Acceleration Clause

A clause that provides the lender the right to demand full repayment of the loan if the borrower fails to pay it off.

What Is an Acceleration Clause?

An Acceleration clause in a contract gives the lender the right to demand full repayment of the loan if the borrower fails to pay it off. Such clauses are commonly utilized in mortgage loans and real estate lending.

It is also known as an "Acceleration Covenant." It is a rule in a loan agreement. It allows the lender to demand quick repayment if certain conditions are unmet. It helps to protect the lender if the borrower breaches their obligations.

It can be triggered by missed payments, defaulting on other debts, or not meeting financial goals. In a business enterprise loan, there is probably a provision that we could allow the lender to ask for a fast charge if the borrower fails to meet unique monetary desires or pay previous money owed.

Borrowers must note the clause before signing the settlement, as it's a critical part of the mortgage settlement. Failing to comply with the clause can result in consequences like foreclosure, legal actions, etc.

- An acceleration clause is a provision in a loan agreement or mortgage that allows the lender to demand immediate repayment of the entire loan balance if certain conditions are met.

- The primary purpose of an acceleration clause is to protect the lender's interests by allowing them to quickly recoup their funds in the event of borrower default or other specified conditions.

- It ensures that lenders can take prompt action to mitigate losses if the borrower's financial situation deteriorates.

- Invoking an acceleration clause and the subsequent default or foreclosure can significantly impact the borrower's credit score and credit history.

Example Of Acceleration Clause

There are a few examples of the acceleration clause.

Let us now look at an example to understand the concept of an acceleration clause better.

- Jack agreed to buy a commercial property from Max for $600,000.

- Jack has to pay back the money in 10 equal yearly installments of $60,000.

- Jack paid the first seven installments on time.

- However, Jack should have paid the eighth installment on time, which caused a default.

- Because of a clause in the agreement, Max can ask Jack to repay the remaining $180,000 immediately.

- Suppose Jack needs to pay the remaining debt within the specified time. In that case, Max can take back the commercial property without giving back the $420,000 Jack already paid.

Thus, the above acceleration clause instance clearly explains the technique. It is important to note that the acceleration clause will no longer be precipitated on its own if the borrower fails to pay an installment. The cause occurs after the lender decides to invoke the clause.

Importance of Acceleration Clause in Loan Agreements

These rules are critical in loan agreements because they give lenders a powerful tool to protect themselves. They help them reduce their risk of default. Lenders can use an "acceleration provision" to get their money quickly.

It can be seen when the borrower's financial status changes, such as during economic downturns or unforeseen personal occurrences.

For Lenders

The clause states that if the defaulter no longer meets their responsibilities or violates the clause, the lender can ask the borrower to pay off the full loan.

Rather than waiting for the borrower to make regular payments over time, this can assist lenders to limit their risk and recoup their assets more rapidly. Extending the repayment time can also keep borrowers from accruing further interest and fees.

For Borrowers

Borrowers need to be aware of the clause and comprehend the elements that would cause it to be activated.

Failure to comply with those triggers can have profound implications, including default, foreclosure, and deterioration of credit score ratings. If borrowers take steps to prevent it from being used, it can help them keep their finances stable and avoid hardships.

