|

Macrohard

Personally, I think ^that’s a way better name for the U.S.’s second-largest company, but looking at Bill Gates, it’d probably be a stretch even on a good day.

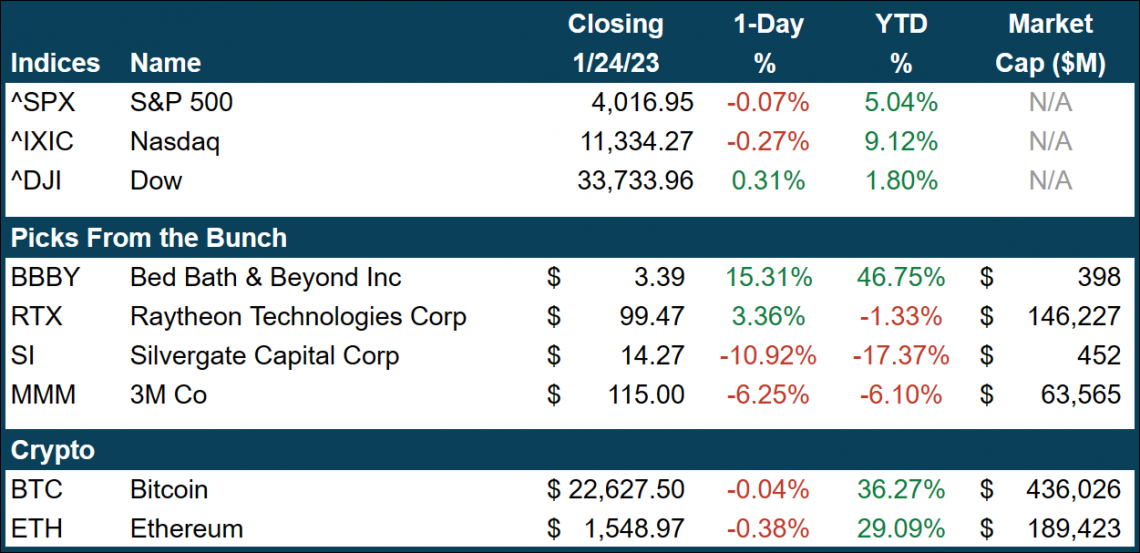

Moving on, Microsoft announced earnings yesterday. Shares popped off out the gate, gaining nearly 5% immediately in after hours trading. As traders do, once they actually started reading the report, shares crashed right back down to Earth.

At the time of writing, shares had moved down about 1% following the quarterly drop. Let’s take a look at why.

Similar to bank earnings providing economic data so good you wanna inject it into your veins, Microsoft gives a phenomenal lens into the spending levels of businesses over a given time period. Here, that consists of September-December 2022, the same quarter the “guaranteed recession” idea came into question. LFG!

First and foremost, the big boi of the tech world did beat on the bottom line. EPS came in at $2.32 vs. the consensus of $2.29. Top line missed by about 0.35%, clocking in at $52.75bn vs. the $52.94bn expected.

That’s all fine and dandy, but slow-reading investors became concerned once they actually started to pay attention to the parts making up the sum.

First and foremost, the most disappointing part of the report was the lackluster revenue guidance the firm gave, projecting ~$1.5bn less than consensus estimates for the firm’s estimates.

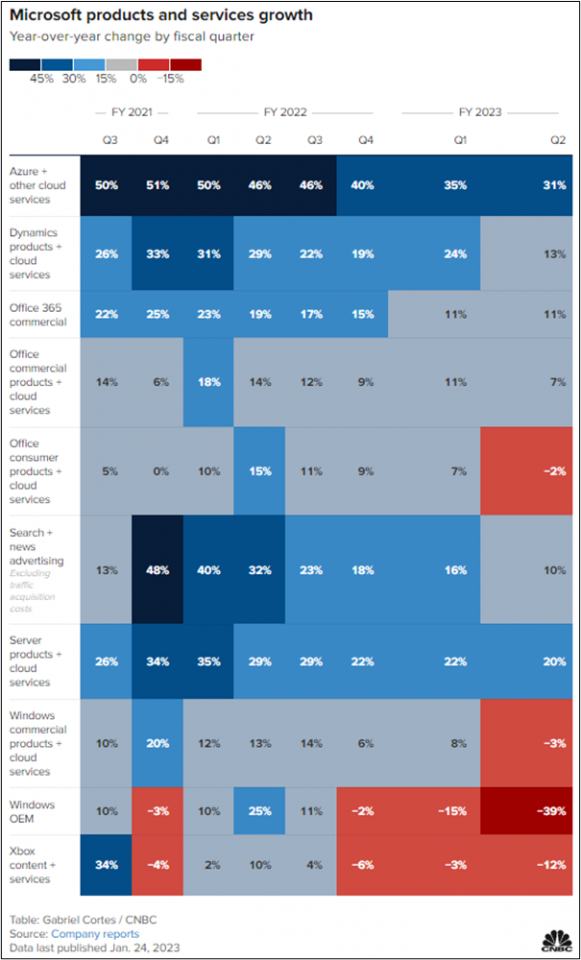

The spotlight was on Microsoft’s Intelligent Cloud business, containing units like the Windows and SQL servers, Nuance and Enterprise Services, and most importantly, Azure.

