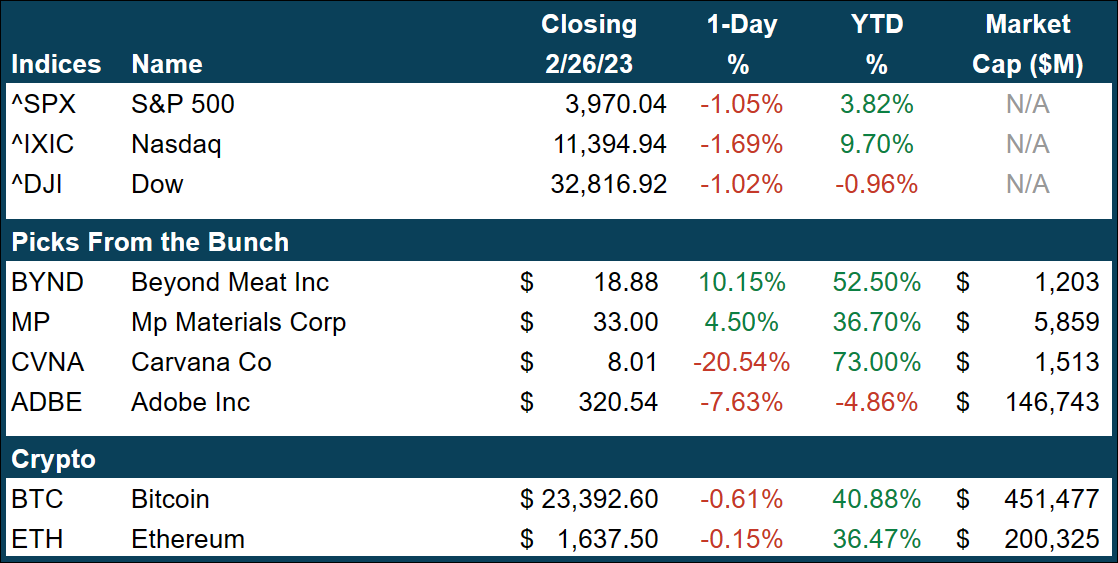

|

Core Day

Everyone loves a solid core day, and the Federal Reserve is no different. Except, instead of trying to finally get those 6-pack abs, the Fed tries to get that 2% inflation target. Same thing, right?

And just like your regular consumption of 6-pack beers prevents your success, the fiscal and monetary $ printing prevents JPow’s success. Nevertheless, we fight both on.

But, instead of looking in the mirror to check his progress, JPow checks government reports and other “official” data for these measures. And finishing out last week, we got the latest and (according to the Fed) the greatest report on consumer prices in the form of the January Core Personal Consumption Expenditure (PCE) price index.

The PCE basically measures the same basket of goods as the CPI, but with food and energy excluded, as well as various other alterations to the weightings of the other line items.

Like golf, we’re looking for a low score here, and unfortunately, that is not at all what January gave us. PCE clocked in at 4.7% for the month of January, beating expectations of 4.3% for the year and registering the highest monthly gain since August at 0.6%. Needless to say, Mr. Market had a meltdown only slightly less egregious than Kanye West on that whack-a** Alex Jones guy’s show.

Mr. Market reacted in such a way for the exact reason you’re expecting me to tell you right now. Inflation came in hotter than expected, particularly on a monthly basis, with the acceleration of PCE growth reaching levels not seen since the days of peak inflation last summer.

There was a brief moment there for a few months where we thought this whole thing might actually be transitory. Friday ripped those hopes apart like Charlie Munger ripped Disney apart this past weekend.

This acceleration in PCE comes on the back of a hotter-than-expected CPI report, and a way-too-jacked jobs report coming out of January as well. One of those would be bad enough, but all three of those things clocking in successively pretty much explain why the S&P has wiped out almost all of 2023’s gains.

Aside from Mr. Market’s schizophrenic hysteria, futures markets trading rate-linked assets pushed the implied probability of a 50 bps rate hike at FOMC’s next meeting to 36%, more than double that of the previous week at just under 18%. Further, the 2-year treasury yield, which basically serves as the bond market’s fed funds rate, jumped over 4.8% for a quick sec and still sits at the highest levels since 2007.

The narrative among some experts and “experts” out there is mostly just speculation, but there’s nothing we love more here than that, so let’s run with it.

Basically, some believe the broad-based inflation the economy has ridden since late 2021 is playing out over two primary cycles. The first was goods inflation, which of course, peaked last summer with things like gas and lumber hitting all-time highs. Now, some argue that we are experiencing that second cycle, being services inflation, as costs associated with the services side of the economy are newly in the driver’s seat.

On the other hand, maybe we just haven’t tightened enough, and prices are setting up to give us the liveliest dead-cat bounce of all time. Fingers crossed for the former, and just remember we’re looking for golf-score inflation: the lower, the better.

|