Cost Structure

The different types of costs incurred by a business to produce, market, and deliver its products or services

What is Cost Structure?

A cost structure is essentially a breakdown of all expenses a company incurs to create and deliver its products or services to customers. These costs usually include fixed and variable costs.

Now, this cost structure isn't the same for every company. It can vary a lot depending on what a company produces, who its customers are, and what it aims for. But broadly, there are two main types:

- Value-driven structure: Quality is the primary consideration. Generally, these are luxury goods with high price tags.

- Cost-driven structure: Price is the primary consideration. These companies prioritize low price tags over the quality of the goods and services they provide.

Within these structures, companies deal with three main types of costs:

- Fixed cost: These costs stay the same no matter how much a company produces. Instead, there is one price to pay, regardless of the number of goods and services produced.

- Variable cost: These costs change depending on how much a company produces. The more goods and services produced, the larger the total variable cost.

- Mixed cost: This is the most complicated of the three, as it combines both types of expenditure. This entails a price with both a fixed aspect and a variable part.

Usually, companies categorize these costs to understand them better and see how profitable a particular project will be. They group similar expenses into something called a "cost pool." For instance, all the money spent on marketing goes into the marketing cost pool.

Once they've figured all this out, they can set prices for their products or services to achieve the desired profit margin.

Another added benefit of a company reviewing its cost structure is that it can reveal the points of inefficiency. By finding these inefficiencies, they can make changes allowing them to maximize profits.

Moreover, having a detailed cost structure is very helpful when analyzing investment opportunities and forecasting profits. For example, when performing the "discounted cash flow analysis" to decide on an investment, a solid cost structure is essential. It's one of the most common ways to decide if a business opportunity is a smart move or not.

- There are two main types of cost structure: value-driven (focused on quality) and cost-driven (focused on low prices).

- Cost structure includes fixed costs (that stay the same), variable costs (that change with output), and mixed costs (that have both fixed and variable elements).

- Value-driven structures allow for higher profit margins but smaller customer bases, while cost-driven structures target larger audiences with lower prices.

- Analyzing cost structure helps set pricing, maximize profits by finding inefficiencies, and forecast earnings for valuation models.

- The three main cost types are: fixed (flat rate), variable (depends on output), and mixed (has both fixed and variable components).

Types of cost structure

As previously mentioned, there are two structures: value-driven and cost-driven. Value-driven refers to companies that seek to provide high-quality goods. On the other hand, cost-driven refers to the cost structure that aims for the lowest production.

Each cost structure has its pros and cons, as well as target audiences. However, you will see that these two structures are the extremes. Due to each polarization, it's essential to keep in mind there is not a one-size-fits-all cost structure.

There are millions of companies around the world, and the goods and services of each fit each differently. This is why a company analyzing its cost structure is critical.

The efficacy of each cost structure varies from business to business. Many companies are in the middle of these two, offering mid-range quality and prices.

Each organization, however, generally leans towards one more than the other. As a result, a company will either focus slightly on delivering quality or providing low prices.

Value-driven structure

This structure focuses on high-quality goods. Usually, this results in high costs for producers due to expensive inputs, skilled workers, and long production times.

One might assume that pushing for quality instead of cost leads to low margins, but the truth is the opposite. Of the two structures, value-driven allows for more significant markups.

Certain companies aiming for high-quality products command astronomical price tags compared to other products in their categories.

Some of these luxury brands bear prices higher than what would be justifiable due to their recognition. Product scarcity is also common among value-driven structures.

Examples of companies with value-driven cost structures are Rolex and Gucci.

While producing a Rolex is more expensive than a Casio, Rolex's profit margin is significantly more significant due to their perceived scarcity and brand recognition.

A Casio watch could sell for $25, whereas a Rolex watch could sell for $10,000. But, of course, that doesn't necessarily mean that a Rolex is 400 times better.

As you can tell, quality isn't the only driver in the price for the goods and services of value-driven companies. The con of these quality products is that the customer base is reduced to higher-income individuals and those willing to spend more.

Cost-driven structure

A cost-driven structure aims to create goods and services that fulfill their purpose for the lowest price possible.

The production cost savings are then passed onto the consumer, making the products cheaper than their competitors. In addition, the low price point allows for a much larger customer base, targeting anyone who wants to save money.

The con of this structure is that the goods and services produced tend to be of lesser quality, possibly lasting less time.

It also can lead to a negative brand perception if consumers become frustrated with the poor performance of goods or services. There are two other common ways a company can decrease production costs other than sacrificing quality.

- Economies of scale: These are savings from producing more significant amounts of a given product or service.

- Economies of scope: When a large array of different products or services are produced, costs can decrease due to the crossover of materials, machines, etc.

No Name is an example of a company using a cost-driven structure. As a result, they produce lesser-quality groceries and household products at a price point significantly lower than competitors.

Types of costs

We'll look deeper at each cost type, reviewing the basics of calculating each. As mentioned previously, calculating costs permits financial analysts to perform valuations.

A better comprehension of each charge will be developed by looking at the most common costs for each category.

With over 210 million companies globally, one can only imagine how much their cost structures vary. From small "mom-and-pop" shops to multinational conglomerates, each has costs that permit the production of their goods and services, which are the building blocks.

Keep in mind that these are only the most basic kinds of costs. A litany of other cost types has been created throughout history with varying levels of recognition, like sunk costs and opportunity costs.

Both of these costs are more for theoretical than practical use. In this article, however, we will only review the three most common costs present in modern-day business: fixed, variable, and mixed costs. So first, we'll look at the simplest, the fixed price.