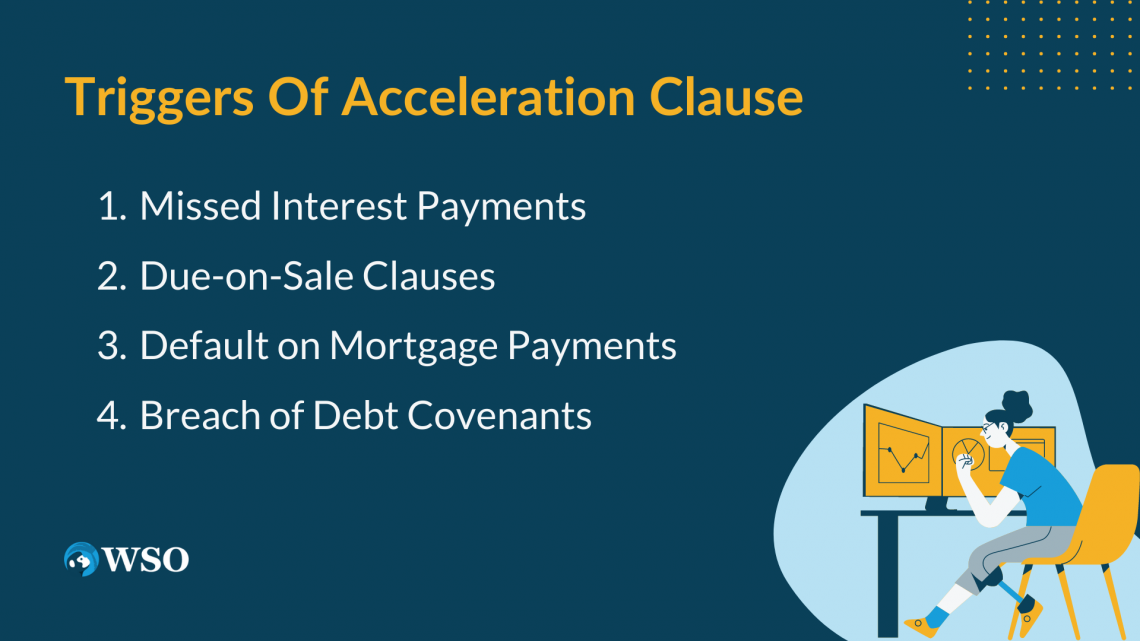

Triggers of Acceleration Clause

Let us list out a few situations that may make the lender invoke the clause in the loan.

1. Missed Interest Payments

Loan agreements must include interest payments; not making them can have a serious impact. Lenders can enforce full loan repayment under this clause if borrowers don't make timely interest payments.

NOTE

Depending on the loan agreement, a different number of missed payments must occur before the clause occurs.

2. Due-on-Sale Clauses

Due-on-sale clauses in loan agreements give lenders the right to request complete repayment of the principal sum if the borrower sells the real estate pledged as security for the loan.

If the property is sold, this clause, comparable to an acceleration clause, can be used to start an accelerated loan repayment.

3. Default on Mortgage Payments

Large loans must be repaid largely through mortgage payments, which must be made on time to avoid default.

A lender may invoke the clause requiring full loan repayment if a borrower skips a predetermined number of mortgage payments.

4. Breach of Debt Covenants

Lenders impose limitations on borrowers through debt covenants to reduce risk and align interests. If the borrower violates these limitations, the lender may invoke the clause and demand full repayment.

NOTE

To prevent default and the triggering of clauses, borrowers must be aware of the debt covenants and make sure they abide by them.

How many late payments before an Acceleration clause kicks in?

The number of late payments required before a clause can vary depending on the precise phrases outlined in the agreement. The number of late payments triggering the clause isn't constant.

Your lender and your loan documents will determine this. Your lender may have the right to declare the entire loan due if you miss only one payment.

Generally, creditors won't ask you to pay the sum until you have made no more than two or three payments. Due to the pandemic, many people are facing money problems. So, lenders are giving borrowers a chance to pay off their late payments.

Lenders use acceleration clauses as a strategic measure to protect their investments. These clauses serve as a secret weapon, allowing lenders to minimize their financial losses.

If a borrower cannot make payments, the lender retains the right to reclaim the asset. By implementing the clauses, lenders can swiftly take action. Also, they can mitigate potential expenses associated with delinquent payments.

The Breach Letter After Activation of Clause

Several items and checklists should be specified in the letter.

A breach letter must specify the following:

- The default, or what the borrower has done wrong.

- The action required to cure the default or what the borrower needs to do to fix the problem.

- A deadline by which the default must be cured, typically at least 30 days after the borrower receives the notice.

- The debt might be accelerated, and the property might be sold if the borrower doesn't address the problem by the deadline stated in the notice.

- The servicer typically sends this letter when the borrower is around 90 days delinquent on payments.

- According to federal law, a lender cannot start the process of taking back a property through foreclosure until 120 days from the default.

- If the borrower does not cure the default, the foreclosure will begin.

