Private Wealth Management

The financial planning and investment management services provided to high-net-worth individuals (HNWI) and/or families.

What Is Private Wealth Management?

Private Wealth Management (PWM) refers to the financial planning and investment management services provided to high-net-worth individuals (HNWI) and/or families.

HNWIs require PWM services because they have sophisticated financial situations with a usually large number of financial assets. If HNWIs managed those assets, they would have no time for other things.

Hence, most HNWIs will pay the price for someone to manage their assets.

Firms offer financial planning and investment management services, including, but not limited to, investment portfolio management, tax planning, real estate planning, risk management, and general financial advice.

PWM professionals and managers often work with a team of advisors who are experts in law and accounting to help clients achieve their financial goals and protect their wealth.

PWM firms may also offer additional services (with extra cost depending on their terms), such as philanthropic planning and real estate consulting.

Note

PWM aims to help clients expand and preserve their wealth over the long term, aligning with the client’s goals.

- Private wealth management involves the provision of personalized financial advisory and investment services to high-net-worth individuals (HNWIs) and families.

- Private wealth managers cater to the unique needs and objectives of affluent clients, offering tailored solutions for wealth preservation, growth, and succession planning.

- Private wealth management services encompass a wide range of offerings, including investment management, financial planning, tax optimization, estate planning, philanthropy advisory, and risk management.

- Private wealth managers have a fiduciary duty to act in the best interests of their clients, prioritizing client needs over their own interests and ensuring full disclosure of fees, conflicts of interest, and investment risks.

Who Offers Private Wealth Management Services?

PWM services are typically offered by financial institutions such as banks, investment firms, and wealth management firms. Banks and investment firms may have dedicated PWM divisions or teams that serve HNWIs. In addition, PWM professionals may work for these institutions as employees or independent advisors who work with clients on a freelance basis (usually wealth management firms).

Some PWM firms are large, multinational institutions that offer a wide range of financial products and services. These firms may have a global presence and serve clients worldwide.

Other PWM firms are smaller, meaning they are more focused on providing personalized service to a select group of clients. These firms typically offer a more tailored approach toward their clients and may offer a wider range of services beyond traditional investment management.

In addition to traditional financial institutions, independent wealth management firms may also offer PWM services that specialize in serving HNWIs. These boutique firms are more focused on providing personalized and a wider range of services beyond traditional investment management offered by big institutions.

Regardless of the type of institution or firm offering PWM services, the goal is generally the same: to help HNWIs grow and preserve their wealth over the long term while also considering their values and goals.

Note

PWM professionals may work with a team of advisors, including attorneys, accountants, and insurance specialists, to help clients achieve their financial goals and protect their wealth.

If you ever enter the realm of PWM, you can work for these large financial institutions as an employee or be an independent advisor who works with clients on a freelance basis.

The following are some of the best wealth management firms:

- Morgan Stanley Private Wealth Management

- Merrill Private Wealth Management

- UBS Private Wealth Management

- Ameriprise Financial

- Advisor Group

Functions of Private Wealth Management Firms

As briefly mentioned, PWM firms offer a range of services to help HNWIs achieve their financial goals and preserve their wealth in the long term.

Examples of these activities include but are not limited to:

- Investment Portfolio Management: Private wealth managers help clients build and manage their investment portfolios, taking into account the client's risk tolerance, financial goals, and investment time horizon.

- This may involve selecting individual investments, such as stocks and bonds, and more complex investment products, like hedge funds and private equity.

- Tax Planning: Private wealth managers may work with clients to develop strategies that minimize their tax burden and maximize their wealth. This may include recommending specific investments or structures like trusts to help clients achieve their tax planning goals.

- Estate Planning: Private wealth managers may help clients develop and implement estate plans that outline how they would like their assets to be distributed after they pass away. This may include creating wills, trusts, and other legal documents to ensure that the client's wishes are fulfilled

- Risk Management: Private wealth managers may help clients identify and manage potential risks to their wealth, such as market fluctuations or legal challenges. This may involve recommending insurance products or implementing risk management strategies to protect against these risks.

- Financial Planning: Private wealth managers may help clients develop long-term financial plans that outline how they can achieve their financial goals and manage their wealth over time. This may include setting financial goals, creating budgets, and developing strategies for saving and investing.

- Philanthropic Planning: Some private wealth managers may also help clients develop and implement philanthropic plans, which outline how they would like to use their wealth to impact the world positively.

- This may involve recommending charitable organizations and causes to support and creating philanthropic structures like charitable trusts.

- Additional services: Some PWM may offer additional services such as real estate consulting and concierge services that help clients manage and balance their personal and professional lives. However, these specific services offered may vary depending on the firm’s size, focus, and clientele.

Who receives Private Wealth Management Services?

PWM services are targeted toward high-net-worth individuals. HNWIs include successful businesspeople, celebrities, and other high-profile individuals. These individuals are more likely to use PWM services to help them manage their assets and achieve their financial goals.

The definition of "high net worth" varies depending on the specific wealth management firm or institution. Still, given the name, it’s safe to say that high net worth refers to individuals or families with significant financial assets.

PWM firms have different minimum asset requirements when accepting clients. They may also consider other factors when considering an intake, such as the complexity of the client's financial situation and the level of service they seek.

The threshold for a "significant amount" of assets varies, but it’s most likely in the millions.

Note

Wall Street Ltd. considers an individual an HNWI if they have at least $1 million in investable assets. In contrast, Oasis & Co. considers individuals to be high-net-worth if their assets total over $5 million.

In addition to the number of financial assets a person has, other factors that may be considered in determining whether someone is an HNWI include their income, the value of their business or other assets, and overall financial complexity.

