverage, car insurance, or different types of insurance.

4. Higher credit limits

A good rating can lead to higher credit limits on credit cards and lines of credit. Financial institutions are more willing to extend larger lines of credit to borrowers with a proven track record of responsible credit management.

Increased credit limits give people and companies more purchasing power and financial flexibility.

5. Enhanced financial opportunities

Good credit opens doors to a wide range of financial opportunities. It improves the chances of securing favorable business loans, attracting investors, and forming strategic partnerships.

Furthermore, those with high credit are more likely to get approved for premium rewards credit cards, giving them access to incentives like cashback, travel rewards, and special advantages.

6. Increased ability to negotiate

Borrowers have more negotiation leverage if they have a strong credit score. They can use their creditworthiness as leverage to acquire better conditions, such as a reduced loan interest rate, a bigger credit limit, or advantageous terms for a mortgage.

NOTE

A strong rating gives individuals and businesses a competitive edge in financial transactions.

7. Improved housing opportunities

A good rating can open doors to better housing opportunities. Landlords often consider credit scores when evaluating rental applications, and a strong credit history increases the chances of being approved for desirable rental properties.

Moreover, it allows for negotiating lower rental rates or reduced security deposits.

8. Peace of mind and financial stability

Peace of mind with high credit is one of the most significant advantages. With a strong credit history, individuals and businesses have a safety net during financial emergencies.

They can confidently navigate unexpected situations, knowing they have access to credit options at favorable terms. A good rating provides financial stability and the freedom to pursue long-term goals and aspirations.

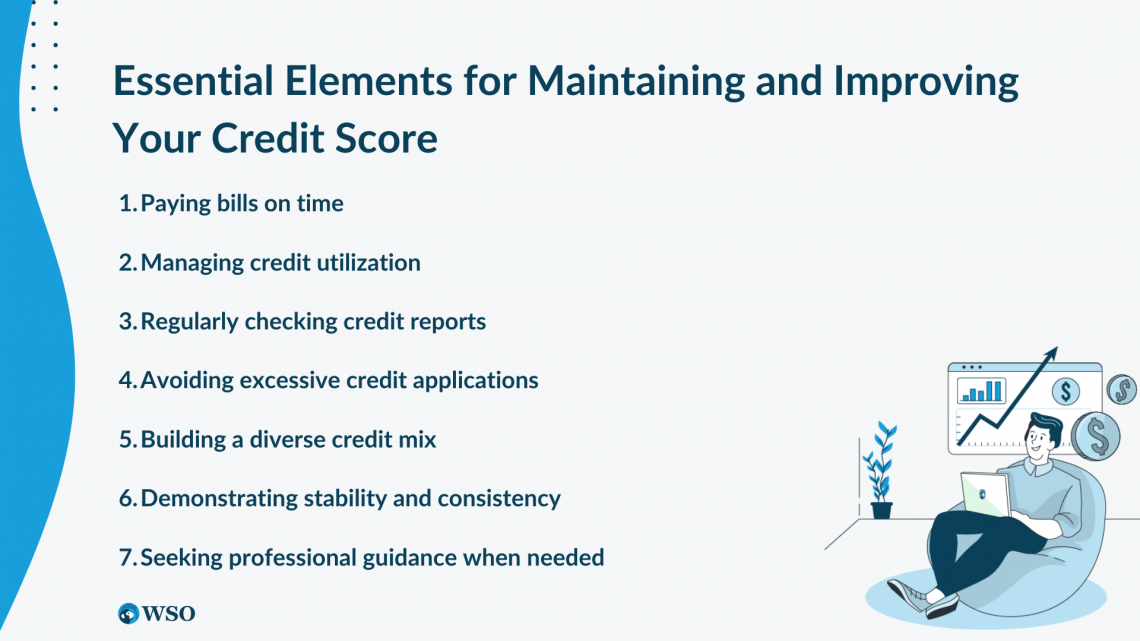

Maintaining and Improving Your Credit Rating

Your financial stability depends on maintaining and raising your credit. Positive borrowing conditions, cheaper interest rates, and a wide range of financial prospects are all made possible by having a high rating.

People must use appropriate credit management techniques to build and maintain solid credit. This includes keeping track of credit use, paying on time, monitoring credit reports often, and refraining from making too many credit applications.

Individuals may establish a strong credit history, boost their creditworthiness, and profit from a favorable credit rating by being aware of these crucial tactics and continuously putting them into practice. Controlling your credit is a proactive step in achieving financial freedom and security.

Essential Elements for Maintaining and Improving Your Credit Score

1. Paying bills on time

Paying bills on time is crucial for maintaining a good rating. Timely payments demonstrate financial responsibility and reliability to lenders and credit rating agencies. Set up automatic payments or create reminders to ensure bills are paid promptly.

Consistently meeting payment deadlines helps build a positive payment history, which is a significant factor in determining creditworthiness.

2. Managing credit utilization

The percentage of your available credit that you are now utilizing is called credit usage. Keeping credit utilization low is key to maintaining a good credit rating. Aim to utilize at most 30% of your available credit across all accounts.