The notice also often informs the borrower of the following:

- The right to reinstate the loan after acceleration or the ability to get back on track with payments,

- The right to assert no default or raise a defense in a foreclosure proceeding.

Right to Reinstate the Loan

Borrowers may struggle to make their loan payments and fall behind at times. If this occurs, the lender can use the provision that says that the borrower has to pay back the whole loan all at once.

However, a clause in some loan agreements called the right to reinstate enables the borrower to correct the issue and keep the loan. It allows the borrower to get back on track by paying the overdue amount plus additional costs.

Borrowers who have a temporary financial problem but can still make their loan payments may find the right to reinstate useful. It means they can pay off their loan and avoid foreclosure. Foreclosure occurs when a person loses his property as they cannot repay their loan.

They can avoid this by exercising their right to reinstate and keep their homes. This also enables them to guard their credit rating, which indicates how well they repay their debts.

Let us understand the terms and conditions of reinstatement. The right to reinstate clause has specific terms and conditions.

- Some lenders may need repayment of the entire loan balance to reinstate the loan.

- It is important to act quickly because there may be a limited time window to exercise the right to reinstate and avoid foreclosure.

Reinstate the Loan After Acceleration

To reinstate the loan, several ways can be appointed.

Some of the ways to reinstate the loan are listed below:

- If the clause in a loan agreement is activated, the lender has demanded immediate compensation for the full Loan.

- However, under some conditions, it is possible that the borrower can reinstate the loan.

- After acceleration, the borrower should pay the lender all past-due sums as if the acceleration never took place to reinstate the loan.

- Moreover, one needs to fix issues that caused the failure and pay back the lender for any expenses they had while enforcing the agreement.

- The expenses related to protecting the lender's stake in the property might include fair fees, such as legal fees and inspection costs.

- The reinstatement may be paid using a cash order, certified cheque, bank cheque, cashier's cheque, or electronic finances transfer.

- The mortgage or deed of trust and your obligations under it return to how they were before the acceleration once you reinstate the loan.

For Seeking Assistance:

- Inform your loan servicer right away if you're struggling to pay your mortgage to explore available options.

- If your loan is being accelerated and a foreclosure is looming, consult a foreclosure lawyer to understand potential defenses and loss mitigation choices suitable for your case.

- If you can't afford a lawyer, reach out to a HUD-approved housing counselor for free assistance, particularly regarding foreclosure prevention methods

What is Foreclosure?

Foreclosure is a provision included in loan agreements. These clauses give the right to demand immediate repayment of the entire loan amount if borrowers fail to pay.

The specific number of missed payments required to trigger the clause. Lenders usually follow one of two methods to take back property when a loan is sped up, and borrowers must catch up on payments or do something to prevent it.

The initial step is a judicial foreclosure, where the lender files a lawsuit in court to foreclose on the property.

The second process is a non-judicial foreclosure that does not involve going to court, but they have to follow state laws.

A new owner, frequently the lender itself, purchases the house at a public auction after the lender has satisfied all legal requirements for foreclosure.

In judicial foreclosures, the sheriff's sale is frequently used as the last stage of the foreclosure procedure. Trustee sales tend to occur more frequently in nonjudicial foreclosures.

Conclusion

To sum up, the acceleration clause is an essential aspect of a loan agreement that each borrower and lender should know. It can significantly impact what transpires if there are issues with the loan.

Furthermore, borrowers must keep the lines of communication open with their lenders. Reaching out to the lender and discussing potential substitutes or modifications to the loan agreement can be helpful in the event of financial hardship or unanticipated circumstances.

Lenders may be willing to work with borrowers to find a solution that avoids the activation of the acceleration clause.

They can protect themselves and reduce the chances of not being able to make payments or losing their property by knowing what can trigger the clause and what will happen if it does.

Reading and apprehending the entire loan settlement, including the acceleration clause, is essential to ensure you understand all the phases before signing. It will help you stay informed and be prepared for any situation.

Seeking expert advice can assist borrowers in fully realizing the implications of the clause. Reinstating the loan can be viable in positive instances, allowing the borrower to deliver the loan back into excellent standing and keep normal payments, subject to the lender's discretion and phrases.

Researched and authored by Khushboo Gupta | LinkedIn

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?