Azure is Microsoft’s most important engine of growth right now. Throughout 2021 and into 2022, that figure averaged around 50%. Last quarter’s growth was posted at 31%, the unit’s slowest growth ever, but still just barely beating expectations. As we all know far too well at this point, coming in line with expectations is basically equivalent to not doing anything at all. Tough look, but it could’ve been a lot worse.

Analysts seem to have anticipated far worse numbers across much of the rest of the business. Growth in units such as Office Commercial, Office 365, and Dynamic products, which include LinkedIn, all hovered around the respectable 7-13% levels. Even goddamn search advertising (that means Bing, btw) accelerated 10% last quarter.

Now, for the tough part. Pretty much anything related to the consumer slumped. PC sales tanked in Q4 from producers like Lenovo and Dell, and as a result, much of Microsoft’s personal computing products fell hardcore. The biggest loser of the quarter was the Windows OEM sector, declining at a rate of 39% YoY.

Video games apparently took a dive as well. Xbox and related services fell 19% over the year, likely stemming from consumers deciding to tighten their belts. This segment fell for the previous two quarters as well, however, so it wasn’t a surprise or anything. Maybe Satya’s tanking to show Lina Khan and the FTC that they need Activision Blizzard to stem the bleeding in the game sector. Good luck.

Taking a broader view, Microsoft’s earnings suggest consumer spending on luxuries like a new laptop is in the absolute gutter while business spending remains resilient but faces challenges. Slowing growth across B2B units suggests a pullback and cost controls across the economy, confirming trends like those observed in tech layoffs and Goldman getting rid of free coffee.

It’s just one company, but it’s a damn big one. We’ll get the rest of big tech’s results starting next week, and man, are we gonna have some fun then.

Stay tuned, apes!

|

Inventore unde maxime velit quidem quia delectus eveniet. Corrupti ut quas quam provident aut voluptatem et. Et qui qui reprehenderit voluptatem accusantium aut. A recusandae quo qui officia ea libero aut. Delectus reprehenderit repellat est. Magnam ipsam in eligendi nostrum sapiente aspernatur.

Sequi hic aut porro ex. Facilis molestiae autem sint sit voluptatum iusto soluta.

Aut explicabo quam quibusdam laboriosam non. Accusamus reprehenderit qui nam sit. Sint quam deserunt possimus explicabo non est. Libero libero necessitatibus qui accusamus quae vel ut.

Cumque odio provident hic fugiat est. Laboriosam ducimus soluta consequatur a est. Dolorem veniam amet distinctio commodi. Deleniti molestiae ipsum aut corporis. Placeat est voluptatem voluptatibus modi nobis porro.

See All Comments - 100% Free

WSO depends on everyone being able to pitch in when they know something. Unlock with your email and get bonus: 6 financial modeling lessons free ($199 value)

or Unlock with your social account...

Rerum minus ut et repellat blanditiis rerum quia. Cupiditate quisquam explicabo consequatur. Accusamus sequi quia consectetur aliquid. Porro quia itaque corporis. Consequatur minus sit debitis et. Exercitationem quasi qui dolore eligendi dignissimos molestiae non ullam.

Sit dolorem vero doloribus quasi repudiandae et ut. Quo dolor possimus ut eos et similique. Autem delectus et deleniti maxime ut. Est minima unde reiciendis adipisci perspiciatis.

Fugit labore id rerum accusantium eveniet qui amet. Deserunt saepe blanditiis et sed quo aliquam hic. Sequi quibusdam velit velit quaerat aut dolorum hic. Excepturi et qui assumenda et. Alias delectus omnis omnis consequuntur velit.

Aut voluptas inventore odio quos quod est. Corporis eos tenetur sed eaque qui voluptatem. Architecto rerum qui itaque alias. Explicabo aut deserunt at nobis voluptatem qui sunt. Ipsum eligendi voluptas alias hic quae quisquam qui. Voluptatem eos consequatur in doloribus totam sapiente omnis.