Non-Qualified Plan

A retirement savings plan that is tax-deferred and employer-sponsored.

What Is a Non-qualified Plan?

A non-qualified plan is a retirement savings plan that is tax-deferred and employer-sponsored. It falls outside the ERISA (Employee Retirement Income Security Act) guidelines and is exempt from the testing required with qualified retirement savings plans.

In this article, we will cover what a non-qualified plan does, why it is beneficial, the different types of non-qualified plans, and the difference between a qualified and a non-qualified plan.

The plan acts as an employee recruitment and retention tool designed to meet retirement needs for key executives and senior management-type employees. The reason for this being is that they are high earners and provide extra incentives to the companies.

The plan also acts as an employer agrees to compensate specific employees for their current services. It also provides more flexibility and is not subject to the same government requirements as other plans, such as the IRA or a 401(k).

It allows a service provider (like an employee, for instance) to earn wages, bonuses, and other types of compensation and then receive them at a later date, thus deferring their income tax.

Employers offer non-qualified plans to help employees save for retirement and allow employees to make up for limitations placed on qualified plans, as they don't have the same rules as qualified plans. It helps employers recruit, retain, reward, and retire top employees and can motivate the executive’s job performance.

They are nondeductible to the employer and are taxable to the employee. Still, they can allow employees to defer these taxes until their retirement and provide special forms of compensation to key employees and executives.

- Retirement Savings Tool: Non-qualified plans offer a method for retirement savings, sponsored by employers and tax-deferred.

- Exclusion from ERISA and IRC Guidelines: Unlike qualified plans, they lack ERISA or IRC safeguards, providing flexibility but also less regulatory protection.

- Executive and Top Employee Benefits: Designed to offer additional retirement savings options specifically for executives and key employees.

- Variety of Plan Types: Non-qualified plans encompass five main types, including deferred compensation, salary-continuation, executive bonus, split-dollar life insurance, and group carve-out.

- Employee Incentive and Reward: Serve as a means for employers to recruit, retain, reward, and retire top talent, motivating them to contribute to the company's success.

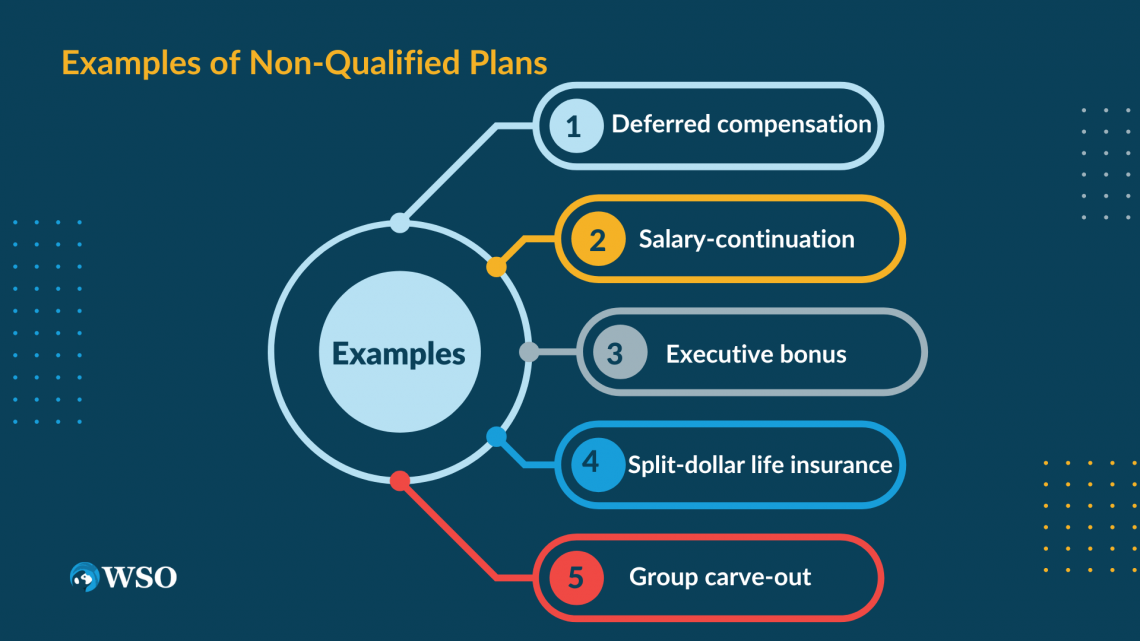

Examples of Non-Qualified Plans

In the following part, we will explore the different types of non-qualified plans, such as:

- Deferred compensation,

- Salary-continuation,

- Executive bonus,

- Split-dollar life in

- Group carve-out.

A deferred compensation plan allows the employee to receive earned compensation later. It includes retirement, pension, and stock option plans, as well as 401(k), excess benefit, bonus, and severance pay plans.

A salary-continuation plan includes funds that an employer pays for future retirement benefits of an executive or higher-tier employee. The employer continues to pay the employee through retirement at a reduced rate.

An executive bonus plan provides supplemental benefits to executives and employees at a deductible business expense for the employer. The employer issues the employee’s life insurance policy and pays the premiums as bonus compensation.

The split-dollar life insurance plan permits premium costs, cash values, and tax benefits of a permanent life insurance plan to be shared between the employer and the employee. It’s not highly regulated and may differ based on a specific contract or situation.

A group carve-out plan replaces part of an employee’s group insurance policy with an individual life insurance policy to avoid high costs.

Non-qualified vs. qualified plans

Now that we’ve discussed what non-qualified plans are, how they work, and their different types, you’re probably wondering what a qualified plan is and how they differ from non-qualified ones.

Qualified plans are employer-sponsored retirement plans that meet the IRC (Internal Revenue Code) and ERISA (Employment Retirement Income Security Act) requirements to qualify for specific tax benefits.

In a qualified plan, you have tax-deferred contributions where employers can deduct money from the plan. They are funded with pre-tax dollars, while non-qualified are funded with post-tax dollars.

A qualified retirement plan includes 401(k), 403(b), Keogh(HR-10), and profit-sharing plans. It can include tax deductions for employer and employee compensation and tax-deferred investment gains until the money is withdrawn from the account.

The table below shows a clear comparison between qualified and non-qualified plans.

| Non-Qualified Plans | Qualified Plans |

|---|---|

| Use after-tax dollars to fund. | Have tax-deferred contributions from employees. (funded with pre-tax dollars) |

| Employers cannot claim their contributions as a tax deduction. | Employers can deduct amounts contributed to the plan. |

| Only select employees are eligible. | All employees are equally eligible. |

| Do not have loans. | Have loans if the plan allows it. |

| Have no IRS-defined limits. | Have compensation deferral limits (total dollar limits are adjusted by the IRS yearly). |

| Assets are not protected from company creditors. | Assets are protected from company creditors. |

One of the biggest differences between a qualified and a non-qualified plan is that qualified plans have safeguards while non-qualified ones do not.

or Want to Sign up with your social account?