High credit utilization may signal financial strain and negatively impact your credit score.

NOTE

Regularly review your credit card balances and strive to pay down debts to maintain a healthy credit utilization ratio.

3. Regularly checking credit reports

Monitoring your credit reports is essential for spotting errors, detecting fraudulent activity, and staying informed about your credit standing. Equifax, Experian, and TransUnion annually offer free copies of your credit reports, which you should examine for accuracy.

NOTE

If you identify any inaccuracies or discrepancies, promptly dispute them to ensure your credit score is based on correct information.

4. Avoiding excessive credit applications

Frequent credit applications can raise concerns for lenders and negatively impact your credit rating. Each credit application results in a hard inquiry on your credit report, which temporarily dings your score.

Minimize unnecessary credit applications and only apply for credit when needed. Be selective and research lenders' requirements and credit offers to increase your chances of approval without generating excessive inquiries.

5. Building a diverse credit mix

Having a diverse mix of credit accounts demonstrates your ability to responsibly manage different types of credit. This includes credit cards, installment loans, and mortgages. Building a balanced credit portfolio over time can improve your ratings of credit.

NOTE

Avoid taking on unnecessary debt or opening multiple accounts simultaneously, as this can backfire and lower your credit score.

6. Demonstrating stability and consistency

Lenders value stability and consistency in credit management. Avoid closing old credit accounts unless necessary, as it can shorten your credit history and impact your credit utilization. Keep your accounts open and active, even if you no longer use them frequently.

Regularly using and responsibly paying off credit cards and loans showcase your ability to handle credit responsibly.

7. Seeking professional guidance when needed

Consider seeking professional guidance if you encounter challenges in maintaining or improving your credit ratings. Credit counseling agencies can provide personalized advice, help you create a manageable repayment plan, and offer strategies to enhance your creditworthiness.

Their expertise can empower you to take control of your finances and work towards a stronger credit score.

Common Misconceptions about Credit rating

Common misconceptions about credit rating can lead to confusion and misinformation when managing personal finances. Understanding these misconceptions is crucial for making informed decisions and improving your rating.

Three prevalent misconceptions include the belief that closing credit accounts helps improve rating, that income affects credit score, and that checking your credit rating harms it.

By debunking these misconceptions, individuals can better understand how credit works and take appropriate actions to maintain and improve their creditworthiness.

1. Closing credit accounts helps improve credit

Contrary to popular belief, closing credit accounts does not necessarily improve your credit rating. It can have the opposite effect. Closing accounts can reduce your available credit and potentially increase your credit utilization ratio, negatively impacting your credit score.

NOTE

Keeping credit accounts open is generally advisable, especially if they have a positive payment history, as this contributes to a longer credit history and demonstrates responsible credit management.

2. Income affects the credit score

Income is not a direct factor in determining your credit rating. Credit score agencies focus on your credit history, payment behavior, and other financial factors when assessing creditworthiness.

A larger salary may bring more financial stability but does not guarantee a better credit rating. However, lenders may evaluate your income when determining your ability to repay loans, and evidence of income may be required throughout the application process.

3. Checking your rating harms it

Checking your credit rating, also known as a soft inquiry, does not harm your ratings. Soft inquiries, such as those initiated by individuals for personal credit checks or employers for background checks, do not impact your credit score.

NOTE

It is important to regularly check your credit reports to monitor your credit health, identify errors, and detect any signs of fraudulent activity. These self-checks are considered responsible credit management and have no adverse effect on your credit.

4. Paying off a debt removes it from your credit report

The idea that paying off a debt would instantaneously erase it from your credit record is a prevalent misunderstanding. Your credit report will contain information about the debt and your payment history for a certain amount of time, generally up to seven years.

However, having a history of paid-off debts can still positively impact your credit rating by demonstrating responsible repayment behavior.

5. Carrying a balance on your credit card improves your credit

Some people mistakenly believe that carrying a balance on their credit card and making minimum payments can help improve their rating.

However, this is not true. Carrying a balance from month to month can result in accruing interest and potentially increasing your credit utilization ratio, which can negatively impact your credit score.

NOTE

Pay off your credit card balances in full each month to maintain a healthy credit utilization ratio and show responsible credit management is generally recommended.

6. Closing a credit card improves your credit score

Another misconception is that closing a credit card will automatically improve your credit score. While closing unused or inactive credit cards may appear reasonable, doing so can limit your available credit and shorten your credit history, which can negatively influence your credit rating.

Instead of closing credit cards, keep them open with minimal usage to maintain a longer credit history and a lower credit utilization ratio.

Credit Rating FAQs

Good credit typically falls within the range of 670 to 850, depending on the credit score agency.

The time required to improve a credit rating varies based on individual circumstances. Generally, consistent positive financial habits can lead to improvements over several months to a few years.

No, credit ratings are not inherited. Their unique financial and credit history defines the credit rating of each individual.

While credit agencies strive for accuracy, errors can occur. It's crucial to monitor your credit reports frequently and notify the appropriate organizations of errors.

In addition to credit rating, lenders examine income, job history, and debt-to-income ratio when determining creditworthiness.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?