Fixed cost

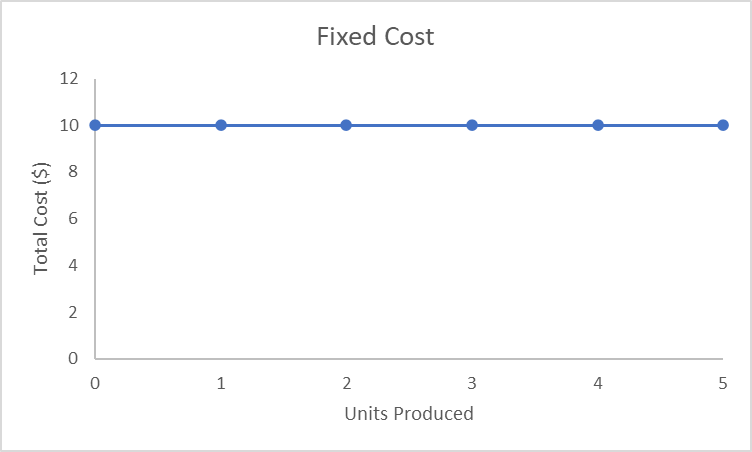

The fixed cost is the simplest of the three costs that will be covered. The essential characteristic of a fixed price is the flat rate that is charged.

So, when you have a fixed cost, it means the amount of money you pay for something doesn't go up or down based on how many things you produce or services you provide.

According to the chart above, imagine you're running a business, and you've got a fixed cost of $10. It doesn't matter if you make one item or a million; you're still paying $10.

Now, let's talk about some common examples. Take office rent, for instance. You have a fixed monthly rent for your office space. It doesn't matter how much business you do in that office, whether it's just a little or a whole lot, the rent stays the same. This unchanging cost, no matter what you're producing, is what makes it a fixed cost.

Variable cost

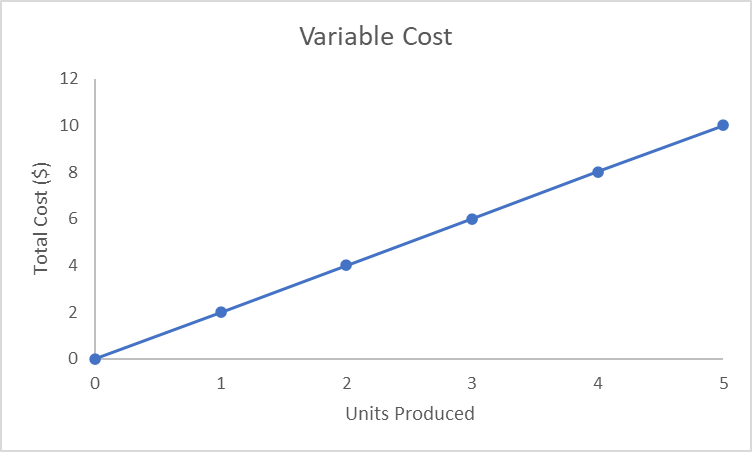

A variable cost is a little more complicated. As the name implies, the amount paid for input with a variable cost relies entirely on how many units of a good or service is produced.

The equation to calculate the price of a variable cost for a given output is the following:

variable cost = price per unit * units outputted.

Looking at the chart above, we see costs increasing by $2 for every new unit produced.

Breaking down this equation, one of the easiest ways to tell that a cost is variable is that when the output reaches zero, the price from that input also does.

The most common variable cost is employee hours. For example, if an organization operates for 100 hours, it must pay employees for 100 hours of work.

If an organization does not operate for a period, no wages must be paid, assuming the salary is hourly rather than annually.

Nearly all other variable costs are business-specific. For example, LCD screens would be a variable cost for a laptop manufacturer, increasing the total variable cost by the screen price for every new laptop.

Mixed cost

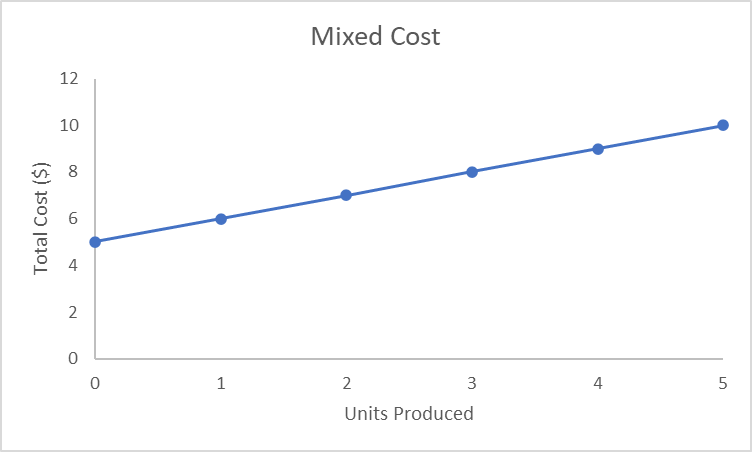

A mixed cost or semi-fixed cost is the most complicated of the three. It is a combination of both variable and fixed costs.

You can imagine a mixed cost as a simple linear equation with an intercept and a slope.

The intercept, i.e., the fixed part of the mixed cost, shows us the minimum flat rate. The slope, i.e., the variable region of the composite price, shows how much each new unit will add to the total cost.

The formula for a mixed cost is the following:

Mixed cost = Flat rate + cost per unit * units produced.

The example above shows that the flat rate is $5, increasing by $1 for every new unit produced. A typical example of a fixed cost is electricity. Generally, a company will pay a baseline amount for electricity in their facility. As we produce more, electricity use will likely also rise. This means that total electricity costs increase when each new unit is made.

Researched and authored by James Fazeli-Sinaki | LinkedIn

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?