HNWIs are often seeking more personalized and comprehensive financial planning and investment management services than what is typically offered through traditional financial institutions, and PWM firms are typically geared toward serving this market.

In general, PWM is geared towards individuals and families who are seeking more personalized and comprehensive financial planning and investment management services than what is typically offered through traditional financial institutions.

The following are four famous people who may have used PWM services include:

- Elon Musk: Musk, the founder and CEO of SpaceX and Tesla (and now CEO of Twitter), has a net worth of billions of dollars from his successful business ventures. So it’s safe to say Musk wouldn’t have time to manage his assets on top of all his ventures and responsibilities.

- Oprah Winfrey: Winfrey, a media executive, philanthropist, and TV star, has billions of dollars in net worth. Suppose she spent all her time managing money. How would she have time to be on TV?

- Warren Buffet: Buffet, an investment legend and CEO of Berkshire Hathaway known for his wealth management expertise will not leave his billions of dollars hanging. Knowing much about wealth management doesn’t mean he has to do it himself.

- Mark Zuckerberg: Zuckerberg, the co-founder and CEO of Meta Platforms (formerly known as Facebook), has earned billions of dollars from all the advertising posts you scroll through daily. Unfortunately, if he wants to continue to do that, he won’t have time for wealth management - this is where PWM comes in.

These are just a few examples, and many other HNWIs may use PWM services to help them achieve their financial goals.

How do Private Wealth Management Firms Operate?

PWM firms have teams of financial advisors, investment managers, and other specialists who work closely with clients to achieve their financial goals and specific needs.

The general outline of how a PWM firm operates is as follows:

- Client Acquisition: PWM firms target wealthy individuals and families as their primary clients. These clients may be referred by the firm’s other clients or identified through the firm’s marketing efforts.

- Initial consultation: When a PWM firm finds a potential client who has expressed interest, it will schedule an initial consultation to discuss its financial goals and needs, risk tolerance, and the services it can provide.

- Financial planning: After the initial consultation, the firm will work with the client to develop a customized financial plan, which may include investment strategies, retirement plans, tax plans, real estate plans, and other financial plans and considerations.

- Investment management: One of the primary services PWM firms provide is investment management, which involves creating and/or managing a portfolio of stocks, bonds, and other securities on behalf of the client or providing recommendations for the client to invest in certain financial products.

- Ongoing communication: Since PWM firms work with clients continuously, they have regular meetings and communication to review the client’s financial plans and investment portfolios to ensure they are on track to meet their financial goals.

- This can include adjusting the client’s financial plan or investment strategy.

- Additional services: If requested, PWM firms will offer additional services like financial education, philanthropic planning, and succession planning.

Note

PWM firms typically use a fee-based payment scale rather than a commission-based one, meaning managers charge their clients a percentage of the assets under management.

By doing so, managers can avoid conflict of interest and have better performance potential.

A commission-based payment incentivizes the managers to recommend investment products that will let them earn high commissions but offer less growth potential to the client’s wealth.

On the other hand, a fee-based payment allows the managers to create a portfolio with various high-profit investment products, leading to growth in the client’s wealth since it is independent of the investment products chosen.

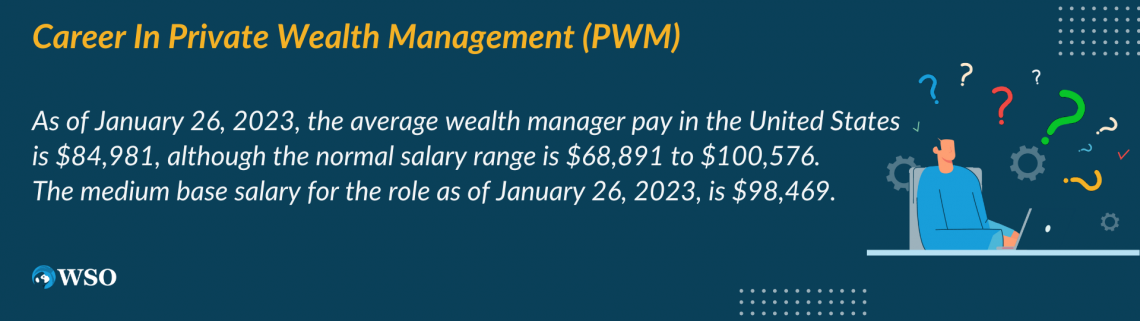

Thinking about Working in Private Wealth Management?

PWM is a considerably lucrative and popular sector of finance to enter. However, if you are considering a career in PWM, you should prepare beforehand since there is a lot of competition.

If you want to enter PWM, there are a few things to keep in mind:

Education And Credentials

Many PWM firms prefer to hire candidates with a bachelor's degree in a related field, such as finance, business, or economics; some firms may also require or prefer candidates with advanced degrees, such as a master's in business administration (MBA).

In addition, obtaining professional certifications, such as the Certified Financial Planner (CFP) designation, can benefit those interested in working in PWM.

Skills And Experience

PWM professionals should have strong communication and interpersonal skills and the ability to think critically and analyze financial information.

Note

Experience in the financial industry through internships or previous employment can also be helpful when seeking a job in PWM.

Job Responsibilities

PWM professionals may be responsible for various tasks, including developing and implementing financial plans, managing investment portfolios, and providing financial advice to clients.

They may also be responsible for maintaining client relationships and building new businesses.

Work Environment

PWM professionals work in office environments and may spend significant time interacting with clients and colleagues. Some professionals may also be required to travel for work.

Career Outlook

The demand for PWM professionals is expected to grow in the coming years as the number of high-net-worth individuals and families continues to increase.

However, competition for jobs in this field can be fierce, and those who successfully secure a position in PWM will typically have a strong educational background and relevant experience.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?