|

Digesting the Fed — Like me, when I see my GPA at the end of the semester, monetary policy is getting tight. JPow was clearly hyped in his Wednesday speech, likely as a result of getting to say “jack ‘em up” for the first time since 2018.

And generally, when a Fed Chair says that, equities throw up and yield curves steepen. You may have noticed the literal opposite happen on Wednesday, so let’s dive a little deeper into what might be going on.

First the bond market, because after all, we still only trust dogs and the bond market. Yield curves flattened following the Fed’s announcement, coming way too close to an inversion of the US 5 and 10-year notes.

This was essentially fixed income traders’ way of responding, “bullsh*t,” to JPow’s confidence in the Fed’s ability to orchestrate a so-called “soft-landing,” a.k.a. a tightening cycle that reduces inflation without hindering the labor market.

Basically, the bond market either thinks the Fed’s plan will either 1) not be as effective in stopping inflation as JPow and the gang think, or 2) it will work so well that rate hikes and other measures will eat into labor conditions. Not exactly a winning kind of view.

Equities, on the other hand, might just be stupid. The only possible explanation for the rise across indexes is either that or equity traders had priced in at least a 25bps hike going into Wednesday’s meeting and had anticipated the degree of aggression in planned monetary policy through 2023.

This seems unlikely, as judging by market expectations as of Tuesday, equity investors were mentally prepared for a 25bps hike at this meeting, a max of 7 other hikes throughout this year, and 1 or 2 hikes in 2023. While that was certainly close, the dot plot and Fed commentary now signal 3 or 4 rate hikes, which would generally scare traders more than a dog looking at a vacuum.

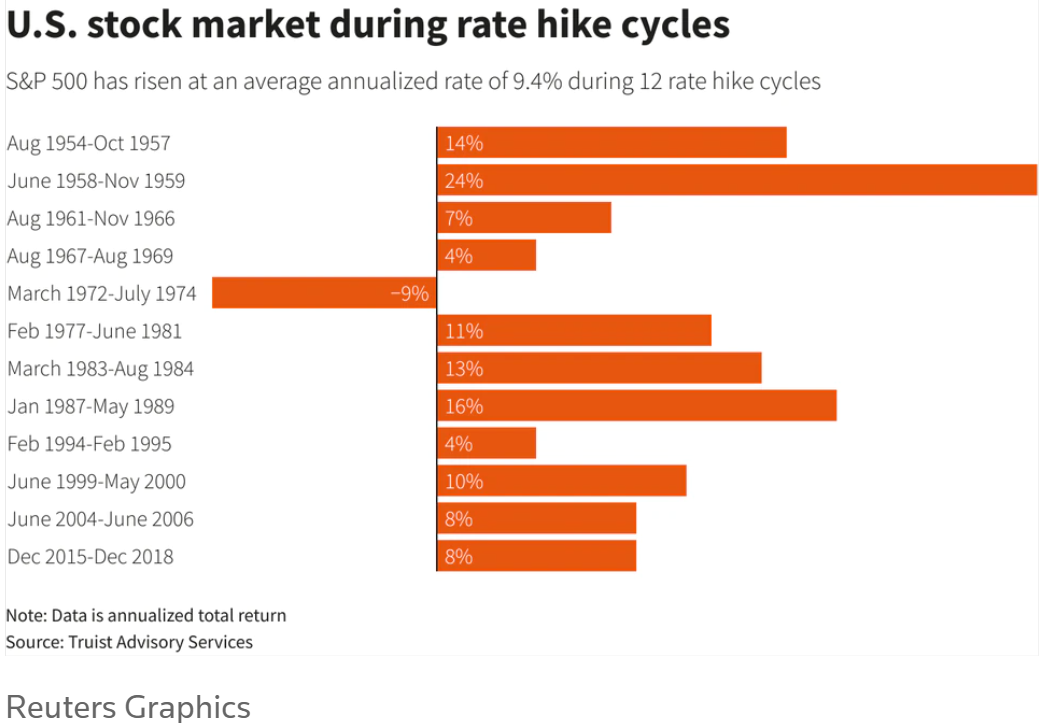

But regardless of what happens in the incredibly short term, history tells us that returns following a hike or during a hike cycle aren’t too shabby. According to a Deutsche Bank study reviewed by Reuters, equities average a return of 7.7% in the 12-months following the start of a rate hike cycle. Reuters also looked at a study by Truist, showing that the average annualized return throughout the course of a hiking cycle is 9.4%.

Keep in mind hiking cycles tend to come into play when the economy is doing well and profits are being pushed higher. Inflation might have something to say about that. But for now, let’s just keep our fingers crossed.

|

Sed et et architecto ab. Non eum vitae error qui et molestiae soluta. Assumenda quia voluptas reiciendis inventore velit laboriosam.

Ea fugiat ab non et ut. Ut quia ut quos sint sit officiis quo.

In ipsam rerum neque quidem. Ea quos omnis molestiae qui expedita ipsa.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...